* Summary: Leonteq offers a solution to manufacture structured investment products (SIPs). It offers unique technology, process and distribution capabilities to clients (banks and life insurance companies) to issue, manage and distribute SIPs. Leonteq's B2B platform benefits from quality and cost leadership that is reinforced with further investments in scale and technology. We transfer coverage to Virginia Nordback and re-initiate with a Buy recommendation and a price target of CHF247.00, offering 43% upside potential.* Growing platform partners: Leonteq's focus is to increase the volume of issued products by growing its platform partner business. It currently works with five partners and announced a further five with its H1 2015 results, which we estimate will go live in H2 2015/2016. Its goal is to reach 30 partners by 2020, with an increased focus outside its domestic market.* A business model in transformation: Leonteq is transforming itself from a financial institution (Fin) via a business services company (Finteq) towards becoming a technology player (Teq). The recently introduced Teq business line addresses the needs of large investment banks and allows Leonteq to break into an additional market. These larger partners will carry the market risk of the SIP on their balance sheets. As a result, this business line will have very low capital requirements. We estimate 84% of revenue in 2017 will come from Finteq and Teq.* Scale over profitability: In our view, the market is focusing too much on short-term profitability pressures, which is the result of growing a lower-margin product that requires investment in staff. We think that investors should look beyond the next two years, when these investments will start to pay off. Scale and the resulting lower unit costs, as well as further sell- and buy-side automation, will reinforce Leonteq's cost leadership and, therefore, secure Leonteq's position as market leader, protecting its margins in the long run.* Future growth: Leonteq aims to bring four partners on board per annum - two insurance and two banking partners. Insurance is an attractive market with generally higher-margin products due to a lack of alternative offerings. Unit-linked policies are long-term investments and thus generate very sticky customers, strengthening the quality of revenue.* Valuation: We use a DCF approach to capture the long-term growth potential. Our cost of equity is 8.7% and our long-term growth rate is 0.5%. With no direct competitors, we look at business services companies and tech companies with a software-as-a-service (SaaS) revenue model. On a 2017 earnings comparison, Leonteq currently seems undervalued.* Catalyst: We expect an update on the integration progress in H2 2015. Full-year results are released on 4 February 2016.

>>> Asset Class Flows

* Equities: $4.0bn inflows (5 straight weeks) (all via ETFs, e.g. EFA, IWM & IWB)

* Bonds: $6.4bn outflows (first outflows in 5 weeks)

* Precious metals: 3 straight weeks of outflows ($0.6bn)

* Money-markets: $9.1bn inflows ($105bn inflows over past 6 weeks)

>>> Equity Flows

* Europe booming: $1.7bn inflows (inflows in 24 of past 26 weeks)

* Japan: small $0.1bn outflows (first outflows in 4 weeks)

* Chart 4: Weekly flows to Govt bond funds ($bn)

* Source: BofAML Global Investment Strategy, EPFR Global

* EM: $2.2bn outflows (largest in 9 weeks)

* US: small $0.3bn outflows (note: $2.6bn ETF inflows vs $2.9bn mutual fund outflows)

By sector: financials see 4 straight weeks of inflows ($0.2bn); tech sees 5 straight weeks of inflows ($0.5bn); outflows from utilities ($0.5bn)

>>> Fixed Income Flows

* Big $4.0bn outflows from Govt/tsy funds (largest since Jun’14)

* $2.0bn outflows from EM debt funds (largest in 10 weeks) (outflows in 15 of 16 weeks)

* Modest $0.5bn outflows from HY bond funds (first outflows in 5 weeks)

* IG bond funds eke out small $0.4bn inflows (5 straight weeks)

* Too early to assess value in VW’s shares: There remains little clarity on two key

questions: 1) what will be the total cash cost of fines, settlement, and recalls? 2) What

reputational damage will the revelations have on customers’ buying behaviour? In this

note we assume that the direct cash cost to VW is €25bn and reduce our forecast for

VW unit sales for the remainder of 2015 and FY16. Incorporating these assumptions,

we stay Equal Weight and reduce our price target for VW Preferred shares to €106 and

to €127 for the Ordinary shares.

* We estimate €25bn of fines spread over 2015-17: We analyse precedents to estimate

€10bn of recall costs and NOx compensation, €8bn of US fines, €2bn for fines outside

the US, €1bn for a US class action lawsuit, €2bn of “economic risk” for CO2 deficiencies,

and €2bn of potential CO2 fines.

