Les discussions entre Orange et Bouygues s’accélèrent

Téléchargez l'appli JDD à la Une sur votre iPhone!

JDD à la une

à bientôt !

Fitbit v GoPro: faster, faster

Fitness trackers are beating action cameras, but Chinese rivals and Apple could be decisive

Both record your athletic exploits (or lack thereof). Both feature on this year’s Christmas lists. And both are electronics manufacturers that had initial public offerings in the past 18 months. So far, Fitbit, maker of movement tracking devices, and GoPro, maker of action cameras, are aligned. Nor are their revenues all that different: Fitbit had sales of $1.5bn in the past 12 months; GoPro’s were $1.8bn. Gross margins? GoPro’s stand at 46.7 per cent; Fitbit’s at 47.7 per cent.

Then they diverge. In terms of release schedule, it is Fitbit that looks to be struggling to stay with the pace. It entered the holiday season without a new gizmo in its product line-up: the latest model was released in January. But GoPro is sweating more heavily. It cut the price of its new Hero4 Session camera from $399 in July and $299 in September to $199 earlier this month. The company’s margin discount to Fitbit is only likely to widen.

The market has reacted to the varied performance. Fitbit is one of the most successful recent tech IPOs: its shares are up 50 per cent from its offer price, albeit they been much higher since the flotation. GoPro in contrast has fallen 20 per cent from its offer price and more than three quarters from its high last year. Fitbit’s enterprise value is about four times forward revenues, GoPro’s just above one times.

A gap is justified but this one looks too wide. Both companies are on the treadmill of developing new winners while seeing off increasingly vigorous competition. Occupying their narrow niches, they lack diversification to smooth out any bumps. GoPro does have one promised pivot: shifting to camera-equipped drones. But China’s DJI already makes room for a camera in its popular Phantom drone. Fitbit is not immune to Chinese competition: Xiaomi, whose fitness tracking devices sell for a fraction of the cost, could take advantage of better distribution in the US and Europe.

Then there is the Apple factor. For Fitbit, Apple is most likely to be a competitive threat — perhaps with a cheaper or more attractive version of its watch. GoPro, however, saw its shares jump 16 per cent this week on speculation that Apple could mount a takeover bid. This is one area GoPro would not have to discount: its market capitalisation of $2.6bn is spare change for the richest company on earth.

Brexit risk a chance for industry to engage in eurozone recovery http://on.ft.com/1P0sh2o

The UK’s fund industry should continue to prosper, in or out, say Huw van Steenis and Bruce Hamilton

Could rising fears of a British exit from the European Union be a bigger risk to the valuations of UK asset managers than to UK banks? This could be one of the big surprises for 2016.

Britain’s fund management industry has been a huge beneficiary of the single market. Take Ucits funds, Europe’s mutual fund umbrella: created 30 years ago, they are now the gold standard for retail investors, with more than €8tn of assets under management.

The UK’s fund management industry accounts for more than a third of assets managed in Europe. A key aspect of this growth has been UK companies’ ability to “passport” their funds into Europe as EU members. The benefits to the UK flow well beyond the City, with many jobs based in Edinburgh, Leeds and Glasgow.

Our base case is that the UK’s fund industry should continue to prosper, whether in or out. Skilled workforces and critical mass give the UK a strong competitive edge that would make it difficult to dislodge. But what if this assumption is wrong?

With the odds of Brexit in the polls close to one in three, according to Morgan Stanley research, fund managers need to explore the alternative scenarios. Brexit could raise questions about the ability of UK-based groups to sell retail funds elsewhere in Europe, if protectionist barriers are put up over time.

The call for protectionism is liable to come not only from those chancelleries keen to enjoy the tax revenue and skilled jobs from a vibrant asset management sector, but also those looking to protect domestic banking systems.

The European Central Bank’s dangerous experiment with negative deposit rates poses significant risks to the eurozone’s banks. As the ECB policy is a disincentive for banks to hold deposits, those institutions, controlling three-quarters of all fund distribution in Europe, will be under pressure to find other sources of fee income. Asset and wealth management are likely to be top of the list.

Brexit could affect distribution, competitiveness, legal structures and currency risk for asset managers.

Distribution costs may rise if the UK were not a European Economic Area member following Brexit, and the UK would need to renegotiate with each country to retain access to EU markets in financial services.

We suspect “grandfathering” arrangements would mean existing UK or European investors in Ucits funds would not need to be segregated, but there could be a challenge to new funds. In practice, UK-based asset managers would seek to establish EU-based management companies to circumvent this risk.

Companies may need to move some investment management jobs. More significant disruption and costs could be incurred if investment management of EU-based products could no longer be delegated back to the UK, as this could require separately capitalised EU subsidiaries and a bulking-up of EU-based investment staff.

Critical here would be the level necessary to satisfy localcountry authorities in the EU that the management company would have sufficient “substance” not to be a mere “letterbox” entity. If the EU drew the line much more tightly than it does for Swiss companies today, it would have a significant bearing on the level of resourcing required in the new EU-based authorised management company. But even if the UK could gain Swiss terms, there would probably be additional transaction costs, affecting competitiveness.

The severity of the repercussions would depend on the shape of post-Brexit trading arrangements. Everything would hang on the negotiation.

It is difficult for asset managers to do any meaningful contingency planning, when the range of outcomes is so wide. But engaging early with the EU, to show UK fund management’s relevance to rebooting the eurozone’s lacklustre recovery, is a good place to start.

Supporting European commissioner Lord Hill’s Capital Markets Union initiative to channel more market-based savings to eurozone companies is a key initiativeimportant — and UK fund managers have much to offer. If the risks of Brexit encourage asset managers to engage more in helping build a more vibrant and prosperous EU, there may be a silver lining to what looks an ominous storm cloud.

Huw van Steenis, World Economic Forum Global Agenda Council member, and Bruce Hamilton are managing directors at Morgan Stanley and recently co-authored “10 Surprises for 2016”

Irish regulator launches fund fee probe

The largest ever investigation in Europe into the fees asset managers charge investors will begin next year amid widespread accusations of overcharging within the fund management industry.

The financial watchdog in Ireland, which oversees more than 6,000 funds, including 3,725 mutual funds, is to examine whether the investment products offer “value for money”.

A spokesperson for the Central Bank of Ireland, the regulator, said: “In 2016, an area of focus will be fees charged by Irish-domiciled investment funds. Value for money for the end investor is an important part of the central bank’s mandate to protect investors’ interests.”

Industry figures say the probe will be a concern for asset management companies, where profit margins have already come under pressure due to increasing demand from regulators and consumers for lower-cost products.

However, Mick McAteer, director of the Financial Inclusion Centre, a think-tank, said: “It is good news that the Irish regulator is looking at fees. EU investors [in funds] pay far too much for inferior performance.”

Guillaume Prache, managing director of Better Finance, a consumer lobby group, added: “Overall, fees are too high in Europe and still not always transparent.”

Fund fees have been scrutinised in recent years due to claims that asset managers are charging investors large sums for active management despite closely following an index, a practice known as “closet tracking”.

It is understood the Irish regulator is separately carrying out a review of closet trackers, but its 2016 fund fee probe will go further.

The investigation of Ireland’s $2tn investment industry will initially focus on total expense ratios, which is a measure of the total cost of a fund to the investor. It usually includes the manager’s annual charge as well as the cost of other services paid for by the fund, such as fees paid to custodians and auditors.

