Closing Stock Market Summary

The stock market had a mixed showing today on below-average volume at the NYSE. The major indices traded in relatively narrow ranges, ultimately settling little changed from Friday. There was not a lot of conviction on either side of the tape as participants look ahead to influential events later in the week.

The standout events include more inflation data in the form of the March Consumer Price Index on Wednesday and Producer Price Index on Thursday.

This morning's release of the New York Fed's Survey of Consumer Expectations did not move the market much. The one-year-ahead inflation expectation remaining at 3.0% for the third consecutive month. At the three-year-ahead horizon, expectations increased to 2.9% from 2.7% while expectations for the five-year-ahead horizon dropped to 2.6% from 2.9%.

There was also an element of hopeful anticipation in play today in front of first quarter earnings results from some big banks ahead of the open on Friday.

JPMorganChase (JPM 198.48, +1.03, +0.5%), Wells Fargo (WFC 57.79, +0.39, +0.7%), and Citigroup (C 61.73, +0.13, +0.2%), which are among the names reporting earnings, logged decent gains today.

Other bank stocks outperformed in sympathy. The SPDR S&P Bank ETF (KBE) gained 1.5% and the SPDR S&P Regional Banking ETF (KRE) climbed 1.7%. The S&P 500 financials sector was among the top performers, rising 0.4%.

On a related note, strength in regional bank shares led to the outperformance of the Russell 2000, which closed 0.5% higher today.

Rising market rates did not dampen buying interest in stocks. The 10-yr note yield settled four basis points higher at 4.43% and the 2-yr note yield settled six basis points higher at 4.79%.

This price action was related in part to the market's ongoing recalibration of rate cut expectations, along with some hesitation in front of this week's Treasury sales. There is a $58 billion 3-yr note auction on Tuesday, a $39 billion 10-yr note auction on Wednesday, and a $22 billion 30-yr bond auction on Thursday.

There was no US economic data of note today.

- S&P 500:+9.1% YTD

- Nasdaq Composite: +8.3% YTD

- S&P Midcap 400: +7.9% YTD

- Dow Jones Industrial Average: +3.2% YTD

- Russell 2000: +2.3% YTD

Looking ahead, Tuesday's economic data is limited to the NFIB Small Business Optimism at 6:00 ET.

