Apple is recruiting experts in automotive technology and vehicle design to work at a new top-secret research lab, said several people familiar with the company, pointing to ambitions that go beyond the dashboard.

Friday’s news of a secret research lab in the FT there, which stirred the froth around Tesla, the electric car company run by Elon Musk. A $75bn takeover target for Apple, anyone?

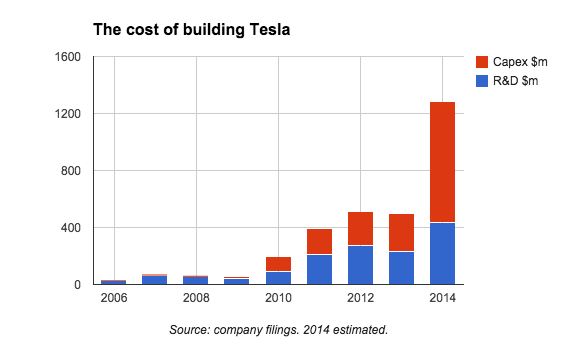

The problem with the theory, aside from Tesla’s mere $25bn market capitalisation, is that nobody really needs to buy Tesla. Might someone? Sure, but a glance at the company’s history shows just how little cash it took to build.

The first vehicle was the Tesla Roadster, a proof of concept sports car. Total capital expenditures and research and development costs from inception to the day of the first delivery ran to about $125m.

Production of a high-end sedan followed, and the development of manufacturing facilities in Palo Alto, California, was helped by a $465m loan facility from the Department of Energy, agreed in 2010 and drawn down in stages.

Tesla also struck deals with Daimler and Toyota to help fund the development of what is known as powertrain technology — the combination of battery, engine, gearbox, clutch and management software that makes an electric car move — and with Panasonic for batteries.

One thing to realise, however, is the simplicity of the electric motor invented by Nikola Tesla compared to an internal combustion engine. The challenge is transferring the power to the wheels smoothly, as well as managing and prolonging the battery life. So far as engineering problems go, it is more a question of people and resources than reinventing the wheel. Tesla has also offered to share patents with the industry on fair terms.

So let’s say you wanted to start an electric car company (or division) from scratch. Here is what Tesla has spent on research and development and capital expenditures:

The 2009 R&D figure includes a $23m contribution from Daimler, but that makes little difference to the overall total of $3.1bn.

More spending is in prospect, with a planned battery “Gigafactory” expected to cost $4bn to $5bn by 2020, of which Tesla will contribute about $2bn, or about $400m a year. Also remember that Tesla was helped out early on by taking over a factory formerly owned by General Motors and Toyota, and you wouldn’t have Elon Musk running the show.

Still, if you think all cars will one day be electric (and driverless), there is time to catch up.

You would have to find staff, but assuming you are a well resourced multi-national company to start with, the numbers aren’t daunting. At the end of 2009, Tesla had 514 full time employees: 142 in manufacturing, 120 in research and development, 71 working on vehicle design and engineering, 83 in sales and marketing, 35 in services, and 63 general and administrative staff. Four years later the total had grown twelvefold to almost 6,000 employees.

Set up your secret research lab and start writing cheques. Lets say you want to do it fast (four to five years) and can throw money at the project. Do you plan to spend double what Tesla did to get to this point? Triple? Even if you did (and weren’t able to find supportive governments, carmakers and battery makers to get involved) you’d still have spent less than a third of what it would cost to buy Tesla outright.

A budget of $1bn to $2bn a year is not exactly small, but aluminium milling specialist Apple already spends $6bn a year on R&D. Google, the online advertising company with a sideline in driverless car technology, spends $10bn annually. In 2013 Volkswagen invested €11bn ($13bn) in property, plant and equipment, and capitalised a further €4bn ($5bn) of research spend.

Or to put it another way, Tesla is a good electric car brand but is unlikely to be the only good electric car brand come 2020. While it has a head start, buying it would be an expensive and unnecessary way to catch up.

Daimler Seeks Approval for Possible 10% Share Buyback

2015-02-17 14:29:14.956 GMT

By Dorothee Tschampa

(Bloomberg) -- Share repurchase authorization to be valid

through March 31, 2020, and would replace five-year clearance

expiring in April 2015, co. says in invitation to annual

shareholders meeting.