* Future sales will be impacted by fears of declines in the residual values for VW, in

our view: Resale values of models affected by the scandal have fallen significantly and

models are taking longer to sell. The full repercussions of this are unlikely to be seen

until the November sales data. We now expect 2015 sales volumes to be down by 2.5%

(compared with management guidance for flat sales) and FY revenue to increase by

3.2% (compared to the 4% management target).

* We are lowering our price targets for the preferred and ordinary shares from €240

to €106 and €127, respectively, but maintain our Equal Weight rating: We have

updated our SoTP for our revised estimates and have factored in a €25bn cost for the

existing NOx and fuel consumption scandals. We are applying discounts of up to 70%

to the multiples of VW’s brands in our SoTP given the obvious concerns over further

problems, and we have added a 20% premium to the ordinary shares because of the

value of their voting rights. While the shares have fallen far and we see more value in

the business than investors are currently willing to ascribe, we equally think that until

there is some sign that the investigations by VW and by the regulators are complete,

the shares will not outperform.

The greatest beer transaction ever

● Greatest beer transaction ever: Anheuser-Busch InBev (ABInBev) finally presented

its formal offer for the share capital of SABMiller. With a transaction value of

GBP71bn, this represents the largest beer deal ever. The combined company will

dominate the beer markets in Africa and both North and Latin America, materially

raising the growth profile of ABInBev.

● 80% of EBITDA in countries with 50%-plus market share: We cannot think of any

other company that can boast a statistic like this. Not only will the NewCo be

selling one-third of all the beer consumed on the planet, it will do so with an

enviable market position in most of the individual markets that matter. In

addition, the group will benefit from the stability that increased geographical

diversification can bring – the largest market is the US with 22% of sales – and will

have, on top of that, one of the strongest growth profiles among the large global

brewers given its high exposure (66% of FY 2017E EBITDA) to emerging markets.

● Earnings can double by 2020: Integration of SABMiller can increase EPS from

USD5.33 FY 2015E to USD9.73 by FY 2020E. Our calculations suggest ROIC can hit

a WACC of 7% by year four when synergies are fully delivered.

● Synergies of USD2.0bn are conservative: There is no structural reason why

SABMiller’s Latin America and Africa EBITDA margins should not converge with

those of ABInBev in North America or Brazil. Applying the former’s margins to

SABMiller subsidiaries yields USD1.3bn of synergies. Applying the latter’s yields

USD2.9bn. USD2.0bn of synergies realised over four years (USD1.4bn announced

plus SABMiller’s cost savings) is conservative.

● All regulatory hurdles are addressable: We believe ABInBev faces regulatory

issues in 13 countries. In most of these markets, either SABMiller or ABInBev has a

dominant position while the other imports brands. In the UK, Russia and Italy

combined share will approach 30% and regulators here may request concessions.

However, the potential impact on cost synergies is limited. ABInBev has

announced the conditional disposal of SABMiller’s North America business for

USD12bn and we believe Chinese brewer CR Snow will follow (USD3.1bn).

● ABInBev becomes our top pick in beverages: Execution risks remain, but

ABInBev’s management has the best M&A track record in the industry. With the

resulting company holding more than a 50% market share in countries that

cumulatively account for 80% of FY 2017E EBITDA, it is feasible for the shares to

trade on multiples in line with major consumer goods peers such as Nestlé (22.6x

FY 2015E P/E). Applying a target P/E multiple of 20x to FY 2020E earnings and

discounting back gives us a 12-month price target of EUR143 (26% upside). We

therefore upgrade to Buy and add ABInBev to our stable of ALPHA stocks.

● Limited upside for SABMiller as a standalone: With both companies agreeing

terms and the cash offer for shareholders set at GBP44, we see limited upside to

the standalone company. We do not envisage regulatory issues beyond Miller

Coors and CR Snow acting as a stumbling block to the deal. We raise our price

target to the cash offer price of GBP44 and downgrade SABMiller to Hold.

● SABMiller’s recent results: The group recorded 20bp of EBITA margin expansion

driven by cost savings and efficiency gains in Africa and Asia-Pacific, although

some of this benefit was offset by adverse currency movements in Latin America

and competitive pressures in Poland. Reported group NPR, EBITA and adjusted

EPS declined by 12%, 11% and 11% respectively and the continued depreciation of

emerging-market currencies remains a significant headwind.

Wirecard, the German listed payments company, is to pay as much as €330m for a business which was barely involved in payments two years ago, according to Indian corporate filings.

Accounts for the largest subsidiary of the group to be acquired show qualified audit opinions due to concerns about revenue recognition and an inability to verify key financial totals, and recent resignations of directors and auditors.

Sales and profits claimed by Wirecard for the businesses it intends to buy also imply a dramatic transformation in financial performance during the last 18 months.

