Wirecard, the German listed payments company, is to pay as much as €330m for a business which was barely involved in payments two years ago, according to Indian corporate filings.

Accounts for the largest subsidiary of the group to be acquired show qualified audit opinions due to concerns about revenue recognition and an inability to verify key financial totals, and recent resignations of directors and auditors.

Sales and profits claimed by Wirecard for the businesses it intends to buy also imply a dramatic transformation in financial performance during the last 18 months.

The question for shareholders, from whom Wirecard has raised €0.5bn in recent years to fund such dealmaking, is what exactly has it agreed to buy?

We’ve previously raised questions about the way Wirecard buys companies, undisclosed portions of previous deals, apparent mismatches between sets of accounts in different countries, the way the cash flow profile of the business is not what might be expected, and a large receivables balance obscured by adjustments the company asks analysts to make.

The company’s cash flow is under scrutiny, and analysts have been waiting to see how the group uses €360m raised from the sale of stock more than 18 months ago.

Wirecard’s purchase also comes at a time when investors are paying close attention to technology companies operating in distant jurisdictions after a series of controversies. For instance Globo, a UK listed group technology group placed into administration this month after the chief executive resigned and admitted “certain matters regarding the falsification of data and the misrepresentation of the company’s financial situation”. The collapse of the company followed a critical report published by a New York hedge fund which found claimed sales partners did not exist, including a Mumbai group which turned out to be a laptop repair specialist which hadn’t heard of Globo.

What Wirecard announced it would buy on October 27 is the fast growing payments business of Great India Retail, which includes the Smart Shop and iCashcard brands, and 60 per cent of GI Technology, a subsidiary operating prepaid payment cards. The company says these operations will have revenues of €45m in 2015, and €75m the year after. Earnings, on a pre-tax, interest, depreciation and amortisation basis will be €7m this year and then as much as €18m in 2016, Wirecard says. It will pay €230m initially, and up to another €100m dependent on future profits.

Wirecard told us “the main legal entities where the payment business of GI Retail Group were concentrated and which were acquired as part of the transaction are Hermes and GI Technology (of which Hermes is the main operative company/revenue generator and GI Technology is mainly the licence provider).”

The two main efforts are iCashcard and Smart Shop, what a spokesperson called “retail assisted ecommerce” — essentially kiosks where Indians can have someone interact with the internet on their behalf. Wirecard also says remittances are a big part of the business. To generate that €45m of sales expected this year, Wirecard said the ecommerce and remittances will transact about €2.8bn of payment volumes.

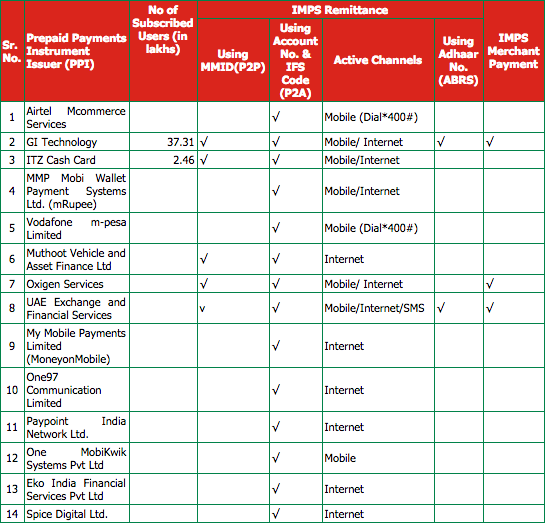

Wirecard also said “The National Payments Corporation of India (NPCI) ranks GI Technology as number one bank’s remitter among 123 members, as of 6th of October 2015.”

To do so, it must be growing very fast indeed. We could only find two references to GI Technology on the NPCI website. One is the number-light table to the right.

To do so, it must be growing very fast indeed. We could only find two references to GI Technology on the NPCI website. One is the number-light table to the right.The other is in a list of milestones of the Immediate Payment Services (IMPS) network run by the NPCI:

GI Technology Pvt. Ltd as a RBI authorized Prepaid Payments Instrument Issuer (PPI) joins IMPS – 4-Jun-13

Swift work to reach number one in under two and a half years. NCPI did not respond to a request for comment.

According to the most recent balance sheet available for GI Technology, at the end of March 2014 trade payables were 87m rupees, or about €1m, and trade receivables were about €0.24m. The group also lists 62m rupees of “security deposits”, up from 49m the year before.

GI Technology was granted a prepaid card license in 2009, but it was only in October last year that it amended its memorandum of association to make reference to remittances and foreign exchange.

What about the parent company, GI Retail? At the end of March 2014 its balance sheet lists reserves of 96m rupees (€1.2m), borrowings of €2m, de minimis cash, and investments of €3m, with the totals for each lower than reported the previous year, which suggests at that time it was neither a large or growing entity. There were zero trade receivables or trade payables. A further subsidiary, GI Hospitalities, filed a sparse balance sheet with no number larger than the 48m rupee (€0.6m) total for trade payables.

Which leaves Hermes, the main operating company which until recently described itself as a travel agent.

At first glance it looks substantial. The annual filing for the year to March 2014 details turnover of 15bn rupees (€185m). However it also describes the business as “travel arrangement tour operator and related services”, and discloses 13 product or services categories within that, with the “turnover of highest contributing product or service” for each. The largest is airline ticket booking, at 11bn rupees, followed by 2.8bn rupees for railway ticket bookings.