The Irish watchdog is looking for “outliers”, funds that have very high total expense ratios. They will then be examined more closely. It is not clear how long the investigation will take.

Gina Miller, partner at SCM Private, the wealth manager, campaigns for greater fund fee disclosure. She said the probe should not just focus on the total expense ratio, claiming this can represents less than 50 per cent of the true cost. It often does not include performance fees and dealing costs, she said.

Fund professionals in Ireland have suggested the central bank’s investigation is unnecessary and smacks of “interference with the free market”.

A fund director who sits on the board of several Ireland-domiciled mutual funds, who requested anonymity, questioned whether it was the “regulator’s business to look at fees”, suggesting European-wide rules already address issues such as fee transparency.

“I am not sure it is up to the regulator to police what is good value,” he said.

However, Mr McAteer said: “The investment industry is one of the worst-performing industries consumers deal with and a range of interventions is needed to make this market work.”

Irish Funds, the local asset management industry association, declined to comment on the probe.

The financial regulator in Luxembourg, the largest domicile of funds in Europe, did not respond when asked if it also planned to investigate fund fees.

Dollar’s Next Move Could Be Lower

With the Fed set to hike rates, don’t be surprised if the dollar’s run of glory comes to an end next year.

All winning streaks must come to an end. The Golden State Warriors, for instance, have won 23 games in a row to start the season, an NBA record, but no one doubts that they will lose—and almost certainly more than once. Similarly, the U.S. dollar has had a winning streak of its own this year, and it might end sooner than you think.

The reasons for the dollar’s durability are so well known at this point that it almost feels unnecessary to recapitulate them here. This week, the Federal Reserve is expected to raise interest rates by a quarter point, its first hike since 2006. And because global investors are typically attracted to currencies with higher interest rates, the dollar should get a boost, especially as others like the Bank of Japan and the European Central Bank expand their bond-buying programs.

To which we say: Duh! The so-called divergence trade has been going on ever since the Federal Reserve said it would begin curtailing its bond purchases back in 2013—and the dollar has risen 20% since then. With the Fed set to hike interest rates this week, don’t be surprised if the dollar’s run of glory comes to an end next year.

That’s not a popular view. Bloomberg forecasts the Dollar Index—a measure of the strength of the U.S. dollar against the euro, yen, and pound, among others—will hit 101 by the end of next year, a 3.5% rise from Thursday’s 97.6. And many strategists are predicting that the euro and the dollar could trade at parity next year, a 9% drop from last week’s $1.099. And it’s largely thanks to the continued divergence between the ECB and the BoJ, on the one hand, and the Fed on the other.

Such divergences, however, aren’t all that rare. Fundstrat strategist Thomas Lee looked at the last 11 tightening cycles, going back to 1971, and found that five started when the ECB (or Germany’s Bundesbank before it) was easing, with such divergences lasting a median of 17 months. “In other words, this is surprisingly common,” Lee says. Nor did the divergences necessarily result in a stronger dollar. In fact, the dollar typically weakened a median 6.6% during the six months after a Fed hike, Lee says.

It’s not too hard to imagine scenarios that would result in such a reversal. Ever since the Fed finished tapering in October 2014, the conversation in the U.S. has been about when the Fed will hike but never about the assumption that it will. But if Yellen and company do in fact hike this week—and maybe again in early 2016—the discussion will inevitably change. Yes, the market will be watching the incoming economic data for signs of more hikes, but also for whether the data are so weak that the Fed will have to stay its hand, or even cut rates. “The very fact that you’re having that conversation is very different from the conversation of the last year or two,” says Daragh Maher, currency strategist at HSBC, who expects the dollar to finish 2016 at $1.20 per euro.

MAKING A RATE HIKE STICK has been tricky. Five central banks have raised interest rates since the financial crisis, and all have been forced to reverse in short order. That the European Central Bank blundered by raising rates beginning in 2010 has become a cautionary tale for policy makers everywhere. But even central banks that didn’t make mistakes have had trouble raising rates and keeping them there. The Reserve Bank of New Zealand, for instance, cut interest rates for the fourth time this year last week, reversing the rate hikes it had put into effect just last year. It’s not out of the question that the U.S. could be forced to do the same.

Nor is it all about the Fed. While investors have been betting on a Fed rate hike, they’ve also assumed that both the ECB and the Bank of Japan will do whatever it takes to boost growth—and weaken their currencies. The BoJ, however, will likely have to wait if it wants to add to its asset purchases after learning last week that the Japanese economy grew by a much better-than-expected 1% during the third quarter. And while the European Central Bank continues to expand its bond buying, Maher says “the potency of its promises is less than it was” following its meeting earlier this month, one that disappointed investors expecting more. “The ability of the ECB to engineer a lower euro once again is diminished,” he adds.

We could have reached the point of peak divergence—and peak dollar.

A WEAK DOLLAR would likely cause celebration among U.S. corporations, which have been battered by the resurgent greenback. Fundstrat’s Lee estimates that the dollar’s rise this year has subtracted $93 billion from the profits of S&P 500 companies, or $10 per S&P 500 share. According to his math, U.S. corporate profits would have grown by 8% without the impact of the strong dollar. A reversal of the dollar would go a long way toward making sure the “profit recession” U.S. companies faced this year is in the past.

So which companies would benefit the most from a weaker dollar? Lee screened for stocks that tended to move in the opposite direction of the dollar and have positive free cash flow, among other factors, and came up with 18. Yes, there were your typical, beaten-down oil companies—offshore driller Diamond Offshore Drilling (ticker: DO) and oil-services company FMC Technologies (FTI) made the list—but so did semiconductor manufacturer Micron Technology (MU), industrial parts supplier W.W. Grainger (GWW), and watch maker Fossil Group (FOSL).

Also making the list: Tiffany (TIF). The iconic jeweler has been battered by the strong dollar, which caused sales in North America to plunge. That’s largely thanks to a drop in spending by foreign tourists, who spent less than they had in the past due to their devalued currencies. No wonder, then, that Tiffany’s stock has fallen 30% so far this year, and now trades at 18.4 times forward earnings, below its 20-year median of 20.7.

Still, Tiffany has a lot going for it. Its overseas sales have been growing at a strong clip, and the jeweler has been able to expand its profit margins—they grew by 0.7% during the third quarter—as it raised prices and benefited from a slumping precious-metal market. The pressure will stay on if the dollar remains strong next year, but if the greenback does turn, the tarnish could come off Tiffany.

LAST WEEK, Keurig Green Mountain (GMCR) announced that it would be bought for $92 a share by a group led by privately held JAB Holding. This was great news for Keurig shareholders, who had watched the stock tumble 61% this year before the deal was announced, and also for Coca-Cola (KO), which was able to turn an ever-so-slight profit on its investment in the coffee company. The purchase, however, continues a trend that goes back at least 10 years—the stock market is shrinking.

Strategas Research Partners’ Jason DeSena Trennert observes that the number of publicly traded companies in the U.S. has fallen to 5,297 from 8,823 in 1997. Yardeni Research’s Ed Yardeni, meanwhile, notes that the share count of nonfinancial companies in the S&P 500 has dropped 7.8% during since the second quarter of 2005, as companies buy back their stock by the bucketful. He also observes a strong link between S&P 500 returns, on the one hand, and the amount of money S&P 500 companies spend on buybacks and dividends. That’s been especially true for companies in the tech and consumer-discretionary sectors, where share count has dropped 16% and 18%, respectively. “This suggests that the EPS impact of buybacks may be more significant at the sector and company levels than for the overall market,” Yardeni says.