The question for shareholders, from whom Wirecard has raised €0.5bn in recent years to fund such dealmaking, is what exactly has it agreed to buy?

We’ve previously raised questions about the way Wirecard buys companies, undisclosed portions of previous deals, apparent mismatches between sets of accounts in different countries, the way the cash flow profile of the business is not what might be expected, and a large receivables balance obscured by adjustments the company asks analysts to make.

The company’s cash flow is under scrutiny, and analysts have been waiting to see how the group uses €360m raised from the sale of stock more than 18 months ago.

Wirecard’s purchase also comes at a time when investors are paying close attention to technology companies operating in distant jurisdictions after a series of controversies. For instance Globo, a UK listed group technology group placed into administration this month after the chief executive resigned and admitted “certain matters regarding the falsification of data and the misrepresentation of the company’s financial situation”. The collapse of the company followed a critical report published by a New York hedge fund which found claimed sales partners did not exist, including a Mumbai group which turned out to be a laptop repair specialist which hadn’t heard of Globo.

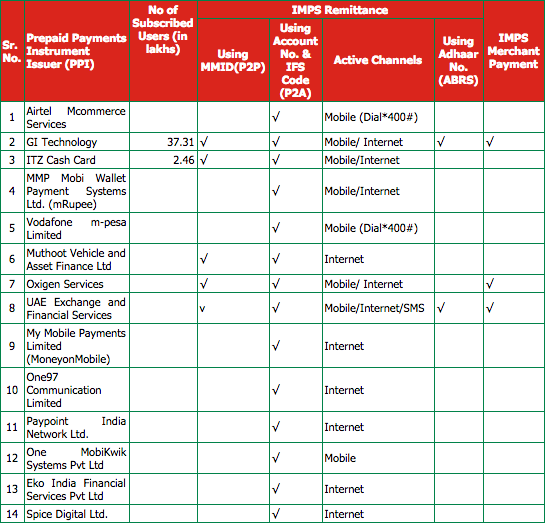

What Wirecard announced it would buy on October 27 is the fast growing payments business of Great India Retail, which includes the Smart Shop and iCashcard brands, and 60 per cent of GI Technology, a subsidiary operating prepaid payment cards. The company says these operations will have revenues of €45m in 2015, and €75m the year after. Earnings, on a pre-tax, interest, depreciation and amortisation basis will be €7m this year and then as much as €18m in 2016, Wirecard says. It will pay €230m initially, and up to another €100m dependent on future profits.

Wirecard told us “the main legal entities where the payment business of GI Retail Group were concentrated and which were acquired as part of the transaction are Hermes and GI Technology (of which Hermes is the main operative company/revenue generator and GI Technology is mainly the licence provider).”

The two main efforts are iCashcard and Smart Shop, what a spokesperson called “retail assisted ecommerce” — essentially kiosks where Indians can have someone interact with the internet on their behalf. Wirecard also says remittances are a big part of the business. To generate that €45m of sales expected this year, Wirecard said the ecommerce and remittances will transact about €2.8bn of payment volumes.

Wirecard also said “The National Payments Corporation of India (NPCI) ranks GI Technology as number one bank’s remitter among 123 members, as of 6th of October 2015.”

To do so, it must be growing very fast indeed. We could only find two references to GI Technology on the NPCI website. One is the number-light table to the right.

To do so, it must be growing very fast indeed. We could only find two references to GI Technology on the NPCI website. One is the number-light table to the right.The other is in a list of milestones of the Immediate Payment Services (IMPS) network run by the NPCI:

GI Technology Pvt. Ltd as a RBI authorized Prepaid Payments Instrument Issuer (PPI) joins IMPS – 4-Jun-13

Swift work to reach number one in under two and a half years. NCPI did not respond to a request for comment.

According to the most recent balance sheet available for GI Technology, at the end of March 2014 trade payables were 87m rupees, or about €1m, and trade receivables were about €0.24m. The group also lists 62m rupees of “security deposits”, up from 49m the year before.

GI Technology was granted a prepaid card license in 2009, but it was only in October last year that it amended its memorandum of association to make reference to remittances and foreign exchange.

What about the parent company, GI Retail? At the end of March 2014 its balance sheet lists reserves of 96m rupees (€1.2m), borrowings of €2m, de minimis cash, and investments of €3m, with the totals for each lower than reported the previous year, which suggests at that time it was neither a large or growing entity. There were zero trade receivables or trade payables. A further subsidiary, GI Hospitalities, filed a sparse balance sheet with no number larger than the 48m rupee (€0.6m) total for trade payables.

Which leaves Hermes, the main operating company which until recently described itself as a travel agent.