* Buyback can be made via stock exchange, public offering or

derivatives

* Co. also seeks authorization through March 2020 to sell as

much as EU10b in convertible bonds or bonds with warrants

with maximum 10 yr maturity

* Daimler proposes supervisory board member Paul Achleitner

for re-election

* NOTE: Annual meeting is scheduled for April 1 in Berlin

* NOTE Feb. 5: Daimler Quarterly Profit Beats Estimates on S-

Class Demand

For Related News and Information:

First Word scrolling panel: FIRST<GO>

First Word newswire: NH BFW<GO>

To contact the reporter on this story:

Dorothee Tschampa in Frankfurt at +49-69-9204-1214 or

dtschampa@bloomberg.net

To contact the editor responsible for this story:

Chris Reiter at +49-30-70010-6226 or

creiter2@bloomberg.net

2015-02-17 14:29:14.956 GMT

By Dorothee Tschampa

(Bloomberg) -- Share repurchase authorization to be valid

through March 31, 2020, and would replace five-year clearance

expiring in April 2015, co. says in invitation to annual

shareholders meeting.

* Buyback can be made via stock exchange, public offering or

derivatives

* Co. also seeks authorization through March 2020 to sell as

much as EU10b in convertible bonds or bonds with warrants

with maximum 10 yr maturity

* Daimler proposes supervisory board member Paul Achleitner

for re-election

* NOTE: Annual meeting is scheduled for April 1 in Berlin

* NOTE Feb. 5: Daimler Quarterly Profit Beats Estimates on S-

Class Demand

For Related News and Information:

First Word scrolling panel: FIRST<GO>

First Word newswire: NH BFW<GO>

To contact the reporter on this story:

Dorothee Tschampa in Frankfurt at +49-69-9204-1214 or

dtschampa@bloomberg.net

To contact the editor responsible for this story:

Chris Reiter at +49-30-70010-6226 or

creiter2@bloomberg.net

--> +0.9% Pre mkt

Mead Johnson Nutrition beats by $0.04, reports revs in-line; guides FY15 EPS below consensus

Reports Q4 (Dec) earnings of $0.92 per share, excluding non-recurring items, $0.04 better than the Capital IQ Consensus Estimate of $0.88; revenues rose 3.2% year/year to $1.09 bln vs the $1.1 bln consensus.

- Constant dollar sales increased 8%; 5% from price and 3% from volume. Foreign exchange adversely affected sales growth by 5%. Gross margin was lower than the prior year quarter due mainly to higher dairy costs and adverse foreign exchange. Earnings before interest and income taxes were also negatively impacted by unfavorable MTM adjustments due to updated actuarial assumptions. EBIT totaled $209.6 mln in Q4 of 2014, compared to $203.9 mln for the comparative period in 2013.

- "As we enter 2015, we face significant headwinds from a strengthening dollar. Approximately three quarters of our revenue is in foreign currencies while much of our cost base is dollar denominated. As a result, our earnings are somewhat exposed to currency fluctuations. Lower commodity costs will, however, allow us to improve gross margins and invest incrementally behind our brands."

RTRS - GREEK PM SAYS PEOPLE CAN NO LONGER TREAT GREECE LIKE A COLONY OR A PARIAH IN EUROPE

China Considering Mergers Among Its Big State Oil Companies

Government economic advisers are conducting a feasibility study of options for consolidation

At the request of China’s leadership, government economic advisers are conducting a feasibility study of options for consolidation, according to officials with knowledge of the research. One involves potentially combining the country’s largest oil companies, China National Petroleum Corp., or CNPC, and its main domestic rival, China Petrochemical Corp., or Sinopec, the officials said. Other options look at merging two other major energy companies, China National Offshore Oil Corp., or Cnooc, and Sinochem Group.

No timetable has been set for a decision on whether or when to proceed with the various proposed mergers, said the officials. Spokespeople for the four Chinese oil companies and the State-owned Assets Supervision and Administration Commission, which oversees the largest state enterprises, declined to comment or didn’t respond to queries.

The possible mergers would be the latest consolidation of state companies blessed by the government as it tries to regear a slowing economy for a new phase of growth. As part of that effort, President Xi Jinping , now more than two years in office, is trying to revamp major state firms to make them more competitive globally.

Though the government has taken some tentative steps to allow more private and foreign capital to flow into infrastructure, resources, banking and other areas long the preserve of state firms, Mr. Xi has said state companies remain an “important pillar of the national economy.” The government “must ensure they thrive,” Mr. Xi said in remarks in August. Bigger and stronger state companies, according to officials and scholars familiar with the leadership’s thinking, are viewed by Mr. Xi as key to China’s reclaiming its prominence in the world.

