Asian Market Update: PBoC expands liquidity with lower repo yields; Ebola worries send US markets to new multi-month lows

Tue, 14 Oct 2014 0:00 AM EST

***Economic Data***

- (AU) AUSTRALIA SEPT NAB BUSINESS CONFIDENCE: 5 (lowest since mid 2013) V 7 PRIOR

- (AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 113.8 v 112.6 prior

- (JP) JAPAN SEPT PPI M/M: -0.1% V -0.1%E; Y/Y: 3.5% (6-month low) V 3.6%E

- (JP) JAPAN SEPT M2 MONEY SUPPLY M2 Y/Y: 3.0% v 2.9%E; M3 Y/Y: 2.5% V 2.4%E

- (SG) SINGAPORE Q3 ADVANCED GDP Q/Q: 1.2% V 0.8%E V Y/Y: 2.4% V 2.7%E

- (KR) SOUTH KOREA SEPT BANK LENDING TO HOUSEHOLD (KRW): 501.3T V 497.0T PRIOR

- (UK) UK SEPT BRC SALES LFL Y/Y: -2.1% (biggest decline in 17 months) V +1.0%E

***Index Snapshot (as of 02:30 GMT)***

- Nikkei225 -1.6%, S&P/ASX +1.1%, Kospi +0.3%, Shanghai Composite +0.3%, Hang Seng +0.7%, Dec S&P500 +0.6% at 1,875

***Commodities/Fixed Income***

- Dec gold +0.3% at $1,233/oz, Nov crude oil -0.8% at $85.06/brl, Dec copper flat $3.04/lb

- GLD: SPDR Gold Trust ETF daily holdings rise 1.8 tonnes to 761.2 tonnes; First rise since Sept 10

- SLV: iShares Silver Trust ETF daily holdings fall to 10,717 tonnes from 10,753 tonnes prior (lowest since Sept 23rd)

- (CN) PBoC to drain CNY20B in 14-day repos (21st consecutive drain); Offer yield at 3.4% v 3.5% prior (3rd yield cut, prior offer yield cut by 20bps to 3.5% from 3.7% on Sept 17th)

- USD/CNY: (CN) PBoC sets yuan mid point at 6.1408 v 6.1446 prior setting (strongest Yuan setting since March 18th)

- (JP) BOJ offers to buy ¥300B in 1-3yr JGB, ¥200B in 3-5yr JGB, ¥400B in 5-10yr JGB, as well as ¥3.5T in T-bills

- (AU) Australia MoF (AOFM) sells A$300M in indexed bonds due 2018; Average yield of 0.6348%; Bid-to-cover: 3.68x

***Market Focal Points/Key Themes/FX***

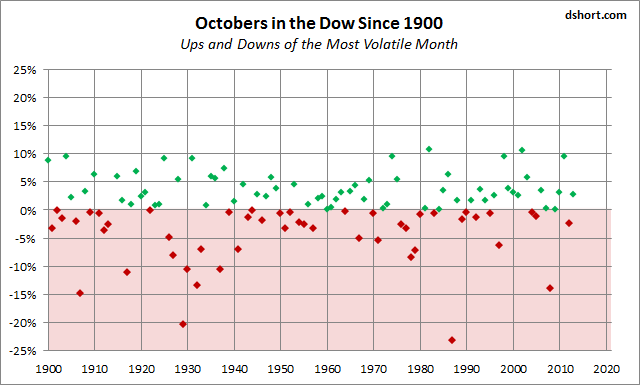

- Dow Industrials and S&P500 cash indices hit 5-month and 4-month lows respectively going into the close as Ebola concerns are hitting panic levels. This marks a 3rd consecutive sharp losing session, and the 3-day drop is the biggest since late 2011. In the final hour, an Air Emirates plane landed in Boston was boarded by health officials after reports that up to 10 passengers were suffering from flu-like symptoms. Subsequent reports indicate there was no Ebola threat at Boston's Logan Airport. Later in the evening, University of Kansas Hospital isolated a man with possible Ebola symptoms - the patient is himself a medic from Kansas and worked on a boat off the coast of Africa treating sick people from regions with prevalent Ebola cases.

- Australia market is outperforming in the region, further helped by positive momentum in basic materials and resources in the wake of stronger than expected September imports in China. Investors are shrugging a slowdown in NAB Business Confidence to a 1-year low, with NAB economist citing lower commodity prices, excess capacity and cautious spending behaviour. RBA assistant gov Debelle said lower AUD may be helpful to meet balanced growth, adding the recent decline still does not match the deteriorating fundamentals on trade weighted basis. AUD/USD sold down below $0.8740 before bouncing above $0.88 handle on broader market strength.

- China is also modestly higher, as traders cheer another de facto easing by the PBoC. For the 3rd time in the last 2 months, PBoC lowered the offering yield on its 14-day repo operations by 10bps to 3.4%. Lending data for September is also on the radar, with press speculation the new Yuan loans could rise from CNY702B in Aug to CNY720-800B.

- Singapore GDP was mixed, accompanied by the semiannual policy review from the Singapore Central Bank. MAS maintained its policy stance allowing for modest gradual appreciation of SGD near policy band, but also lowered its inflation outlook to 1.0-1.5%, briefly sending USD/SGD up by over 30pips above 1.2740.

- A VOX poll out of Brazil showed incumbent Rousseff with a marginal 45% to 44% lead over pro-business Neves. Recall yesterday, a sensus poll by Istoe saw Neves widening his lead to 52-37%, helping EWZ to a 5.6% gain in Monday's US session.

- Going into tomorrow's Bank of Korea policy decision, surveys see a majority of analysts forecasting a 25bp rate cut to 2.00%. Separately on the peninsula, North Korea's Kim Jong Un has made his first public appearance in over a month.

***Equities***

US markets:

- EXAC: Guides Q3 revenue to be at lower range of guidance and earnings to fall below guidance (prior guidance Q3 $0.24-0.26 v $0.25e, R$57.5-59.5M v $59Me); -0.4% afterhours

- GOOG: Said to lead a $500M investment in virtual reality company Magic Leap - tech blogs; -0.9% afterhours

- DRYS: Said to be seeking a loan to repay $700M in debt due Dec 1st - financial press; -1.4% afterhours

- AWI: Guides FY14 lower for EBITDA at $355-375M, R$2.68-2.72B v $2.75Be ($370-400M, R$2.7-2.8B prior guidance); -4.6% afterhours

Notable movers by sector:

- Consumer Discretionary: Coca-Cola Amatil CCL.AU +2.2% (may consider sale of asset); Japan Airlines 9201.JP -4.1%, ANA 9202.JP -4.4% (continued closures on typhoon, Ebola concerns)

- Financials: Yango Group 000671.CN +3.0% (controlling shareholder to raise stake)

- Materials: OZ Minerals Ltd OZL.AU +8.2% (Q3 production results); Mount Gibson Iron MGX.AU +10.7% (Q1 operating results)

- Industrials: Jiangsu Linyang Electronics 601222.CN +2.3% (to invest in photovoltaic projects)

- Technology: PCI-Suntek Technology 600728.CN -2.1% (to issue shares); FujiFilm Holdings 4901.JP +1.2% (prospects of vaccine on continued Ebola concerns)