At first glance it looks substantial. The annual filing for the year to March 2014 details turnover of 15bn rupees (€185m). However it also describes the business as “travel arrangement tour operator and related services”, and discloses 13 product or services categories within that, with the “turnover of highest contributing product or service” for each. The largest is airline ticket booking, at 11bn rupees, followed by 2.8bn rupees for railway ticket bookings.

Yet those revenues are not what most companies would call revenues. The auditor qualified its opinion on the Hermes accounts, with revenue recognition cited as one of the reasons:

The Company’s major revenue is the commission it earns from online booking of air/rail /movie/ bus tickets and other support services which is in the nature of agency commission. As per Accounting Standard 9, gross commission earned should be taken as gross revenue and not the gross inflow of cash or sales value. However, the Company has followed the policy of recognizing gross inflow of cash from sale of tickets as sales value instead of taking gross commission earned as its revenue. This has resulted in the gross revenue overstated by Rs 1,520.17 crores (previous year Rs.1,118.70 crores) and gross purchase cost overstated by Rs.1,492.02 crores (previous year Rs.1,101.86 crores). This is the result of a decision taken by the management and caused us to qualify our audit opinion on financial statements since 2012-13. The effect on the financial statements on account of the same could not be quantified by us.

A crore is 10m rupees. Deduct 15,201.7m rupees from the reported (and audited) total of 15,334.2m rupees, and you are left with 132m rupees, worth €1.6m.

Wirecard said this is not correct. “After changing the revenue recognition from a gross basis (transaction volume processed) to a net basis (commission earned) the total revenue amounts to EUR 15.8m). However, there is no impact on gross margin and EBITDA in FY13/14 due to the change of revenue recognition.”

It gave us the following table of figures for what it is buying based on “audited and consolidated financial statements”:

The annual report to March 2014 also details recent efforts to get into payments, describing a change in policy at the Reserve Bank of India to allowing banks to use intermediaries to supply financial services. “To take advantage of the policy of the RBI, your Company took the initiative and signed up agreement with Yes Bank to act as their BCA last year and capitalised on it this year”.

Hermes’s current website describes itself as the exclusive distribution and recharge network for iCashcard. The March 2014 report describes Hermes signing up with iCashcard during the year, with revenues from iCashcard money transfer commissions totalling 9m rupees, worth €114,000.

The auditors also said the reasons for qualifying the opinion include a lack of verification of key financial metrics: “The Company has not obtained confirmation of balances in respect of Trade debtors, Trade payables, deposits, loans and advances outstanding as on March 31, 2014.”

Following that the memorandum of association was changed in November to include a paragraph detailing payment related services and remittances, then two of the directors of Hermes resigned in December 2014, both citing “personal reasons”. Wirecard said these were close relatives of the founder who were replaced for operational reasons as the company grew.

On 24 August this year longstanding Hermes audit firm Kuriachan & Nova, resigned “due to our pre-occupation on other assignments”. Another firm, V Krishnan & Co, was appointed auditor on the 28th. On the 31st it resigned, saying it was “not in a position to conduct the audit Individually thus resigning for being appointed as Joint Statutory Auditor.” On September 9th both firms were reappointed as joint auditors. Wirecard said the need for joint auditors was a reflection of the company’s growth.

In terms of the underlying businesses Matt Earl has already written a couple of postsat Lordship Trading looking at Great India Retail and Hermes.

The current Hermes Network website was created in May, according to whois data, and prior to that it had a different web address. One of the odd things Matt found from looking at the old site in the internet archive was earlier this year there was little mention of payments on the Hermes website, which described itself as a travel agent.

Hermes made its humble beginning in 2006 and went on to play an important role in the Indian travel industry through its innovative technology approach and its ability to build a nation wide network of traditional travel agents as well as a new set of non traditional agents who have taken travel closer to the common man in India.

Our attention was drawn to a box of “recent events”. In January this year the top event was news that Hermes had signed up with Yes Bank to provide money transfer services. Yet click on the read more… link and the internet archive takes us to a “recent news” page with what looks like headlines for 8 press releases (without links to the full release), all dated May 1, 2011.

The first of those has an unusual headline:

On the old website, in early 2014, Hermes listed three distribution channels, again travel focused:

Matt also compared GI Retail to an Indian competitor, Suvidhaa, which claims 80,000 retail outlets, to GI Retail’s 90,000.

In the year to March 2014, Suvidhaa reported 31bn rupees (€375m) of gross transaction value, income from operations of 377m rupees (€4.6m), but lost 89m rupees (€1m) at the bottom line.