I suppose we should be excited that the shrinking market has helped boost returns. But how much has to happen before we ask if something is wrong?

Renova builds 20% stake in Petropavlovsk, fuelling takeover speculation

Renova, the Russia-based holding company of Viktor Vekselberg, has built up a 20% position in the London-headquartered Russian miner Petropavlovsk [LON:POG], The Sunday Times reported. The move, conducted via Renova subsidiaries Lamesa Foundation, Lamesa Group and Polo Company, has sparked speculation of a potential takeover offer, the unsourced report said.

By Friday 11 December, Renova had acquired a 14.8% stake, or 484m ordinary shares, with a further 5.2% comprising 170m loan notes which can be converted to Petropavlovsk stock, the item reported.

Petropavlovsk had a market capitalisation of approximately GBP 205m (USD 311m) at the end of last week, the report noted.

Sunday Times

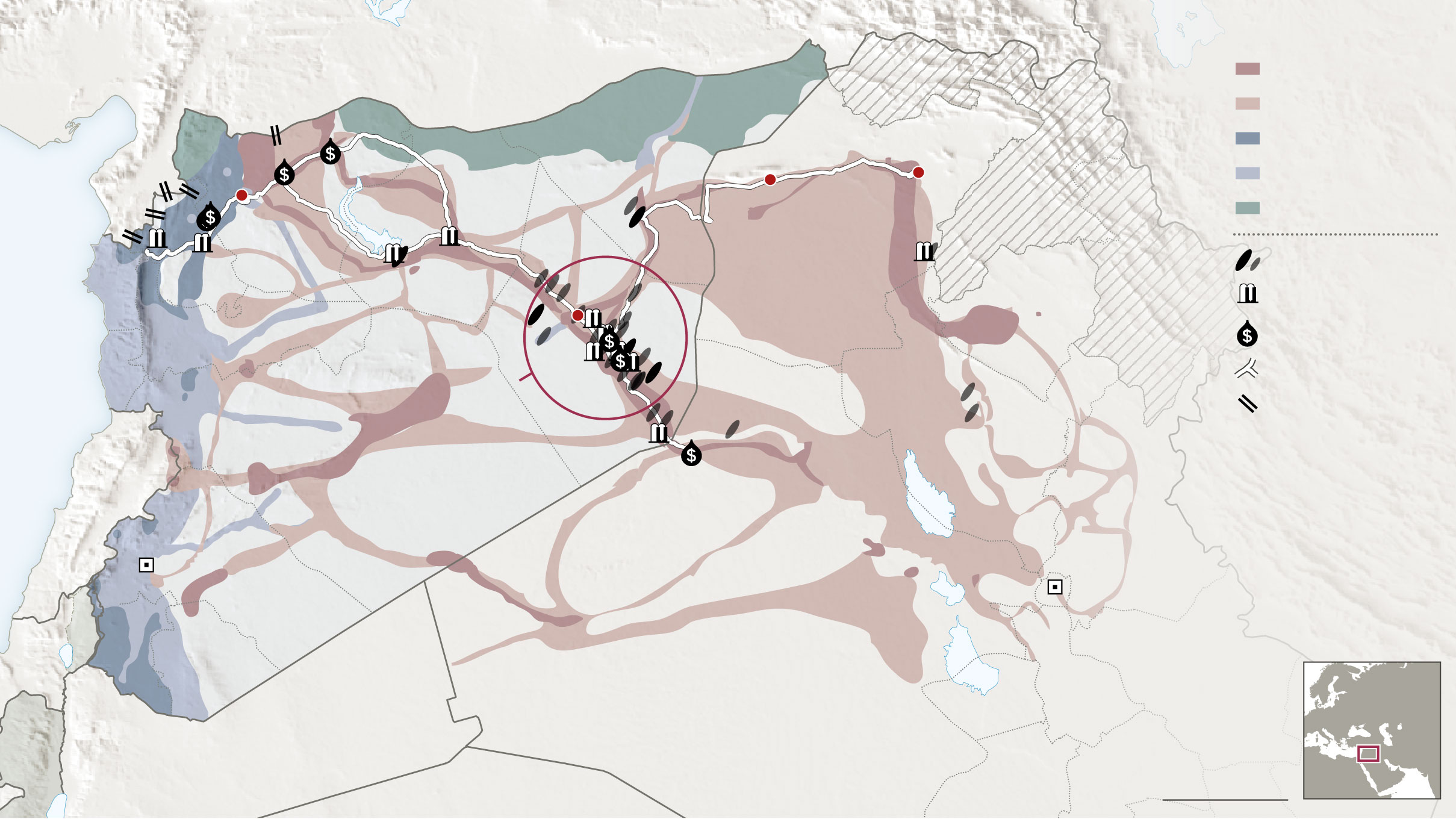

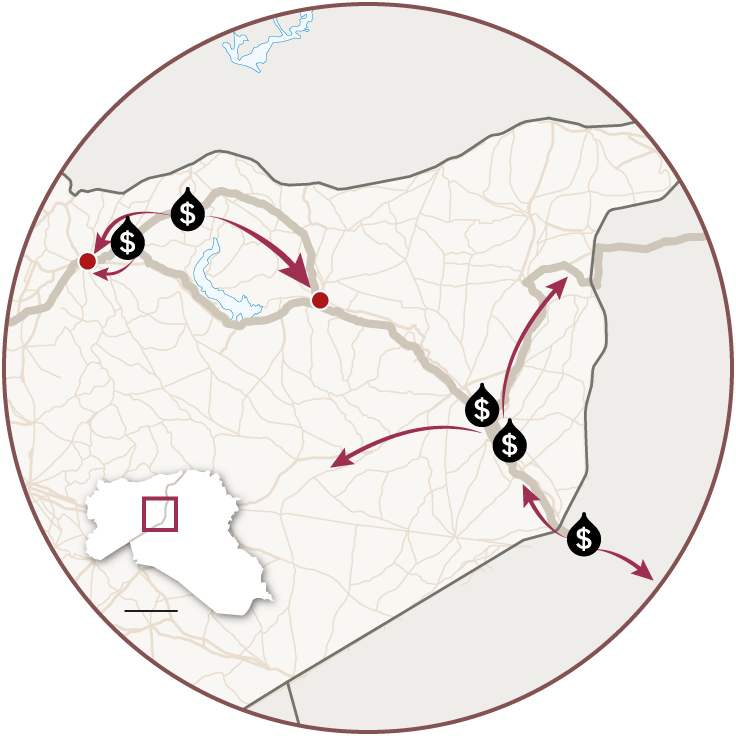

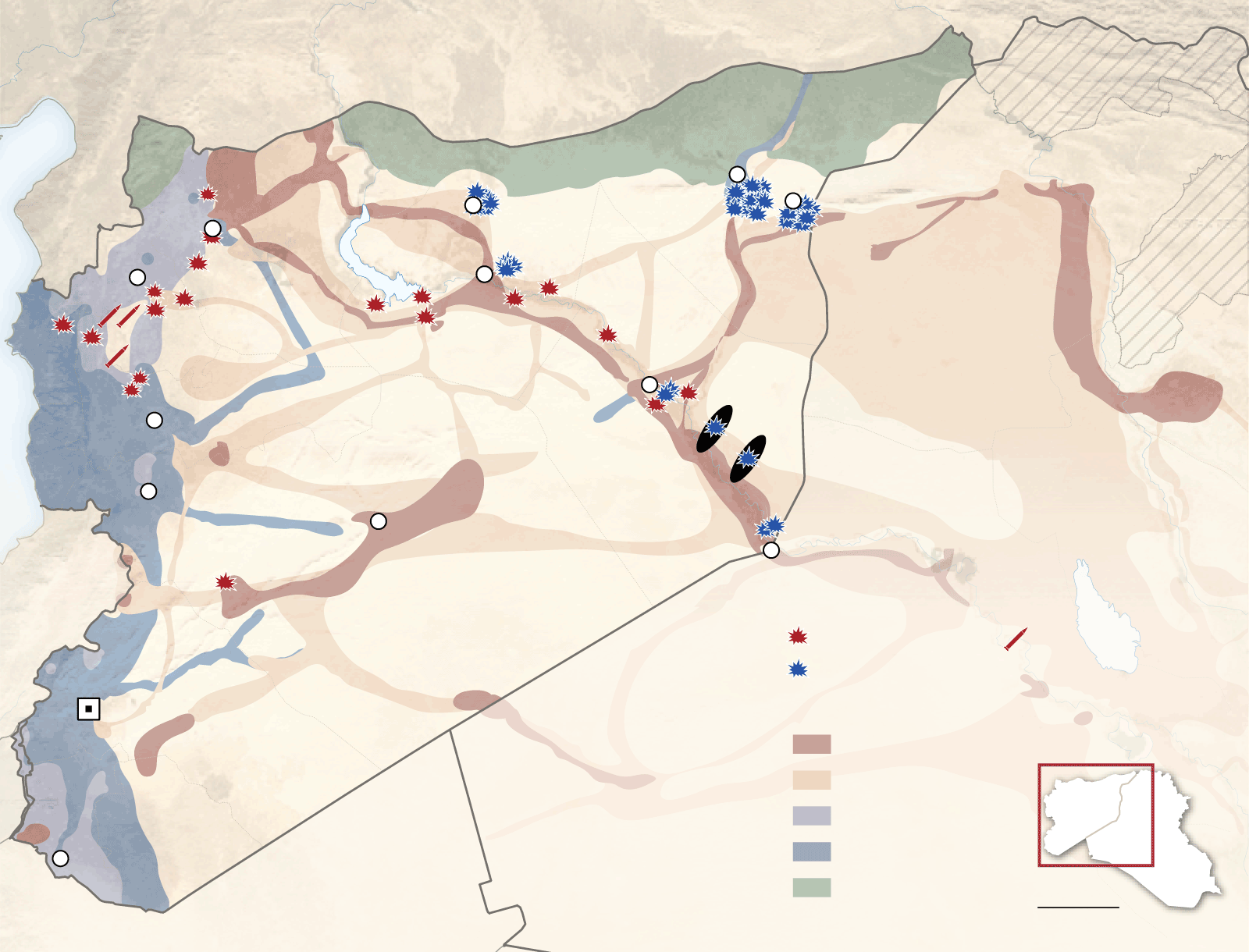

Inside Isis Inc: The journey of a barrel of oil

Territorial controlIsis controlTURKEYIsis supportRebel-heldMosulSinjarSyrian regimeKURDISTANREGIONALGOVERNMENTKurdsAleppoRaqqaOil fieldsMobile refineryDeir EzzorOil marketPrimary oil routesSmuggling routeTargeted by

coaltion airtstrikesal-QaimSYRIALEBANONIRANIRAQDamascusBaghdadISRAELJORDAN100kmSAUDI ARABIAIsis controls most of Syria’s oil fields and crude is the militant group's biggest single source of revenue. Here we follow the progress of a barrel of oil from extraction to end user to see how the Isis production system works, who is making money from it, and why it is proving so challenging to disrupt, even with airstrikes.