Mergers could also boost efficiencies in an economy increasingly burdened by excess capacity—a problem that has caused Chinese manufacturers to compete against one other by cutting prices. Late last year, the government announced a plan to merge the country’s top two state-owned railcar makers with a goal of making the combined company capable of competing with Siemens AG in Germany and Canada’s Bombardier Inc.

The four oil companies—CNPC, Sinopec, Cnooc and Sinochem—have long dominated every phase of the industry; for years each had a geographic or business area of specialty. For instance, CNPC focused on exploration and production, and Sinopec on refining. Over the past 15 years, in response to earlier reform plans to spur competition, they’ have expanded into the others’ turf, creating overlapping operations that span exploration, refining to running gas pumps.

“They’re increasingly fighting among each other,” said one of the officials with knowledge of the consolidation plan. “That has led to lots of waste and inefficiency.”

With international oil prices having halved in less than a year, those problems have become more pronounced, giving reform new urgency. Combining and then streamlining the operations of the major Chinese oil producers could help reduce waste caused by redundant staff and projects, the officials said. A combined enterprise could then focus on building up a better-funded company to compete around the world.

Low oil prices have spurred talk of new deals activity across the globe, as stronger companies engage in opportunistic buying of weaker firms. Among big deals last year, Spain’s Repsol SA agreed to acquire Canadian oil-and-gas producer Talisman Energy Inc. for $8.3 billion.

“We want to create a big Chinese brand to better compete overseas,” the Chinese official said. “We want our own Exxon Mobil.”

The potential shake-up would cap what has been a tumultuous period for China’s oil industry. Chinese oil giants—in particular CNPC—have been the focus of an antigraft campaign championed by President Xi. Leading industry executives have been detained for suspected graft, and added scrutiny has helped spur a huge pullback in new investment by wary executives.

A decision to consolidate China’s oil sector by making big state firms even bigger could end up tamping competition at home and stymie market-oriented reforms, some analysts said. It is unclear whether a possible consolidation would be followed by reforms, such as lowering barriers that have marginalized independent oil-and-gas producers.

“If you are focused on the foreign market, you certainly want to consolidate because it’s more competitive abroad,” said Lin Boqiang, director of the China Center for Energy Economics Research at Xiamen University. “But if just for the domestic market it’s better to have more competition, because competition leads to efficiency.”

Beijing has started inviting private capital into the oil industry. Sinopec last year sold a nearly 30% stake in its retail sales-and-marketing unit to a group of 25 investors, mostly Chinese. But none of the initiatives involves selling a controlling stake to the private sector.

A bigger challenge is whether the government would allow the combined entities to improve performance by reducing their huge workforces or shedding assets, said Philip Andrews-Speed, an expert on energy governance in China at the National University of Singapore. “That will be the test of whether this is old state-ism ... or are they really looking for better performance,” he said.

PetroChina Co. , the listed arm of CNPC, has nearly 550,000 employees world-wide, more than seven times as big as Exxon Mobil Corp. The Chinese company delivered revenue of $361 billion in 2013, compared with more than $420 billion in sales and other revenue at Exxon.

These days, all of China’s big oil companies have been under pressure from prices and from the government to cut costs and focus on improving returns. For example, Cnooc Ltd. , the listed unit of China National Offshore Oil, says it will cut capital spending by as much as 35% in 2015 as a result of falling global oil prices. Expenditures at PetroChina and Sinopec are also expected to fall this year.

Marrying CNPC and Sinopec would create one of the world’s biggest companies. A combined entity at least in the short run could control a vast majority of China’s onshore oil-and-gas production and would hold total assets of hundreds of billions of dollars.

In the case of Cnooc, a merger with Sinochem, would give it more refining operations, giving it more sources of revenue that over time could help shield it against oil-market volatility. Cnooc is regarded by analysts as the most vulnerable to the oil-and-gas price drop, in part because it expanded aggressively abroad, buying assets including Canadian oil-sands operator Nexen Inc. for $15.1 billion in 2013 when prices were high.

*HUTCHISON TALKS TO MERGE WITH WIND IN ITALY SAID TO ACCELERATE

2015-02-17 14:03:47.50 GMT

--KENNETH WONG

-0- Feb/17/2015 14:03 GMT

2015-02-17 14:03:47.50 GMT

--KENNETH WONG

-0- Feb/17/2015 14:03 GMT

InterContinental Hotels Group has promised shareholders an 11 per cent boost to its final dividend, despite warning of rising geopolitical and macroeconomic uncertainty in the coming year.