Wirecard said “obviously the payment business of GI Retail was showing a stronger business performance than this competitor”.

Matt also finds a TV interview with the ceo of Suvidhaa, which compares with what some might regard as the surprising lack of Indian business coverage of the Wirecard deal. The Economic Times gave it a 60 word brief, while the Business Standard tookthe Reuters rewrite of the press release. Perhaps it’s because travel agent and ticket kiosks are pretty common in a big country with lots of people who lack internet access.

What then should we conclude?

The reason it’s important for auditors to verify key financial balances, such as trade receivables and trade payables, is as a check on the overall quality of the accounts. Were a company to overstate revenues and profits, it would then have to find a way to spend the fake cash created, either by inflating costs or the value of assets it buys.

Auditors can be fooled, Globo got a clean bill of health from Grant Thornton, for instance, but there were red flags prior to that: BDO resigned as auditor in February 2014, for instance, citing an inability to agree “audit scope in relation to our involvement in the work of component auditors”.

India is a fast growing economy, with e-commerce, payments and remittances all experiencing rapid growth. Wirecard investors will no doubt be reassured by what the company says was “intensive internal and external legal, financial and tax due diligence”. They may, perhaps, want to get a clearer picture of what the company is buying.

Dow-1.44% S&P-1.40% Nasdaq-1.22% Russell-1.98% VIX 18.37 ( 14.39%)

US MArket Closed Lower, S&P closed below its 200d MA. Weakness in europe didn't help US Sentiment. Energy sector (-2.4%) struggled from the start and the significant underperformance in the growth-sensitive group set the tone for a down day. The sector widened this week's decline to 5.4% while crude oil fell 2.7% to $41.78/bbl. materials sector (-2.0%) finished at the bottom of the leaderboard while other groups posted slimmer losses. Tech outperform and avoid a bigger decline. utilities sector (-1.2%) held a slim gain at the start, but could not hold its ground into the afternoon. consumer staples (-1.4%) and health care (-1.8%) registered wider losses.. IBB -2.1%, down -3.1% for the week. Volume were in line with average @850mil shares. US After Hours USAT +15.9%, LPCN +15.5%, PLNT +13.1%, WLDN -23%, JWN -20.4%, PRTY -15.4%, FOSL -14.7% following earnings/guidance Market sentiment in Asia has turned decidedly bearish going into the weekend, tracking steeper losses on Wall St widely attributed to the decline in energy and strong JOLTS report boosting expectations of Fed liftoff. China vice head of economic monitoring and analysis center Pan remarked it would help for PBoC to further cut RRR and interest rates. Japan cabinet officials Amari and Aso both indicated the govt is not planning an extra budget even if Q3 GDP contracts, sending Japan back into technical recession. Japan Q3 GDP data will be updated this coming Sunday evening. Fed Vice Chair Fischer capped off an active session of Fed-speak with fairly upbeat comments, noting the downward pressure on US inflation is related to USD and energy and will fade in 2016. Focusing on USD, Fischer said US economy is weathering the impact of strong exchange rate as well as foreign weakness well, concluding that rate liftoff next week may be appropriate.

Nikkei -0.51% HangSemg -2.25% Shanghai -1.51%

Eur$ 1.0785 JPY 122.68 CNY 6.3738 GBP 1.5216 CHF 1.0018 RUB$66.6070 WTI $41.63 (-0.29%)

S&P +0.15% EuroStoxx -0.56% Dax -0.48% SMI -0.59%

Macro :

- World Bank to Participate in Greek Banks’ Recap: Capital.Gr

Keep an eye on :

- ABG/P SM : Abengoa to Announce Record Losses, El Confidencial Reports

- AGFB BB : Agfa-Gevaert 3Q Net EU30m vs EU6m Y/y; Reiterates FY Margin Goal

- B5A GY : Bauer Says Order Backlog Rises to Record, Reaffirms Forecast

- BKEB BB : Bekaert 3Q Rev. of EU898m Misses Est.; Net Debt Drops to EU906m

- EN FP : Bouygues 3Q Sales Decline, Profit Increases; Keeps Outlook

- ENEL IM : Enel 3Q Ebitda, Revenue Beat; Confirms 2015 Targets, Div. Policy

- GFK GY : GFK 3Q Rises 4%, EPS Up 43%; Confirms 2015 Forecast

- HDD GY : Heidelberger Druck 2Q Adj. Ebitda Drops; Confirms FY Targets

- MAERSKB DC : Maersk Chairman Says Low Debt Gives Room for M&A: Berlingske

- SYNN VX : +12.8% After Hours on Chemchina news : ChemChina Is Said to Be in Talks to Acquire Syngenta