By Erika Solomon, Robin Kwong and Steven Bernard•UPDATED December 11, 2015

Where the oil is extracted

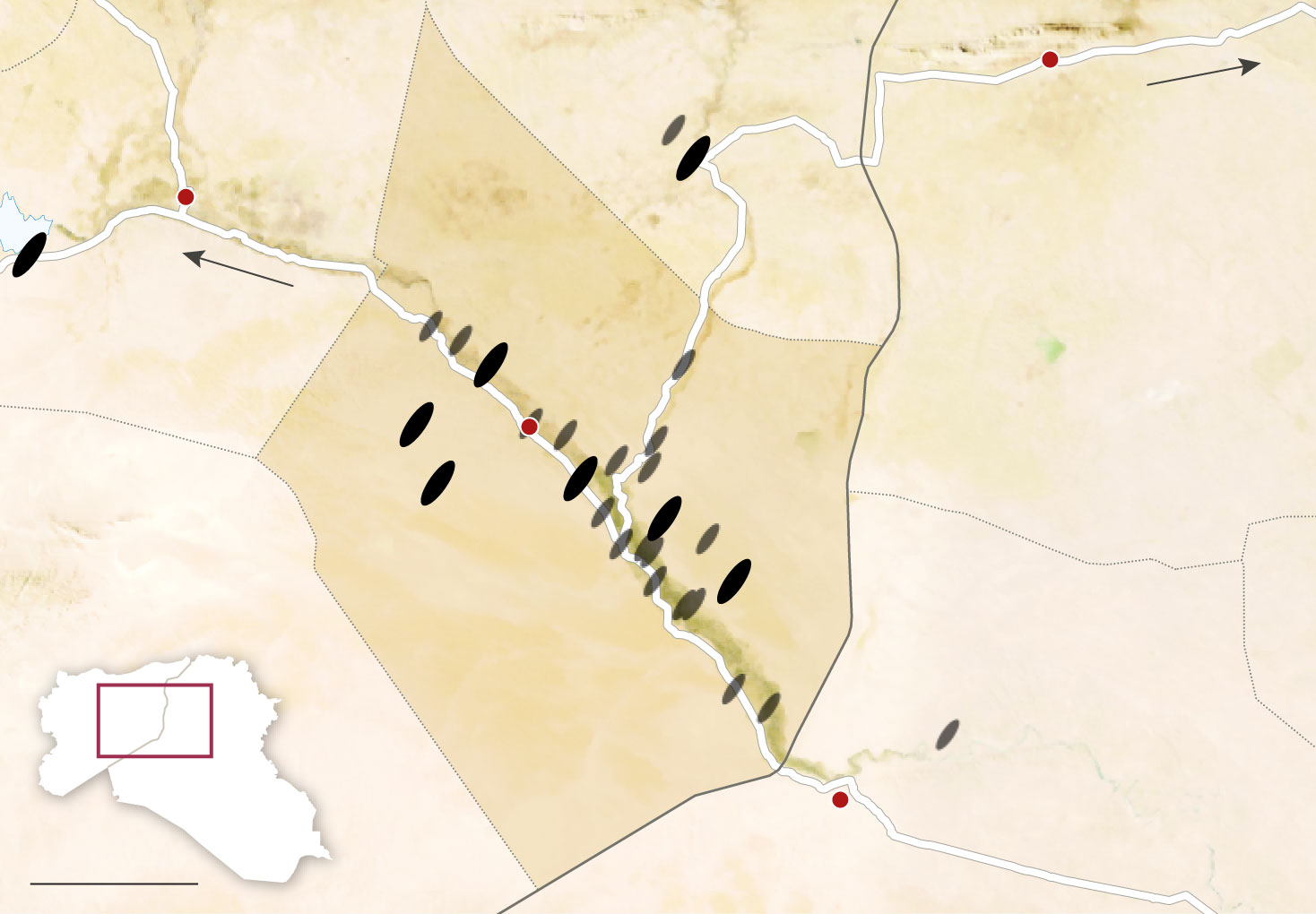

Isis’s main oil producing region is in Syria’s eastern Deir Ezzor province, where production was somewhere between 34,000 to 40,000 barrels a day in October, according to locals. This has since fallen due to coalition and Russian airstrikes against oil facilities. Isis also controls the Qayyara field near Mosul in northern Iraq that produces about 8,000 barrels a day of heavier oil that is mostly used locally to make asphalt.

Sinjar

To Mosul

Raqqa

al-Tabqa

al-Jabseh

To Aleppo

Deiro Field

al-Kharata

Deir Ezzor

IRAQ

al-Omar

al-Shoula

al-Taim

SYRIA

al-Tanak

DEIR EZZOR

SYRIA

IRAQ

al-Qaim

50km

It is difficult to determine a definitive oil production figure for Isis-controlled areas. But it is clear production levels have dropped in the Syrian fields since they were taken over by the militants. Most oil fields in the area are aging and the group does not have the technology or equipment needed to maintain them.

A new air campaign on Isis oil by the US-led coalition started at the end of October and is now more effectively disrupting Isis's crude extraction. Production fell by 30 pct this month at al-Omar and al-Tanak, Isis's two top producing fields and the most targeted by the recent offensive. Up to now, however, it is still likely the most lucrative revenue stream for Isis's central leadership.

The price of the oil depends on its quality. Some fields charge about $25 a barrel. Others, like al-Omar field, one of Syria’s largest, charge $45 a barrel. Overall, Isis is estimated to earn about $1.1m a day.