The world’s largest hotel operator by number of rooms reported revenue per available room rising 6.1 per cent for the year to December 31, driven by 7.4 per cent growth in the Americas, where it makes most of its profits.

However, its shares had fallen back 5 per cent by lunchtime London trading on Tuesday to £24.55.

“The markets where we are earning the great majority of our profits are not necessarily exposed to macroeconomic and geopolitical uncertainties, but the world is becoming riskier,” said Paul Edgecliffe-Johnson, chief financial officer.

The results cap a busy year in which it saw off an informal takeover approach and pressure from activist shareholder Marcato.

Mick McGuire’s Marcato hedge fund, which owns about 4 per cent of the FTSE 100 company, has called for IHG to seek a tie-up with an American rival to allow an “inversion” of corporation tax if the US group moved its headquarters to the UK, where IHG is based.

Richard Solomons, chief executive of IHG, said that while there was “theoretical” value in mergers in any industry, the company was focused on a strategy of organic growth.

“We have delivered more total shareholder returns ahead of anyone else in our industry in the past 10 years, and if someone is interested in our business then it’s up to them to talk to us. But we’re confident in our strategy and that’s what we’re working on,” he said.

Weaker trading in China in the fourth quarter and the lack of news on the anticipated sale of the InterContinental Hong Kong hotel may have disappointed investors, said Wyn Ellis, analyst at Numis Securities. “But the general commitment to an efficient balance sheet and cash returns remains,” he added.

IHG, which owns the Holiday Inn, Crowne Plaza and InterContinental brands, returned more than $1bn to shareholders last year, including a $763m special dividend in May following an informal takeover approach and sale of two hotels. The 11 per cent boost in final dividend to 52 cents brings the total dividend to 77 cents, up 10 per cent.

The chain, which runs on an “asset light” model under which it manages hotels but does not own the property, accepted a €330m offer for the InterContinental Paris Le Grand hotel in the period. Mr Solomons said a decision on what to do with the proceeds would be taken when the sale is completed in the first half of 2015.

Mr Solomons said he was concerned about the “constant sniping at business” in the UK, where acting Walgreens Boots Alliance boss Stefano Pessina sparked controversy last month after saying a Labour government would be a “catastrophe”.

When asked if he thought Ed Miliband, Labour party leader, was supportive of business, Mr Solomons said: “I haven’t heard a lot that sounds supportive of wealth creation and I think that’s unfortunate”.

Reported operating profit fell 3 per cent to $651m, in line with market expectations, following disposals of hotels in 2013. However, underlying operating profits rose 8.1 per cent to $639m, including a $9m hit from currency fluctuations, and the company reported its strongest net room growth since 2009, up 3.4 per cent to 710,000

The company made its first corporate acquisition in a decade last year when it bought the Kimpton US boutique hotel group for $430m in cash. The deal gave IHG 62 upmarket resorts and 71 restaurants, bars and lounges in the US, boosting its presence in the fast-growing sector of the hospitality industry.

Operating profits in the Americas rose 8 per cent on an underlying basis and IHG added 38,000 rooms, a 12 per cent jump and its best performance for six years.

In China, where the company has operated for 30 years and this month launched the first of its Hualuxe hotel brand, revenue per available room fell 3.4 per cent as it shifted focus from large coastal cities to growth in medium-sized centres.

Operating profits rose 9 per cent “in a challenging environment with slower macroeconomic conditions, government austerity measures and protests in Hong Kong”.

The UK and Germany performed well, the company said, but economic troubles in Russia led to a fall in income of $3m.

Instability in Thailand in the first half led to a double-digit decline in revenue per available room, IHG added.

Gapping down

In reaction to disappointing earnings/guidance: RGSE -17.9%, HLX -11.4%, WLT -10.1%, IHG -5.6%, VNR -5.1%, AGIO -3.8%, WWW -3.5%, GLF -2.6%, USTR -1.5%, CADC -1.5%, CRY -0.9%, EPE -0.8%, MGM -0.8%, SYKE -0.7%, PES -0.7%

Select silver/mining stocks trading lower: SSRI -3.3%, SLV -3.0%, PAAS -2.4%, SLW -2%