- SYNN VX : Business Insider: Syngenta reportedly rejects yet another multibillion-dollar takeover offer

- GLE FP : SocGen to Close 74 French Branches From 2016, Echos Says

- SPA BB : De Bois Family EU95 Offer to Take Spadel Private Starts Today

- TCH FP : Technicolor Completes EU227M Rights Offer; Demand About EU600M

>>> Up

*AB INBEV RAISED TO BUY VS HOLD AT BERENBERG

*BAE SYSTEMS RAISED TO NEUTRAL VS UNDERWEIGHT AT JPMORGAN

*HHLA RAISED TO NEUTRAL VS REDUCE AT NOMURA

*ICAP RAISED TO HOLD VS SELL AT LIBERUM

*LEONTEQ REINITIATED AT BUY AT BERENBERG; PT CHF247

*ONTEX RAISED TO NEUTRAL VS UNDERWEIGHT AT JPMORGAN

*TELENOR RAISED TO BUY VS HOLD AT NORDEA

>>> Down

*BREMBO CUT TO NEUTRAL VS OUTPERFORM AT MEDIOBANCA

*DEUTSCHE BANK CUT TO NEUTRAL VS BUY AT CITI

*EUROFINS SCIENTIFIC CUT TO REDUCE VS HOLD AT HSBC

*FERRAGAMO CUT TO NEUTRAL VS OUTPERFORM AT MEDIOBANCA

*IMI CUT TO ’HOLD’ AT SOCIETE GENERALE

*IMI CUT TO UNDERPERFORM AT RBC CAPITAL

*SABMILLER CUT TO HOLD VS BUY AT BERENBERG

*SPIRE HEALTHCARE CUT TO NEUTRAL VS OVERWEIGHT AT JPMORGAN

*VERBUND CUT TO SELL VS HOLD AT BERENBERG

*WILLIAM DEMANT CUT TO HOLD VS BUY AT NORDEA

>>> PT Change

>>> initiation

*ALPHA BANK RATED NEW BUY AT HSBC; PT EU0.137

*COVESTRO RATED NEW OUTPERFORM AT CREDIT SUISSE; PT EU34

*PIRAEUS RATED NEW HOLD AT HSBC; PT EU0.061

>>> Call

Asian Mid-session Update: Soft lending figures weigh on China markets

***Economic Data***

- (JP) JAPAN SEPT FINAL INDUSTRIAL PRODUCTION M/M: 1.1% V 1.0% PRELIM; Y/Y: -0.8% V -0.9% PRELIM

- (JP) Japan Sept Conference Board Leading Economic Index -0.8% v 0.1% prior

- (KR) South Korea Sept Conference Board Leading Economic Index (LEI) +0.6% v +0.3% prior

- (SG) SINGAPORE SEPT RETAIL SALES M/M: -3.7% V +5.5% PRIOR; Y/Y: 4.6% V 5.5%E; RETAIL SALES EX AUTO Y/Y: -1.4% V +0.7%E

- (PE) PERU CENTRAL BANK LEAVES REFERENCE RATE UNCHANGED AT 3.50%, AS EXPECTED

- (CL) CHILE CENTRAL BANK (BCCH) LEAVES OVERNIGHT RATE TARGET UNCHANGED AT 3.25%, AS EXPECTED

- NPD: Oct US total video game sales $806M, +2% y/y

***Index Snapshot (as of 02:30 GMT)***

- Nikkei225 -0.8%, S&P/ASX -1.5%, Kospi -1.1%, Shanghai Composite -1.2%, Hang Seng -2.1%, Dec S&P500 +0.1% at 2,042

***Commodities/Fixed Income***

- Dec gold +0.1% at $1,082/oz, Dec crude oil -0.6% at $41.52/brl, Dec copper -0.5% at $2.16/lb

- GLD: SPDR Gold Trust ETF daily holdings fall 1.5 tonnes to 661.9 tonnes; Lowest since 2008

- SLV: iShares Silver Trust ETF daily holdings rise to 9,801 tonnes from 9,756 tonnes

- (CN) China Iron and Steel Association (CISA): China Jan-Oct apparent steel consumption -5.7% y/y

- USD/CNY: (CN) PBoC sets yuan mid point at 6.3655 v 6.3628 prior setting; 9th straight weaker setting; weakest Yuan setting since Sept 29th

- (JP) BOJ offers to buy ¥400B in 5-10yr JGBs, ¥240B in 10-25yr JGBs and ¥140B in JGBs with maturity over 25-yr

- (AU) Australia MoF (AOFM) sells A$800M in % 2019 Bonds; avg yield: 2.2231; bid-to-cover: 2.98x

