Albert Edwards sees ‘a multiyear bear market for bonds’

Friday interview: Albert Edwards

Albert Edwards, the provocative and voluble strategist at Société Générale, is known for two things: his long standing “ice age” theory, that the US and Europe will follow Japan into a period of stagnation and deflation, and for being a so-called “permabear” on stocks. Below, he discusses that reputation, the evolution of his long-term view, and the probability that we are still facing a recession and even a deflationary bust. The interview has been edited for clarity and brevity.

Unhedged: There is a critique or caricature of you as a one-note permabear, a clock that is right twice a day. The critics might say you have been bearish all the way through a great run for markets. Please respond.

Albert Edwards: My uber-bear views came about because of my ice age thesis, which I put in place at the back end of 1996. We used to work with Peter Tasker, who was our Japanese strategist at Dresdner Kleinwort, which I joined in 1988. We went through the Japan boom and bust together. And I came to the conclusion that what was playing out in Japan would also play out in the west, with a lag.

The Japanification of the US and Europe was basically like the secular stagnation thesis. In financial markets, cyclicality would de-rate relative to certainty. So equities would underperform government bonds. We’d reach the stage in the economic cycle where the traditional correlation between bonds and equities would break down. As inflation got lower, what you might call the Abby Cohen thesis [after the well-known Goldman Sachs strategist] said that lower bond yields are great for equities because the P/E [price/earnings] ratio will go up forever. But we thought that eventually, as you got down to sub-2 per cent inflation and bond yields fell further, the “P” would start coming down. That’s what happened in Japan.

That was for a couple of reasons. One is at very low rates of inflation, the economic cycle, certainly in Japan, became much more volatile than the profits cycle. So the cyclical risk premium goes up. Secondly, long-term earnings expectations, especially at the end of bubbles, usually became totally detached from nominal [gross domestic product] growth. And as nominal GDP growth got towards zero, we found that long-term earnings expectations collapsed.

So based on the experience in Japan, we thought US bond yields would collapse and once equity valuations finally topped out, you would enter a multiyear valuation bear market in absolute terms. Our bearish call on equities attracts the most attention. But our bond call worked out. The Japanification call worked very well. Our institutional clients understand our calls largely played out, other than the equity bear market.

Unhedged: Why was the equity bear market call wrong?

Edwards: Before the bubble burst in 2000, equity and bond yields had been coming down together. Once it burst, bond yields carried on falling, but equity yields started to rise from 2000. That decoupling was what I expected. But where my ice age call stopped working was from 2008 onwards when quantitative easing kicked in. Hosing money out for QE re-coupled equity and bond yields, which started falling together again.

Unhedged: So QE changed your view on equities. What else has changed, in your mind, since the ice age argument was first made in 1996?

Edwards: Another thing I got wrong was cycles didn’t become more volatile. The [Federal Reserve] stepped up the gear in manipulating the cycle. And you got the longest economic cycle in US history, prior to the 2020 pandemic recession.

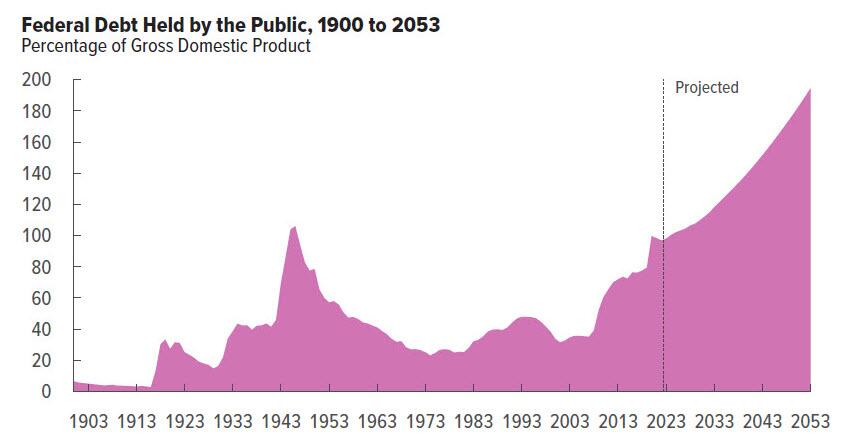

Before the pandemic, I had written that the next recession, when it comes, would end the ice age thesis. I thought that in the next recession, we would cross the Rubicon into MMT [modern monetary theory, the idea that capacity constraints, not budget constraints, are the relevant limit on government spending]. I didn’t realise it would be so easy! I didn’t realise you would get the level of populism around the world that we got, because of inequality. And I thought the next recession would be a deep one, because if you remember, in 2019, there was an incredible corporate debt bubble. That would force US authorities to step in aggressively. They did end up being aggressive, but it was because of the pandemic, which eliminated opposition to crossing the fiscal Rubicon.