Other news: CLTX -82.3% (announces Phase II trial of MRX-6 cream 2% in pediatric Atopic Dermatitis did not reach primary endpoint), VBLT -44.7% (announces removal of FDA partial clinical hold on VB-111), WHX -21.7% (NYSE suspends trading, company expects trading to move to OTC effective with the opening of trading on February 17, 2015), JOEZ -12.4% (disclosed it received an additional notice of defaults and events of default), NBG -10.6% (no resolution in Greece/EU talks), MNST -2.5% (disclosed that in relation to its previously announced agreement with Coca-Cola (KO), it expects to incur costs associated with the transition of its distribution arrangements in an amount currently estimated to be $280 mln), QTWO -2.3% (files for offering of ~4.56 mln shares of common stock: co selling 1.5 mln shares, selling stockholders selling ~3.06 mln shares), ASML -2% (still checking), ARMH -1.8% (still checking), GSK -1.6% (still checking), AZN -1.5% (US District Court rules PULMICORT RESPULES patent is invalid), GGP -0.9% (disclosed that it has extended its employment agreement with CEO Sandeep Mathrani for an initial five year term)

Analyst comments: BID -4.3% (downgraded to Market Perform from Outperform at Cowen), CVC -1.7% (downgraded to Sell from Neutral at UBS), M -1.4% (initiated with an Underweight at Barclays), LYB -1.2% (downgraded to Neutral from Buy at Citigroup), JWN -1.1% (downgraded to Underweight at Barclays), ZAYO -1.1% (downgraded to Underperform from Neutral at Macquarie)

In reaction to disappointing earnings/guidance: RGSE -17.9%, HLX -11.4%, WLT -10.1%, IHG -5.6%, VNR -5.1%, AGIO -3.8%, WWW -3.5%, GLF -2.6%, USTR -1.5%, CADC -1.5%, CRY -0.9%, EPE -0.8%, MGM -0.8%, SYKE -0.7%, PES -0.7%

Select silver/mining stocks trading lower: SSRI -3.3%, SLV -3.0%, PAAS -2.4%, SLW -2%

Other news: CLTX -82.3% (announces Phase II trial of MRX-6 cream 2% in pediatric Atopic Dermatitis did not reach primary endpoint), VBLT -44.7% (announces removal of FDA partial clinical hold on VB-111), WHX -21.7% (NYSE suspends trading, company expects trading to move to OTC effective with the opening of trading on February 17, 2015), JOEZ -12.4% (disclosed it received an additional notice of defaults and events of default), NBG -10.6% (no resolution in Greece/EU talks), MNST -2.5% (disclosed that in relation to its previously announced agreement with Coca-Cola (KO), it expects to incur costs associated with the transition of its distribution arrangements in an amount currently estimated to be $280 mln), QTWO -2.3% (files for offering of ~4.56 mln shares of common stock: co selling 1.5 mln shares, selling stockholders selling ~3.06 mln shares), ASML -2% (still checking), ARMH -1.8% (still checking), GSK -1.6% (still checking), AZN -1.5% (US District Court rules PULMICORT RESPULES patent is invalid), GGP -0.9% (disclosed that it has extended its employment agreement with CEO Sandeep Mathrani for an initial five year term)

Analyst comments: BID -4.3% (downgraded to Market Perform from Outperform at Cowen), CVC -1.7% (downgraded to Sell from Neutral at UBS), M -1.4% (initiated with an Underweight at Barclays), LYB -1.2% (downgraded to Neutral from Buy at Citigroup), JWN -1.1% (downgraded to Underweight at Barclays), ZAYO -1.1% (downgraded to Underperform from Neutral at Macquarie)

Gapping up

In reaction to earnings/guidance: VIPS +10.1%, ROX +6.7%, VDSI +6.1%, Z +4.2%, GT +4.2%, TTS +3.4%, QSR +2.7%, WM +2.7%, MDT +2.3%, ITRN +2.1%, GIS +1.1%, FDP +1.1%, HK +1%, USAT +0.5%

M&A news: CCG +5.6% (announces exploration of strategic alternatives), LMNS +1.5% (reports of Fosun (FOSUF) interest)

Select oil/gas related names showing early strength: GDP +3.9%, SDRL +3.9%, NBL +2.4%, PBR +1.9%, OAS +1.5%, WLL +1.3%, PWE +0.8%, BHI +0.8%