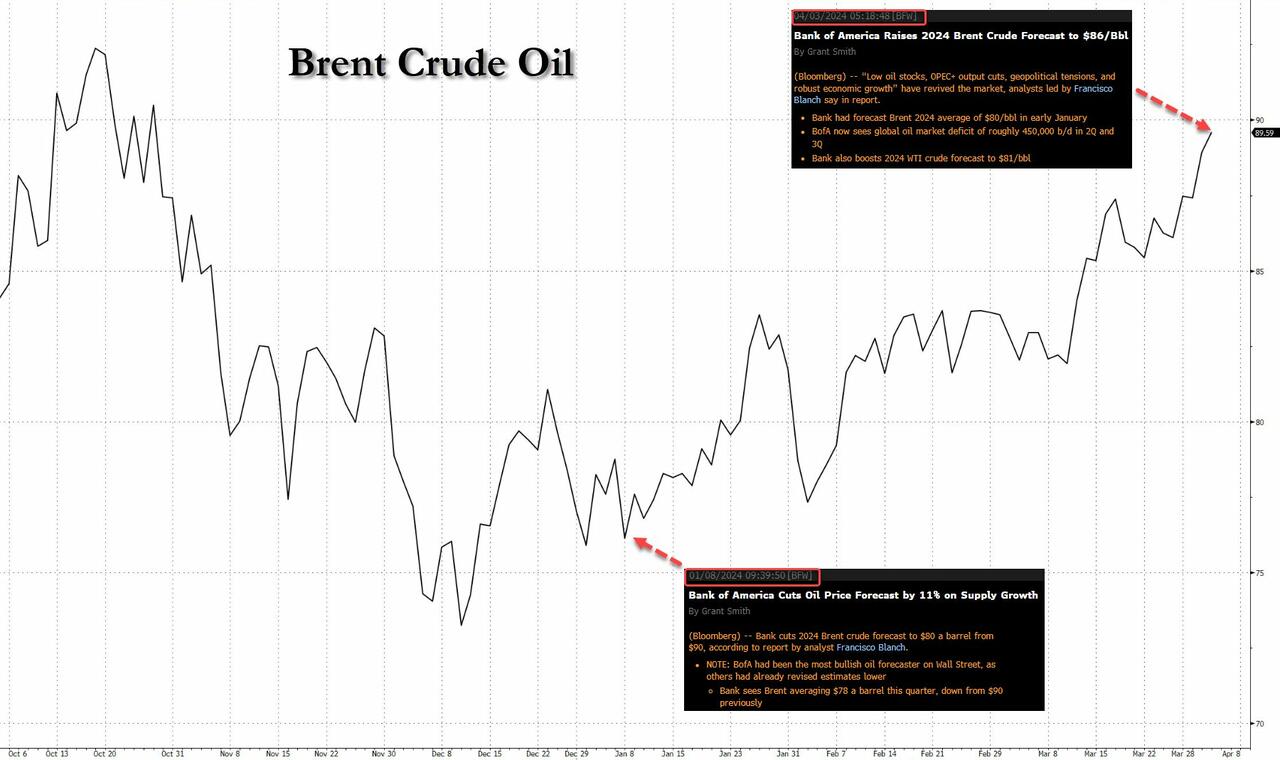

Here's What Will Push Oil Above $100/Bbl

Back in early December, just after Powell's dovish pivot shocked everyone, many closet oil bulls like BofA's energy strategist Francisco Blanch, predicted that a dovish Fed would send oil back to $100. Unfortunately for him, oil did nothing and just one month later, as no oil buying had materialized, Blanch threw in the bullish towel and cut his oil price forecast by 11%, ironically bottom ticking to the dot oil just as it was about to soar by 20% in the next three months, an ascent which was capped with... Blanch raising his Brent oil price forecast.

To be sure, BofA wasn't the only one to predict $100 oil: two weeks ago JPMorgan commodity analyst Natasha Kaneva was looking at Russia's unexpected pivot to producing less oil than it was allowed, and wrote that "the shift in Russia’s oil strategy is surprising" and "at face value, and assuming no policy, supply or demand response, Russia’s actions could push Brent oil price to $90 already in April, reach mid-$90 by May and close to $100 by September, keeping pressure on the US administration in the run-up to elections."

In short, the fate of Biden's re-election was now in the hands of Putin if the Russian leader wanted to push up the price of oil back to triple digits by limiting output, and the only recourse Biden has - according to JPMorgan - was releasing another 60 million barrels of oil from the SPR (see full JPM note here).

But it increasingly appears that $100+ oil is inevitable, regardless of what Putin does or does not do, and as Bloomberg writes over the weekend, the odds of $100 oil are rapidly rising, because while the recent surge in po; above $90 just days ago was blamed on escalating military tensions between Israel and Iran, "the rally’s foundations went deeper — to global supply shocks that are intensifying fears of a commodity-driven inflation resurgence."

Consider: a recent move by Mexico to slash its crude exports is compounding a global squeeze, prompting refiners in the US (the world’s biggest oil producer) to consume more domestic barrels. At the same time, American sanctions have stranded Russian cargoes at sea, with Venezuelan supply a potential next target. Meanwhile, Houthi rebel attacks on tankers in the Red Sea have delayed crude shipments, and despite all the "turmoil", OPEC and its allies are sticking with their production cuts.

It all adds up to a magnitude of supply disruption that has taken traders by surprise. The crunch is turbocharging an oil rally ahead of the US summer driving season, threatening to push Brent crude, the global benchmark, to $100 for the first time in almost two years; in fact the last time oil was trading there, Joe Biden was draining the SPR to the tune of several million barrels per week. That’s amplifying the inflation concerns that are clouding US President Joe Biden’s reelection chances and complicating central banks’ rate-cut deliberations.

For oil, “the bigger driver right now is on the supply side,” said Amrita Sen, founder and director of research at Energy Aspects. “You have seen quite a few pockets of supply weakness, and demand overall on a global basis is healthy.”

According to Bloomberg, oil shipments from Mexico, a major supplier in the Americas, slid 35% last month to their lowest since 2019 as President Andres Manuel Lopez Obrador tries to make good on promises to wean the country off costly fuel imports. The country’s exports of so-called sour crude — the heavy, dense kind that many refineries are designed to process — now stand to shrink even further as state-controlled oil company Pemex is now planning on cutting an additional 330 kb/d in May, Reuters reported citing sources.

That decision has roiled oil markets around the world. Mars Blend, a medium-density sour crude from the US Gulf Coast, has in recent days risen to a multi-year premium over lighter WTI, the national benchmark. Mars usually trades at a discount to WTI. Brent crude hit $90 a barrel on Thursday, the highest since October, and extended gains on Friday. JPMorgan said it could hit $100 by August or September.