- (US) Weekly Fed Balance Sheet Total Assets for week ending Nov 11th: $4.49T v $4.49T prior; Reserve Bank Credit: $4.45T v $4.45T prior; M1 y/y change: 6.9% v 7.2% prior; M2 y/y change: 6.0% v 5.9% prior

***Market Focal Points/FX***

- Market sentiment in Asia has turned decidedly bearish going into the weekend, tracking steeper losses on Wall St widely attributed to the decline in energy and strong JOLTS report boosting expectations of Fed liftoff. China markets are particularly soft in the wake of October lending figures out overnight falling to a 15-month low of CNY514B. YTD steel consumption out of CISA reflects the slowing in the property sector as well. China vice head of economic monitoring and analysis center Pan remarked it would help for PBoC to further cut RRR and interest rates.

- Japan cabinet officials Amari and Aso both indicated the govt is not planning an extra budget even if Q3 GDP contracts, sending Japan back into technical recession. Japan Q3 GDP data will be updated this coming Sunday evening (US time). Also out of Japan, Conf Board Leading Index fell -0.8% v 0.1% prior, and resident economists noted downside risks still remain. Toshiba was under heavy pressure again after Nikkei reported Westinghouse unit has disclosed writedowns of $1.3B in FY12 and FY13, raising further concerns about the company's transparency in disclosing large losses.

- Fed Vice Chair Fischer capped off an active session of Fed-speak with fairly upbeat comments, noting the downward pressure on US inflation is related to USD and energy and will fade in 2016. Focusing on USD, Fischer said US economy is weathering the impact of strong exchange rate as well as foreign weakness well, concluding that rate liftoff next week may be appropriate. Despite these somewhat hawkish view, USD majors were not particularly volatile - USD/JPY traded in a 25pip range above 122.50, AUD/USD consolidated the rally after strong jobs figures in a 20pip range below 0.7140, and NZD/USD was in a 15pip range below 0.6550. Chinese Yuan midpoint setting was set weaker for 9th straight day, as China monetary authorities anticipate currency strength from potential inclusion into the SDR.

***Equities***

US equities / ADRs:

- USAT: Reports Q1 -$0.01 v $0.01e, R$16.6M v $15.0Me; +15.9% afterhours

- LPCN: Reports Q3 -$0.35 v -$0.34e (2 ests); +15.4% afterhours

- SYT: Reportedly has rejected approach from ChemChina; talks said to continue and are not exclusive to ChemChina - press; +12.8% afterhours

- CWEI: Reportedly Concho considering acquisition of CWEI - press; +5.5% afterhours

- YUM: Reports Oct China SSS +5%; Reiterates Q4 China SSS guidance of 0-4%; +4.3% afterhours

- ILMN: To be added to S&P500, replacing SIAL after the close on Nov 18th; +4.1% afterhours

- AMAT: Reports Q4 $0.29 v $0.28e, R$2.37B v $2.39Be; +2.8% afterhours

- PBR: Reports Q3 Net loss $1.1B v loss $2.2B y/y; Rev $23.2B v $38.8B y/y; +0.2% afterhours

- CSCO Reports Q1 $0.59 v $0.56e, R$12.7B v $12.6Be; -5.1% afterhours

- LOCO: Reports Q3 $0.18 v $0.15e, R$88.9M v $90.4Me; -8.3% afterhours

- BEBE: Reports Q1 -$0.16 v -$0.17e, R$96.3M v $93.1Me; To close up to 30 stores in FY16; -10.5% afterhours

- FOSL: Reports Q3 $1.19 v $1.13e, R$771M v $785Me; -15.6% afterhours

- JWN: Reports Q3 $0.57* v $0.72e, R$3.24B v $3.37Be; -20.9% afterhours

Notable movers by sector:

- Consumer discretionary: Sun Art Retail Group 6808.HK -3.2% (9-month result)

Nine Entertainment Co Holdings NEC.AU -3.4%, Southern Cross Media Group SXL.AU +0.9% (confirms talks with Southern Cross)

- Consumer staples: BGF retail Co 027410.KR -13.0% (Q3 result); Nissin Food Holdings Co 2897.JP +8.1% (H1 result)

- Financials: Samsung Life Insurance Co 032830.KR -3.1% (Q3 result); Sony Financial 8729.JP -1.2% (H1 result); T&D Holdings 8795.JP -1.1%?(H1 result)

- Industrials: Yue Yuen Industrial 551.HK -5.4% (9-month result); RUSAL PLC 486.HK -4.5 % (Q3 result)