Other news: IBIO +40% (following 60 Minutes special this weekend on partner Mapp Pharma's ZMapp product as a treatment for Ebola), ONCY +29.4% (confims that the FDA has granted Orphan Drug Designation for its lead product candidate, REOLYSIN, for the treatment of pancreatic cancer), GEVO +20.1% (cont strength), GENE +16.9% (cont pre-mkt vol), RXDX +7.1% (confirms it Received Orphan Drug Designation from FDA for Entrectinib for the Treatment of Molecularly Defined Subsets of Colorectal Cancer), CEL +6.5% (announces collective employment agreement), NAVB +5.6% (peer-reviewed publication of results from a Phase 3 clinical trial; results demonstrated that Lymphoseek met the primary efficacy endpoint), PSTI +5.2% (still checking), CYRN+4.6% (announced that ALSO Deutschland GmbH now distributes the cloud-based CYREN WebSecurity solution), CANF +3.6% (receives notice of allowance in U.S. for Psoriasis patent), MHR +3.4% (announces 2015 upstream capital expenditure budget; flexible 2015 upstream budget of $100 mln), RTK +3.2% (announces that GSO Capital Partners has increased its credit facility for Rentech by up to $63 million), CYTX +3% (announces the first patient has been treated in its FDA approved trial assessing the effect of Cytori Cell Therapy for osteoarthritis of the knee), NVAX +2.5% (favorable commentary on Friday's Mad Money), HOT +2.5% (announced that Frits van Paasschen has resigned as CEO), ACT +1.6% (launches generic Pulmicort RESPULES), NICE+1.4% (announces Sarit Sagiv as its new CFO), NEE +1.4% (announces CFO transition plan)

Analyst comments: SRPT +7.8% (upgraded to Buy from Neutral at BofA/Merrill), EURN +5.1% (initiated with a Buy at Citigroup), FEYE +1.5% (target raised to $49 from $44 at BofA/Merrill), GPRO +1.2% (initiated with a Outperform at Northland Capital), MU +1.1% (upgraded to Outperform from Neutral at Macquarie), BBVA +1% (upgraded to Outperform from Underperform at Exane BNP Paribas)

In reaction to earnings/guidance: VIPS +10.1%, ROX +6.7%, VDSI +6.1%, Z +4.2%, GT +4.2%, TTS +3.4%, QSR +2.7%, WM +2.7%, MDT +2.3%, ITRN +2.1%, GIS +1.1%, FDP +1.1%, HK +1%, USAT +0.5%

M&A news: CCG +5.6% (announces exploration of strategic alternatives), LMNS +1.5% (reports of Fosun (FOSUF) interest)

Select oil/gas related names showing early strength: GDP +3.9%, SDRL +3.9%, NBL +2.4%, PBR +1.9%, OAS +1.5%, WLL +1.3%, PWE +0.8%, BHI +0.8%

Other news: IBIO +40% (following 60 Minutes special this weekend on partner Mapp Pharma's ZMapp product as a treatment for Ebola), ONCY +29.4% (confims that the FDA has granted Orphan Drug Designation for its lead product candidate, REOLYSIN, for the treatment of pancreatic cancer), GEVO +20.1% (cont strength), GENE +16.9% (cont pre-mkt vol), RXDX +7.1% (confirms it Received Orphan Drug Designation from FDA for Entrectinib for the Treatment of Molecularly Defined Subsets of Colorectal Cancer), CEL +6.5% (announces collective employment agreement), NAVB +5.6% (peer-reviewed publication of results from a Phase 3 clinical trial; results demonstrated that Lymphoseek met the primary efficacy endpoint), PSTI +5.2% (still checking), CYRN+4.6% (announced that ALSO Deutschland GmbH now distributes the cloud-based CYREN WebSecurity solution), CANF +3.6% (receives notice of allowance in U.S. for Psoriasis patent), MHR +3.4% (announces 2015 upstream capital expenditure budget; flexible 2015 upstream budget of $100 mln), RTK +3.2% (announces that GSO Capital Partners has increased its credit facility for Rentech by up to $63 million), CYTX +3% (announces the first patient has been treated in its FDA approved trial assessing the effect of Cytori Cell Therapy for osteoarthritis of the knee), NVAX +2.5% (favorable commentary on Friday's Mad Money), HOT +2.5% (announced that Frits van Paasschen has resigned as CEO), ACT +1.6% (launches generic Pulmicort RESPULES), NICE+1.4% (announces Sarit Sagiv as its new CFO), NEE +1.4% (announces CFO transition plan)

Analyst comments: SRPT +7.8% (upgraded to Buy from Neutral at BofA/Merrill), EURN +5.1% (initiated with a Buy at Citigroup), FEYE +1.5% (target raised to $49 from $44 at BofA/Merrill), GPRO +1.2% (initiated with a Outperform at Northland Capital), MU +1.1% (upgraded to Outperform from Neutral at Macquarie), BBVA +1% (upgraded to Outperform from Underperform at Exane BNP Paribas)