| Oilfield | Est. production (bpd) | Price ($/barrel) |

|---|---|---|

| al-Tanak | 11,000-12,000 | $40 |

| al-Omar | 6,000-9,000 | $45 |

| al-Jabseh | 2,500-3,000 | $30 |

| al-Tabqa | 1,500-1,800 | $20 |

| al-Kharata | 1,000 | $30 |

| al-Shoula | 650-800 | $30 |

| Deiro | 600-1,000 | $30 |

| al-Taim | 400-600 | $40 |

| al-Rashid | 200-300 | $25 |

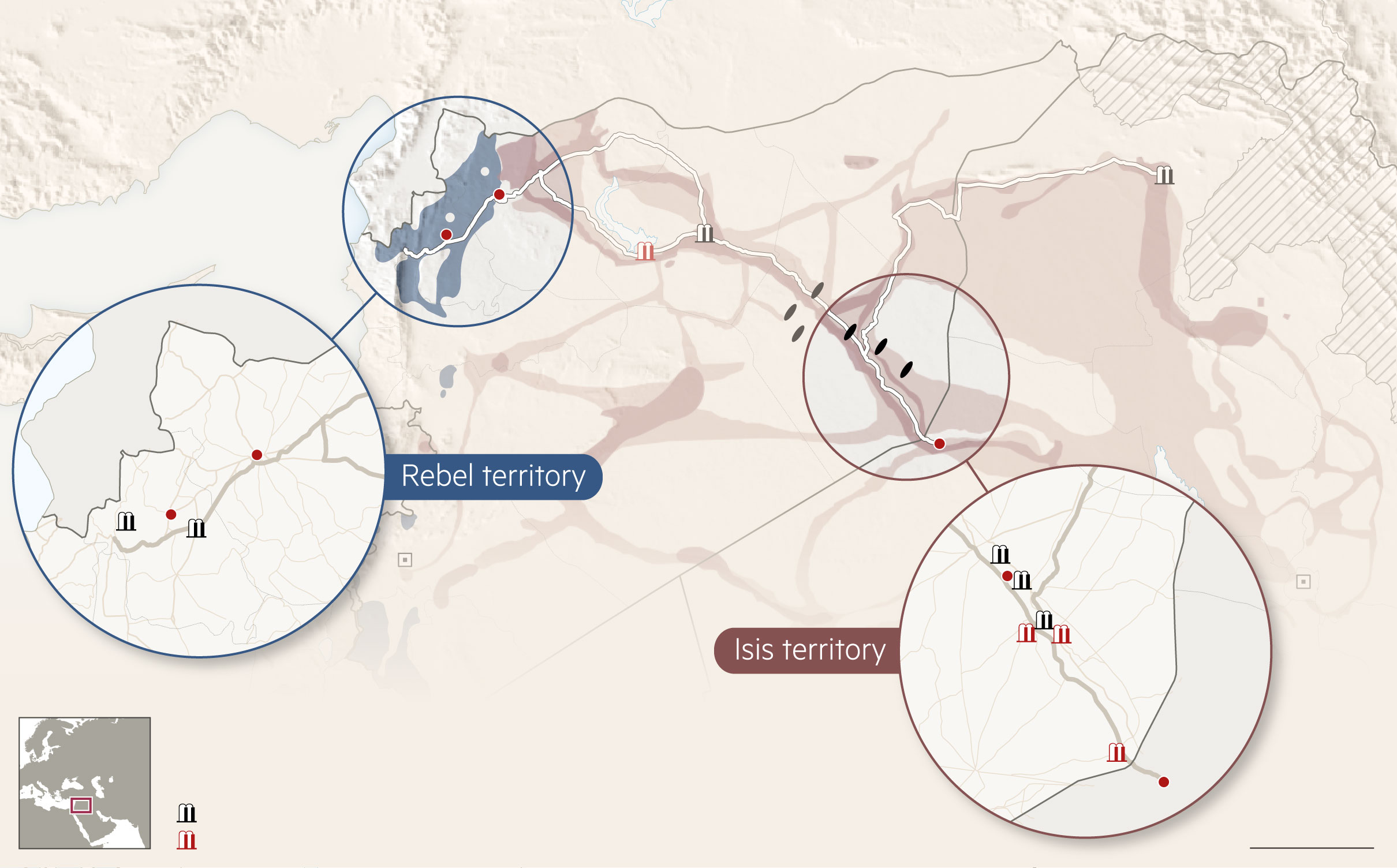

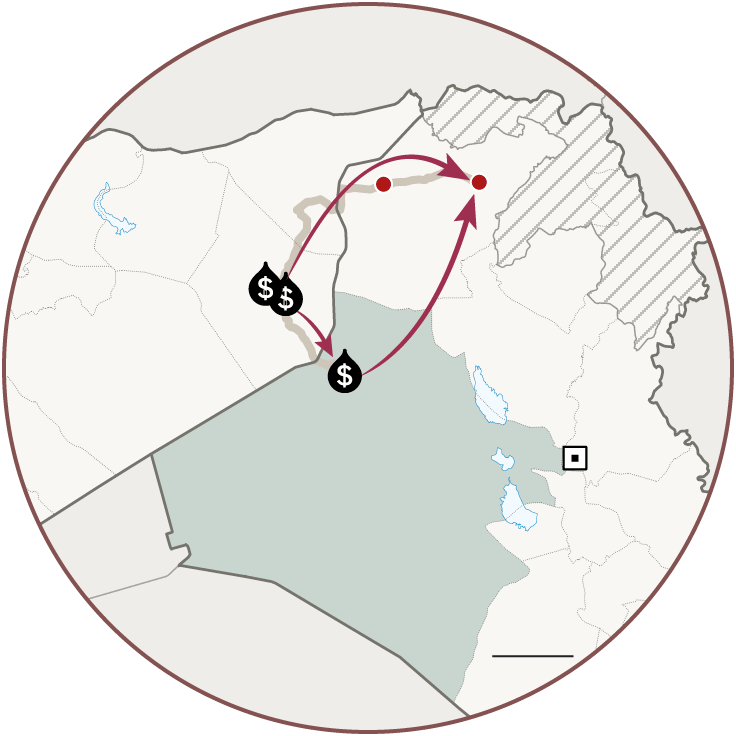

Selling crude oil

Though many believe that Isis relies on exports for its oil revenue, it profits from its captive markets closer to home in the rebel-held territories of northern Syria and in its self-proclaimed “caliphate”, which straddles the border between Syria and Iraq.

The group sells most of its crude directly to independent traders at the oil fields. In a highly organised system, Syrian and Iraqi buyers go directly to the oil fields with their trucks to buy crude. This used to result in them waiting for weeks in traffic jams that sprawled for miles outside of oilfields. But since airstrikes against oil vehicles intensified, Isis revamped its collection system. Now, when truckers register outside the field and pick up their number in line, they say they are told exactly what time they can return to fill up to avoid a pile-up of vehicles and make a more obvious target for strikes.

Oil refineries

Traders have several options after they pick up their cargo:

- Take the oil to nearby refineries, unload it and return to queue at the field—usually done by traders under contract to refineries.

- Sell their oil on to traders with smaller vehicles, who then send it to rebel-held northern Syria, or east towards Iraq.

- Try their luck selling to a refinery or sell it at a local oil market. The biggest are near al-Qaim on the Syrian-Iraqi border.

Most traders prefer to sell the oil on immediately and pick up a fresh number at the fields. They can expect to make a profit of at least SL3,000 (about $10) per barrel.

Traders in Syria's eastern Deir Ezzor province say coalition airstrikes have not targeted their trucks by as much the coalition claims, and say Russia has targeted them more aggressively. Instead the attacks focused on disrupting the extraction process - hitting around the wells or facilities at the oil fields, as well as Isis vehicles. The goal does not appear to be to hit the actual wells but impede efforts to extract from them.