Yet those revenues are not what most companies would call revenues. The auditor qualified its opinion on the Hermes accounts, with revenue recognition cited as one of the reasons:

The Company’s major revenue is the commission it earns from online booking of air/rail /movie/ bus tickets and other support services which is in the nature of agency commission. As per Accounting Standard 9, gross commission earned should be taken as gross revenue and not the gross inflow of cash or sales value. However, the Company has followed the policy of recognizing gross inflow of cash from sale of tickets as sales value instead of taking gross commission earned as its revenue. This has resulted in the gross revenue overstated by Rs 1,520.17 crores (previous year Rs.1,118.70 crores) and gross purchase cost overstated by Rs.1,492.02 crores (previous year Rs.1,101.86 crores). This is the result of a decision taken by the management and caused us to qualify our audit opinion on financial statements since 2012-13. The effect on the financial statements on account of the same could not be quantified by us.

A crore is 10m rupees. Deduct 15,201.7m rupees from the reported (and audited) total of 15,334.2m rupees, and you are left with 132m rupees, worth €1.6m.

Wirecard said this is not correct. “After changing the revenue recognition from a gross basis (transaction volume processed) to a net basis (commission earned) the total revenue amounts to EUR 15.8m). However, there is no impact on gross margin and EBITDA in FY13/14 due to the change of revenue recognition.”

It gave us the following table of figures for what it is buying based on “audited and consolidated financial statements”:

The annual report to March 2014 also details recent efforts to get into payments, describing a change in policy at the Reserve Bank of India to allowing banks to use intermediaries to supply financial services. “To take advantage of the policy of the RBI, your Company took the initiative and signed up agreement with Yes Bank to act as their BCA last year and capitalised on it this year”.

Hermes’s current website describes itself as the exclusive distribution and recharge network for iCashcard. The March 2014 report describes Hermes signing up with iCashcard during the year, with revenues from iCashcard money transfer commissions totalling 9m rupees, worth €114,000.

The auditors also said the reasons for qualifying the opinion include a lack of verification of key financial metrics: “The Company has not obtained confirmation of balances in respect of Trade debtors, Trade payables, deposits, loans and advances outstanding as on March 31, 2014.”

Following that the memorandum of association was changed in November to include a paragraph detailing payment related services and remittances, then two of the directors of Hermes resigned in December 2014, both citing “personal reasons”. Wirecard said these were close relatives of the founder who were replaced for operational reasons as the company grew.

On 24 August this year longstanding Hermes audit firm Kuriachan & Nova, resigned “due to our pre-occupation on other assignments”. Another firm, V Krishnan & Co, was appointed auditor on the 28th. On the 31st it resigned, saying it was “not in a position to conduct the audit Individually thus resigning for being appointed as Joint Statutory Auditor.” On September 9th both firms were reappointed as joint auditors. Wirecard said the need for joint auditors was a reflection of the company’s growth.

In terms of the underlying businesses Matt Earl has already written a couple of postsat Lordship Trading looking at Great India Retail and Hermes.

The current Hermes Network website was created in May, according to whois data, and prior to that it had a different web address. One of the odd things Matt found from looking at the old site in the internet archive was earlier this year there was little mention of payments on the Hermes website, which described itself as a travel agent.

Hermes made its humble beginning in 2006 and went on to play an important role in the Indian travel industry through its innovative technology approach and its ability to build a nation wide network of traditional travel agents as well as a new set of non traditional agents who have taken travel closer to the common man in India.

Our attention was drawn to a box of “recent events”. In January this year the top event was news that Hermes had signed up with Yes Bank to provide money transfer services. Yet click on the read more… link and the internet archive takes us to a “recent news” page with what looks like headlines for 8 press releases (without links to the full release), all dated May 1, 2011.

The first of those has an unusual headline:

On the old website, in early 2014, Hermes listed three distribution channels, again travel focused:

Matt also compared GI Retail to an Indian competitor, Suvidhaa, which claims 80,000 retail outlets, to GI Retail’s 90,000.

In the year to March 2014, Suvidhaa reported 31bn rupees (€375m) of gross transaction value, income from operations of 377m rupees (€4.6m), but lost 89m rupees (€1m) at the bottom line.

Wirecard said “obviously the payment business of GI Retail was showing a stronger business performance than this competitor”.

Matt also finds a TV interview with the ceo of Suvidhaa, which compares with what some might regard as the surprising lack of Indian business coverage of the Wirecard deal. The Economic Times gave it a 60 word brief, while the Business Standard tookthe Reuters rewrite of the press release. Perhaps it’s because travel agent and ticket kiosks are pretty common in a big country with lots of people who lack internet access.

What then should we conclude?

The reason it’s important for auditors to verify key financial balances, such as trade receivables and trade payables, is as a check on the overall quality of the accounts. Were a company to overstate revenues and profits, it would then have to find a way to spend the fake cash created, either by inflating costs or the value of assets it buys.

Auditors can be fooled, Globo got a clean bill of health from Grant Thornton, for instance, but there were red flags prior to that: BDO resigned as auditor in February 2014, for instance, citing an inability to agree “audit scope in relation to our involvement in the work of component auditors”.

India is a fast growing economy, with e-commerce, payments and remittances all experiencing rapid growth. Wirecard investors will no doubt be reassured by what the company says was “intensive internal and external legal, financial and tax due diligence”. They may, perhaps, want to get a clearer picture of what the company is buying.