- Technology: Quanta Computer 2382.TW -0.7% (Oct result); Hikari Tsushin, Inc 9435.JP -5.0% (H1 result); Toshiba Corporation 6502.JP -5.4% (writedown disclosure)

- Materials: Paladin Energy PDN.AU -3.0% (Q1 result)

- Energy: Showa Shell 5002.JP -1.3% (9-month result)

Most used buzzword... Uncertainty. More so than in previous years, investors are finding it difficult to construct a directional outlook. This is the corollary of extreme market volatility in 2014, and a series of unexpected and arguably inconsistent government actions. Uncertainty on the future encompasses:

· Uncertainty on the accuracy of official figures, particularly key metrics such as FX reserves & credit measures which are critical to making informed judgments on the vulnerability of the economy.

· Uncertainty on the reform agenda. Few doubt the government's dogmatism in pursuing reform, but questions remain on its likely pace and nature.

· Uncertainty on the government's ability to deliver reform in a manner that does not stifle economic growth.

Most bearish investors... International macro investors are the most negative on the Chinese market. International equity investors are also avoiding exposure, but are more nuanced as they can participate in pockets of structural growth. Local investors seem more constructive, and have more faith in the government's ability to manage the transition.

Biggest macro question... Will the RMB be devalued? Investors are divided between those who see devaluation as inevitable to maintain growth against the background of reform and imported monetary tightening, and those who do not. The latter group point to still considerable reserves, the willingness & ability of government to stimulate via fiscal policy, and the potential for competitive devaluations by other countries should they let the RMB fall.

Most discussed theme... New economy vs. old economy. Among equity investors there is a clear consensus to be long pockets of structural growth such as healthcare, education, leisure & ecommerce, and underweight resources, energy & capital goods. This has led to extreme positioning and valuations, and has likely exacerbated market volatility.

Most requested fieldtrip... Internet, closely followed by Consumer.

Most talked about stock... VIPShop. The leading flash sales company fits into favoured themes of ecommerce & millennials (in particular their desire for variety & value for money).

Brave contrarians... A few investors attempting to resist the temptation of the herd. Interesting, isolated suggestions include Macau gamers, asset managers, and property companies

After Hours Summary: USAT +15.9%, LPCN +15.5%, PLNT +13.1%, WLDN -23%, JWN -20.4%, PRTY -15.4%, FOSL -14.7% following earnings/guidanceAfter Hours Gainers:

Companies trading higher in after hours in reaction to earnings: USAT +15.9%, LPCN +15.5%, PLNT +13.1%, DAR +8.2%, XPLR +7.8%, BUFF +7.3%, RPD +6.8%, FGEN +4.3%, YUM +4.1%, HART +3.7%, AMAT +3.5%, CXRX +3.4%, PEN +1.8%, PBR +1.1%, SA +0.3%, CLIR +0.1%

Companies trading higher in after hours in reaction to news: LPCN +15.5% (FDA has assigned a PDUFA goal date of June 28, 2016, for co's NDA for LPCN 1021; FDA determined an Advisory Committee meeting was not necessary; co also reported earnings), SYT +12.8% (higher following reports that the company rejected a $42 bln acquisition offer), CTHR +5.6% (hired Suzanne Miglucci as President and CEO, effective December 1, 2015), CWEI +5.5% (seeing reports that Conco Resources (CXO) is bidding to acquire the company), ILMN +4.1% (to replace SIAL in the S&P 500), TWX +1.5% (seeing reports that Hulu is looking to sell a stake to Time Warner), RIO +1.5% (Reservoir Minerals reports it has entered into an earn-in and joint venture agreement with Rio Tinto relating to four exploration permits in the Timok Magmatic Complex)

After Hours Losers:

Companies trading lower in after hours in reaction to earnings: WLDN -23%, JWN -20.4%, PRTY -15.4%, FOSL -14.7%, BSQR -12.5%, BEBE -10.5%, LOCO -8.7%, TAHO -7.2%, VJET -6.2%, CSCO -4.9%, MSTX -3.5%, QTWW -2.9%, IMOS -2.8%, CPA -0.5%, KITE -0.3%, GLPG -0.2%

Companies trading lower in after hours in reaction to news: PAYC -5.2% (announced a secondary offering of 4.5 mln shares of common stock by selling stockholders), LGF -2.6% (filed for offering of 5 mln shares of common stock; part of transaction with Liberty Global (LBTYA) and Discover Lightning Investments announced on November 10), XRT -2.1% (released Holiday 2015 update; same store sales for the first week of November 'a bit slow'), OREX -1.6% (filed for 25 mln share offering of common stock for selling shareholders)