TURKEY

Mosul

KURDISTAN

REGIONAL

GOVERNMENT

Aleppo

Raqqa

Idlib

Tabqa

SYRIA

IRAQ

TURKEY

Aleppo

al-Qaim

Idlib

Saraqeb

Khsham

Jisr

ash-Shugur

Damascus

Baghdad

SYRIA

al-Muhassan

Mayadeen

al-Tayyaneh

IRAQ

SYRIA

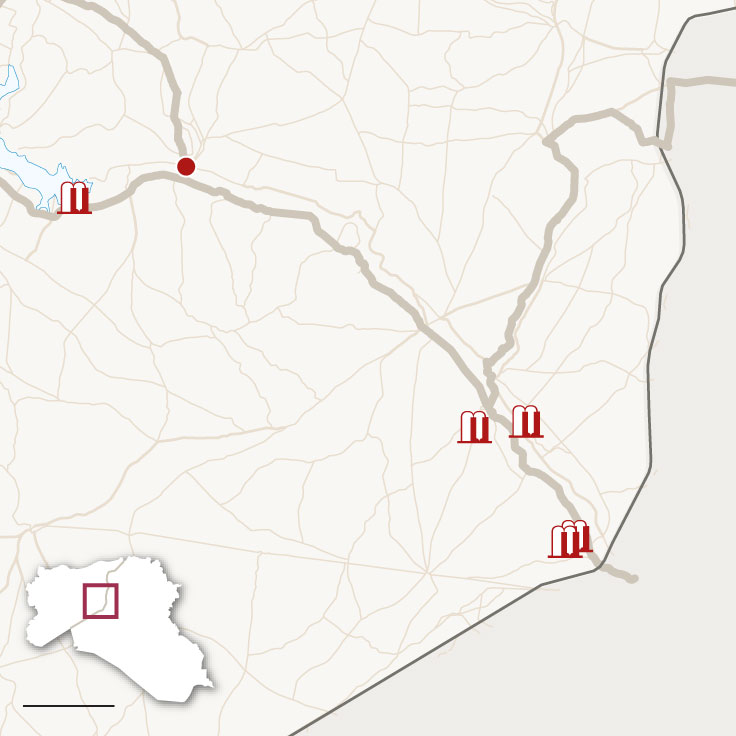

Mobile refineries

Recently bought by Isis

al-Bukamal

al-Qaim

100km

The bulk of oil refineries are in Isis-controlled Syria. The few in rebel-held territories have a reputation for lower quality output than the refineries in the east.

The refineries produce petrol and mazout, a heavy form of diesel used in generators – a necessity as many areas have little or no electricity. Because the quality of the petrol can be inconsistent and is more expensive, mazout is in greater demand.

Refining is done by local residents who constructed their rudimentary refineries after Isis's prefabricated "mobile" facilities were destroyed by coalition airstrikes. The owners make purchase agreements with the militants for their products.

There are also signs that in recent months Isis may have returned to refining. In interviews with traders, the FT discovered the group had bought five refineries since mid-2015.

Raqqa

Tabqa

SYRIA

al-Tayyaneh

Mayadeen

al-Bukamal

SYRIA

IRAQ

IRAQ

40km

At Isis refineries, the former owner stays on as a "front" man. The group supplies the oil; in return it takes all mazout production and splits the profits on petrol production with the original owner.

Traders say Isis has its own tankers that supply crude to its refineries from oil fields regularly. The group also appears to retain many of its earlier contracts with unaffiliated gas stations and other refineries.

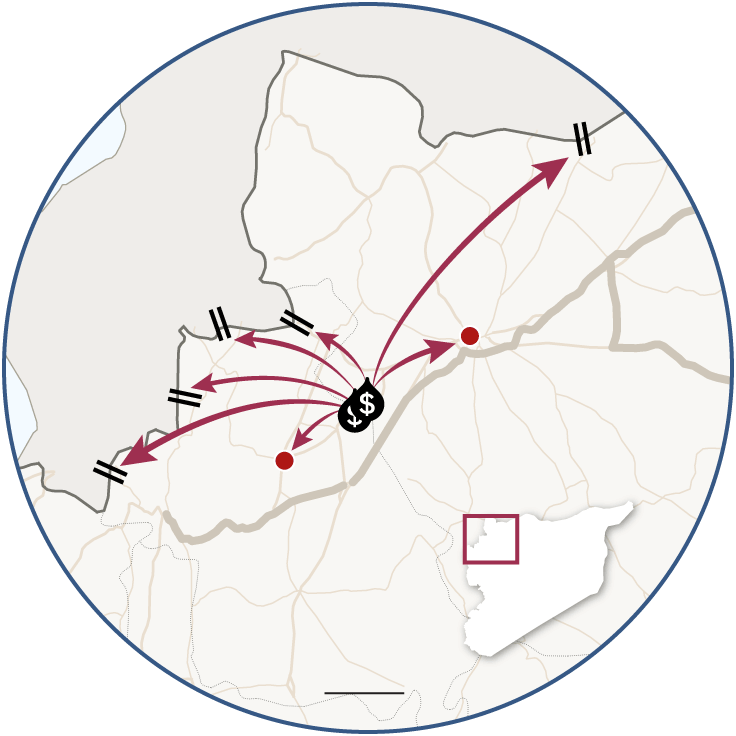

Fuel to market

Once the oil is refined, it is bought by traders or taken by dealers to markets across Syria and Iraq. At this point, Isis is almost completely disengaged from the trade. About half the oil goes to Iraq, while the other half is consumed in Syria, both in Isis territories and rebel-held areas in the north.