In the global financial crisis, the US injected liquidity into the veins of Wall Street, so narrow money measures exploded but broad money didn’t. In the pandemic, they also did it into the veins of Main Street, printing money for direct transfers. That was bonkers; even the MMTers should’ve seen that. Given the capacity constraints, [inflation was sure to follow].

I had said the next recession would be the end of the ice age, and we would enter a multiyear secular trend of higher highs and higher lows for bond yields, inflation and interest rates. I had thought this would occur, but not as rapidly as it did.

Unhedged: Given higher highs and higher lows for rates and inflation, how do risk assets respond to that?

Edwards: Even though the ice age call didn’t work for the overall equity market, it was relevant within the equity market. Bond-sensitive sectors, such as defensives and growth, did incredibly well, relative to cyclicality and value. So if you’re an equity-only investor, the direction wasn’t right, but the sector allocation within equities was absolutely spot on.

Within equity markets, particularly the US, they’ve become much more dominated by tech and bond-sensitive stocks, which benefit from lower bond yields. Apart from last year’s [artificial intelligence] narrative-driven rally, which supported tech despite rising yields, defensiveness has come to dominate the stock indices, which is what you’d expect after a multiyear bull market in government bonds.

Going forward, if my “great melt” thesis is right and we’re entering a multiyear bear market for bonds, it’s pretty problematic for equity markets dominated by bond-sensitive sectors, like the US, which have been lifted by falling bond yields. You’ll need really rapid earnings growth for tech stocks to power through higher bond yields.

Unhedged: Summing it up very simply, then, the great melt thesis amounts to fiscal incontinence → higher inflation → higher rates → trouble for rate-sensitive stocks. Is that right?

Edwards: That’s right. With tech back up to 31 per cent of total US market cap, a level only surpassed for a few months around September 2020, so much of [US stock outperformance] has been multiple expansion. Up until the Powell pivot in 2018-19 [when Jay Powell’s Federal Reserve switched from raising to lowering rates], tech wasn’t at a particularly substantial P/E premium relative to the market. After the Powell pivot, then it went bonkers, and even more bonkers during the last recession.

The big call I’ve made is that if a recession comes along, you’ll get lower bond yields, but that won’t benefit tech. What really destroyed tech in 2001 is that you’d had many years of good, strong earnings growth. Lots of those companies hadn’t been around for a very long time. The market didn’t really know what was cyclical and what was growth. Investors took the internet story and re-rated most stocks to be on growth valuations, even if they were cyclicals. Then recession came along. Stocks on 40x P/E suddenly had falling earnings. So people went, well, seems like we got both earnings and multiples wrong. The whole sector collapsed. I think this is the biggest risk for equities: that a recession exposes vast portions of tech as cyclicals masquerading as growth stocks. So lower bond yields don’t save them. You get a step derating and the baby gets thrown out with the bathwater.

Unhedged: But isn’t there a difference of degree between the dotcom boom and now? Back then, you had Cisco trading at 100 times earnings. Now, you have the Big Techs trading at, say, 27 or 30. There’s a big difference between 100 and 27.

Edwards: Absolutely. I’m not saying they collapse to the extent they did in 2001. But the same qualitative argument applies. We saw it in 2022, when we had profit disappointments. Tech was really hurting in 2022, until ChatGPT came along at the end of the year. If you look at tech trailing earnings relative to the market in 2023, they haven’t done so well. Forward earnings have gone up, but trailing earnings haven’t really. It’s a story which has yet to deliver.

If tech wasn’t 31 per cent of US market cap, you wouldn’t really worry. But it is. A tech collapse wouldn’t be like a traditional bear market where you’d get rotation out of cyclicality into defensiveness and growth. Maybe you get that flight out of cyclicality in the next recession, and defensiveness gets squeezed up to the moon, to a ridiculous valuation. This was the point Peter Tasker always used to make. One of the lessons from Japan was the extremes of valuation that defensives reached in the crisis. People wanted certainty and safety.

Unhedged: Japan’s crisis was deflationary, though.

Edwards: The monetarists were right in the wake of the pandemic. Look at broad money — Divisia M4 in the US. It rocketed up in the pandemic. MMT believers should have been screaming about capacity constraints. Stephanie Kelton’s book [The Deficit Myth] says you can print money to finance deficits until near the end of the cycle, when you hit capacity constraints. So the MMTers should have been screaming: don’t do this! This is going to create inflation! This was, if you like, the experiment during the pandemic, and monetarists were right. [The money printing] created inflation.