There are fuel markets throughout Isis-controlled areas and rebel-held Syria, often located close to refineries. Most towns have a small fuel market where locals buy and sell oil. But traders supplying these smaller markets often buy their oil in bulk from larger hubs.

TURKEY

Manbij

al-Bab

Raqqa

Aleppo

al-Birayha

Theban

al-Qaim

SYRIA

SYRIA

IRAQ

40km

IRAQ

Isis markets

There are larger Isis-controlled markets in towns like Manbij or al-Bab in Aleppo’s eastern countryside. Traders here must present a document proving they have paid zakat, a tithe, to buy oil without tax. Traders from rebel-held Syria who have not paid the tithe, must pay a tax of SL200 per barrel, or about $0.67.

Some privately-owned markets also levy taxes. Al-Qaim market, one of the largest in the region, charges buyers and sellers about SL100 ($0.30) per barrel of crude purchased.

TURKEY

Mosul

KURDISTAN

REGIONAL

GOVERNMENT

Sinjar

SYRIA

IRAQ

al-Qaim

Baghdad

ANBAR

JORDAN

100km

SAUDI ARABIA

Mosul

In Isis-controlled Iraqi cities like Mosul, the fuel is sold at mini “petrol stations” with two pumps. They are ubiquitous on Mosul street corners and locals usually name the oil according to the part of Syria it came from. This helps buyers determine the quality of the oil and compare prices.

Elbeyli/al-Rai

TURKEY

Besaslan

Sarmada

Aleppo

Hacipasa

Kafr Halab

Maarat al-Naasan

Idlib

Kharbet

al-Jawz

SYRIA

20km

Rebel markets

Two types of fuel are sold in rebel-held Syria: pricier fuel refined in Isis areas, and cheaper locally refined fuel. Residents typically buy a mix of both, and use the cheaper variety for generators and keep better quality variety for their vehicles.

Since the airstrikes began, prices of mazout and diesel in rebel-held areas have doubled. Prices of food are higher as well because transport costs are rising.

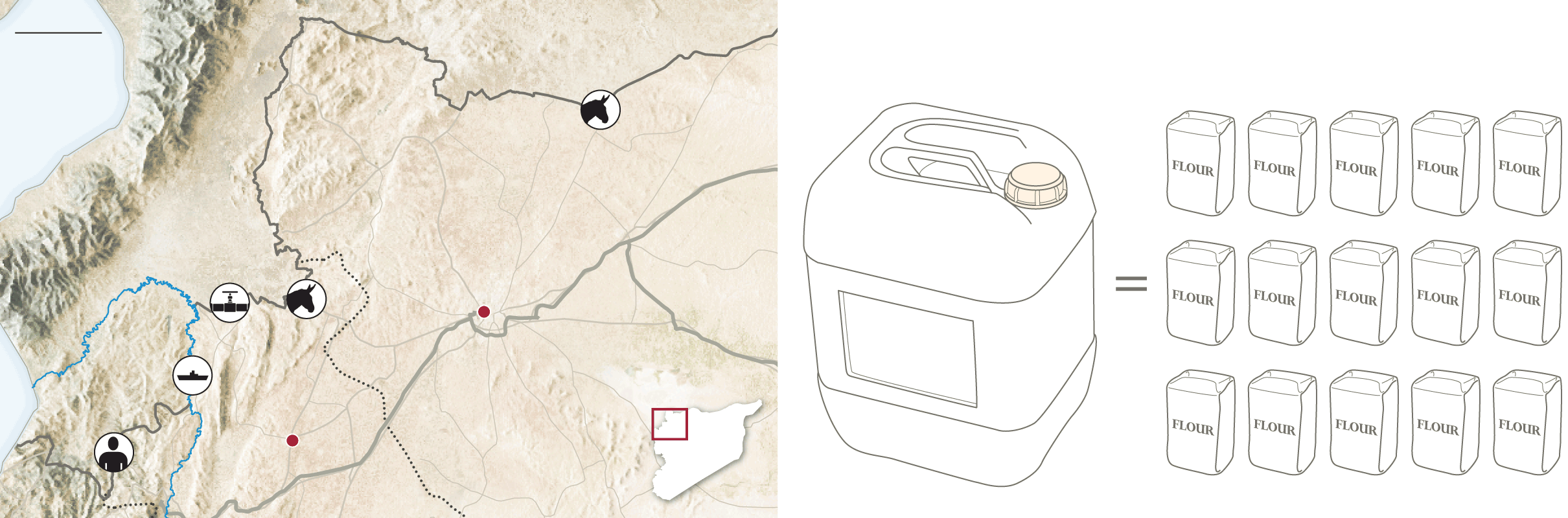

Fuel smuggling

With Isis only concerned with making its profits ‘at the pump’, smuggling fuel into neighbouring countries can be good business for entrepreneurial Syrians and Iraqis. Syrian smugglers say it has been declining in recent months, not because of tighter border controls but because the sharp fall in international oil prices make it unprofitable. But some determined smugglers continue their trade.

Most of the smuggling from the Syrian side has gone through opposition areas in the northwest. Locals buy fuel at the market, pour it into jerry cans and carry it over the border on foot or, in mountainous areas, by donkey or on horseback.

In Iraq, the bulk of smuggling through the northern Kurdistan region has been blocked, so locals say the route now goes south through Anbar province towards Jordan.

25 litre jerry can

20km

Weight when full: approx 22.5kg

Equivalent to 15, 1.5kg bags of flour

al-Rai

TURKEY

SYRIA

Orontes River

Sarmada

Aleppo

Besaslan

Hacipasa

Idlib

Kharbet al-Jawz

Boat

When oil prices were high, smugglers loaded larger jerry cans (50-60 litres) of oil into metal tubs or small row boats and, using ropes attached to each river bank, pulled their cargo across the river and into Turkey. On the other bank, tractors picked up the supply and took it to a local informal market, where it was picked up by large trucks, which sold it on.

When oil prices were high, smugglers loaded larger jerry cans (50-60 litres) of oil into metal tubs or small row boats and, using ropes attached to each river bank, pulled their cargo across the river and into Turkey. On the other bank, tractors picked up the supply and took it to a local informal market, where it was picked up by large trucks, which sold it on.

Pumps

Some Syrian and Turkish border towns have co-operated by burying small rubber tubes under the border, such as at Besaslan. In recent months, Turkey has stepped up border patrols and are constantly digging out the makeshift pipelines.