The monetarists are now saying that the broad money supply measures have collapsed, contracting at a rate consistent with a collapse from inflation into deflation. And the problem is all these central bankers have purged money supply not just from their models, but from their thinking. They’re very open about that. If you don’t like money supply, look at bank lending data. If the monetarists are right, if we get a recession now, it could be a deflationary bust. Now, that doesn’t negate the secular story, which is that the fiscal diarrhoea is there, and that can’t be and won’t be unwound because there’s no political will to retrench.

Unhedged: In a slowdown, you should expect to see pretty considerable margin compression. Suddenly demand is a lot more elastic. Companies start competing on prices again. That is supposed to lead to a potentially non-linear decrease in inflation, but it didn’t happen. We did get two quarters of pretty weak US GDP in the first two quarters of 2022, and there was a little bit of margin compression. But not that much. Why?

Edwards: What always causes recession is the business investment cycle. It’s only about 15 per cent of US GDP, but it’s so darn volatile. If you don’t get business investment downturns, you would not get recessions at all.

A lot of economists, like me, think business investment leads the economic cycle. So profit growth slows down and turns negative, and with a lag business investment follows. And then, with a bit of a lag, employment follows that. Whole economy profits did slow down year on year to zero. And business investment activity, including inventories, did slow down to zero year on year, without going negative.

What helped offset that? Margins stayed relatively high. Partly, that was because consumers had not worked through their savings, so companies didn’t feel compelled to cut their margins. Plus the fact that it was so difficult to hire workers during the pandemic. You just spent 18 months finding John Doe to fill that job gap; you’re not going to rush to fire him in this downturn. Plus, you have the rotation out of goods consumption during the pandemic into services, which are more labour intensive, so the labour situation held up better than it normally would. That helped underlying demand.

Unhedged: Can you put these points about the profit cycle in the context of the ice age and great melt theories?

Edwards: The initial burst of inflation was due to the factors which will continue to drive it: the monetary financing of fiscal incontinence. And then you had this one-off occurrence of price gouging. Interest rates ended up rising higher than they would’ve otherwise, because of profit-led inflation. What the regulators should have done was find some of the worst cases and go after them. That would’ve been a signal to everyone else.

But I do think margins clatter downwards as you go into this recession. Whole-economy margins are still at very elevated levels. Greedflation has delayed the recession. Lower net interest payments [from companies locking in low rates] have delayed the recession. But you drill down below the mega caps and the large caps, and bankruptcies for 2023 are up 72 per cent year on year. The level is surpassing that of 2020, before they put the bailout measures in place.

Below the top 100 companies, the corporate sector is in incredible pain, especially the unquoted sector. Eventually, as these zombie companies go bankrupt, this is what will start increasing [the chances of recession].

Unhedged: Accepting your views about the long-term trends, what does a rational institutional or individual portfolio look like right now? How do we translate your worldview into a portfolio?

Edwards: What we’re saying to clients is that a recession is coming. This has been the most predicted recession in history, and people have got it wrong, so they tend to give up. But I’m not embarrassed to get things wrong. I think it could be deeper than people expect. The zombie company effect could make it more severe, because it’s being delayed for so long.

I think a rational portfolio is still leaning towards an ice age-style allocation in the near term. The cyclical risks warrant leaning towards defensiveness and bond-sensitive stocks. But be very, very careful of tech, as we discussed. Expect US 10-year bond yields probably to end up with a “1” in front of them, though a low “2” is plausible, too. My view is that yields revert to a higher low, not the low-lows of the pandemic era.

Expect headline inflation of zero, and core inflation to come down. Apartment completions this year are just off the scale. Rents are going to absolutely collapse. So even the normal core inflation ex-food and energy could come down, because of the rent component. And core CPI ex-shelter is already below 2 per cent year on year.

So I think it’s a bond-friendly environment cyclically. But I would use this recession [when it comes] to rotate into cyclicality and value stocks on a strategic basis and rotate the portfolio away from bond-sensitive stocks.

Unhedged: And after the recession?

Edwards: I actually think in the next cycle, we could end up in the US with yield curve control [central bank bond-buying aiming to cap long-term bond yields]. There is no way there is going to be fiscal consolidation. For populist reasons, no politician has the stomach to do it, they will just be voted out. The Fed will be forced by politicians to hold down bond yields.

But what I would say, and I think this goes for everyone, is I think the short-term cyclical outlook is incredibly uncertain, more uncertain than normal. But in the medium term, think of the maddest thing you could think of, and actually, you might not be so wrong.