Some Syrian and Turkish border towns have co-operated by burying small rubber tubes under the border, such as at Besaslan. In recent months, Turkey has stepped up border patrols and are constantly digging out the makeshift pipelines.

On foot

A popular crossing point for smugglers carrying jerry cans of fuel on their backs has been from Kharbet al-Jawz in rebel-held Syria to Guvecci in Turkey. This has been largely shut down by Turkish forces, but the remote terrain makes it impossible to stop.

A popular crossing point for smugglers carrying jerry cans of fuel on their backs has been from Kharbet al-Jawz in rebel-held Syria to Guvecci in Turkey. This has been largely shut down by Turkish forces, but the remote terrain makes it impossible to stop.

Horseback

In places like al-Sarmada and al-Rai, smugglers have crossed the border by mule, donkey or horses that can carry four to eight jerry cans at a time.

In places like al-Sarmada and al-Rai, smugglers have crossed the border by mule, donkey or horses that can carry four to eight jerry cans at a time.

Airstrikes

At the end of October, the US-led coalition launched a fresh assault on Isis oil infrastructure. These airstrikes were followed by Russian attacks, and intensified in mid-November.

The coalition airstrikes against Isis oil operations have mainly targeted the oil extraction process, rather than refineries or oil markets. Bombs have hit Isis vehicles operating at the oil fields, and facilities for pumping or moving oil.

For example, the biggest single blow to Isis oil extraction, locals say, was a strike that took out the machinery that allowed oil workers to centrally control the wells at al-Omar field, Isis's single biggest oil source.

This had been critical because wells there can be 30km away from each other, and the machinery allowed workers to close down a well that was struck and avoid a fire spreading. Now, each well must be operated manually, which dramatically slows down the process of running the entire field.

Strikes on Syria from Nov 20

KURDISTAN

REGIONAL

GOVERNMENT

TURKEY

al-Hasakah

al-Hawl

Ain Issa

Aleppo

Idlib

Raqqa

Deir Ezzour

SYRIA

al-Omar

Hama

IRAQ

al-Tanak

Homs

Palmyra

al-Bukamal

LEBANON

Airstrikes

Russia*

Russian cruise

missiles*

US-led coalition

Damascus

Areas of control

Isis control

Isis support

SYRIA

Rebel-held

Deraa

Syrian regime

JORDAN

IRAQ

Kurds

50km

Sources: Institute for the Study of War, US Central Command,

US Department of Defense, FT research

* Confirmed by local credible reporting

These efforts to stop Isis earning money from oil is starting to have an effect. Production fell by 30 per cent in December at al-Omar and al-Tanak.

But it comes at a human cost. Civilian traders have been hit by an increasing number of strikes. Local civilians are angry about the new campaign and they fear for their own economic survival, which is now entangled with that of Isis's finances.

"This is considered our infrastructure, and destroying it like this...shows that the objective is to kill the Syrian people," says Omar al-Shimali, who lives in the rebel-held Aleppo province to the northwest.

http://thetim.es/1Nq3mm8

Saudi prince hopes to stay at Holiday Inn

THE new owner of the luxury Fairmont and Raffles hotel chains could soon be back on the hunt for big acquisitions, making the FTSE 100 giant InterContinental Hotels Group (IHG) a prime target.

The French owner of Ibis and Sofitel, Accor, bought the Canada-based Fairmont for $3bn (£2bn) last week, the latest in a wave of big-money deals in the industry. Kingdom Holding — the investment fund run by Prince Alwaleed bin Talal of Saudi Arabia — will become one of Accor’s largest shareholders in return for its stake in Fairmont.

The Saudi fund indicated this weekend that it will push for more deals.“Combined, Accor stands stronger and larger and will clearly sit in the predator camp in the prey/predator play,” said Sarmad Zok, chief executive of Kingdom’s hotel arm.

That could IHG vulbnerable to a takeover

Asset managers have raised billions of dollars from investors to lend to companies as fund houses step into an arena traditionally dominated by banks.

European-based fund managers have $41bn ready to deploy in direct lending deals, twice as much as in 2012, according to Preqin, the data provider. This backs up suggestions asset managers are increasingly becoming so-called shadow banks.

The fund management industry has flocked to the direct lending space in the wake of rules introduced since the financial crisis, which have made it less attractive for banks to loan to businesses to the same degree they once did.

Fenton Burgin, partner in the debt advisory practice at Deloitte, the consultancy, said investors struggling to achieve strong returns amid low interest rates are helping to drive the growth of the sector.

Long-term institutional investors are swapping the liquidity of bonds for higher returns by putting money into private debt funds, he said.

Towers Watson, the consultants, said its clients, typically pension funds, have globally allocated more than $7bn to illiquid credit investment strategies, which range from direct lending to property debt, over the past five years.

Chris Redmond, global head of credit at Towers Watson estimates around a third to half of the assets deployed by clients went to direct lending deals. “We view [illiquid credit investment strategies] as an excellent opportunity for investors with a tolerance for illiquidity and a desire to improve overall portfolio efficiency,” he said.

Shadow banking has come under increased scrutiny in recent years amid fears such activities pose risks to financial stability. Mr Redmond played down concerns about the risks investors face from direct lending and other forms of illiquid credit strategies.

Mr Burgin said the direct lending sector is growing quickly. “The development of direct lending as an alternative asset class is ultimately where we think the market will develop over the next 12 to 18 months,” said Mr Burgin.

According to Deloitte, 61 direct loans were made during the third quarter of this year in Europe, up 14 per cent year on year.

KKR, the private equity group, has loaned more than half a billion dollars to companies in Europe this year. A loan to the Casual Dining Group, which is behind the Café Rouge chain of restaurants, is among eight direct lending deals KKR has made in the region this year.

“This is the first year [direct lending] has achieved a critical mass in Europe,” Marc Ciancimino, KKR’s head of European private credit, told the FT.

Last week, Hermes Investment Management, M&G Investments and AIG Asset Management signed an agreement with Royal Bank of Scotland, the UK bank, to co-fund loans of up to £100m.

Assets in the direct lending industry have more than tripled since 2006 to $441bn by the end of last year, according to figures from Brown Brothers Harriman, the financial services group, and Preqin.

Annual Changes to the NASDAQ-100 Index

The following seven companies will be added to the Index: Ctrip.com International, Ltd. (Nasdaq:CTRP), Endo International plc (Nasdaq:ENDP), Expedia, Inc. (Nasdaq:EXPE), Maxim Integrated Products, Inc. (Nasdaq:MXIM), Norwegian Cruise Line Holdings Ltd. (Nasdaq:NCLH), T-Mobile US, Inc. (Nasdaq:TMUS) and Ulta Salon, Cosmetics & Fragrance, Inc. (Nasdaq:ULTA).

As a result of the re-ranking, the following seven companies will be removed from the Index: C.H. Robinson Worldwide, Inc. (Nasdaq:CHRW), Expeditors International of Washington, Inc. (Nasdaq:EXPD), Keurig Green Mountain, Inc. (Nasdaq:GMCR), Garmin Ltd. (Nasdaq:GRMN), Staples, Inc. (Nasdaq:SPLS), VimpelCom Ltd. (Nasdaq:VIP) and Wynn Resorts, Limited (Nasdaq:WYNN).