Canadian Cold Lake oil priced at the Gulf Coast traded at the narrowest discount to WTI in almost a year. Key indicators for Middle Eastern medium-sour crude, such as Oman and Dubai contracts, are rallying too.

To be sure, it's not just Mexico's fault: back in February we first warned that long before hedge funds - all heavily short crude - realized what was coming, the physical market was screaming tightness with the Brent prompt spread exploding to a backwardation around 90 cents after tumbling to a multi-year low in late December.

And indeed, a closer look at oil supply showed that there was a clear drop off in production which would guarantee higher prices.

The sharp drop in output in early 2024 came before Mexico’s move, when we noted a sequence of supply disruptions both large and small: in January, a deep freeze ate away at crude output and inventories in the US at a time when they would normally grow, keeping stockpiles below seasonal averages through late March. Then, Mexico, the US, Qatar and Iraq cut their combined oil flows by more than 1 million barrels a day in March, tanker tracking data showed (Baghdad pledged to limit output to make up for non-compliance with prior pledges to OPEC+).

Also adding to the tightness, OPEC member the United Arab Emirates curbed shipments of its Upper Zakum, a medium-sour oil, by 41% in March compared with last year’s average, according to Kpler data. The state oil company is diverting more supplies of that crude to its own refinery, traders told Bloomberg. Though the cuts were expected and Abu Dhabi National Oil Co. is offering buyers another type of crude as a substitute, the decline in Upper Zakum exports is contributing to higher regional prices amid the broader OPEC+ curtailment.

Crude markets in Europe, meanwhile, were pressured higher by the Houthi attacks in the Red Sea, which sent millions of barrels of crude on a detour around Africa, delaying some supplies for weeks. Disruptions to a key North Sea pipeline, unrest in Libya and a damaged pipe in South Sudan also contributed to the rally, while US sanctions have deprived Russia of tankers that previously transported its oil to buyers including India.

Making matters worse for Biden who is absolutely terrified of higher oil and gas prices, the supply pinch could become even more acute in the weeks ahead. That's because Venezuela dictator Nicolas Maduro is showing no sign of heeding promises he made to Biden and other "democracies" to move toward free and fair elections, in response the Biden administration could reimpose sanctions this month, although it most likely won't as it would mean an even lower approval rating for the outgoing US president, confirming once again just how malleable and laughable western "democratic" ideals are.

The plunge in supply - which we warned about two months ago, and which has materialized now - is a stark contrast from just a few months ago, when oil plunged to multi-month lows as US production climbed and Russian seaborne crude exports ratcheted higher despite sanctions, which have since been expanded. The US Energy Information Administration, after forecasting global inventories to remain unchanged this quarter, now predicts they’ll fall by 900,000 barrels a day. That’s the equivalent to the production from Oman.

Putting it all together, Goldman - which has turned decidedly less bullish on oil ever since the firm's iconic commodity analyst Jeff Currie quit last year - last night published a report (available to pro subscribers) in which it said that the market is finally pricing in "firm demand and geopolitical supply risks, which together have boosted positioning and valuation."

And while Goldman expects Brent to stay below $100/bbl in its base case in which the bank assumes:

- already solid demand,

- no additional geopolitical supply hit, and

- that elevated spare capacity will lead OPEC+ to raise production in Q3.

... the bank warns that "geopolitical impediments to OPEC’s ability/desire to deploy spare capacity could send Brent above $100." Needless to say, when it comes to "base case" forecasts from Goldman's research desk (not to be confused with the bank's terrific Sales and Trading desk), they virtually always end up being wrong, which is why $100 oil is now virtually guaranteed.

Goldman also listed other reasons why Brent could reach $100, including i) the Russia-Ukraine or Middle East conflicts may damage upstream, midstream, or downstream oil infrastructure, and ii) Iranian oil supply may decline on disruptions or under a potentially more hawkish US.

Below we excerpt from the Q&A attached to the Goldman report (the full note is available to pro subs in the usual place).

Q. Why have crude oil prices rallied?Brent has rallied to $91/bbl because the market is now pricing in a firmer demand outlook and some geopolitical downside risks to oil supply, which together have boosted positioning and valuation.Upgraded market expectations of oil demand have fueled the rally.

- First, the IEA forecast of 2024 oil demand growth has crept higher on solid oil demand data outside China, and GDP upgrades.

- Second, sentiment about demand in investor conversations has turned from bearish to constructive.

- Third, oil prices have also risen after strong activity releases this week, including manufacturing surveys in China, the US, and India and US employment.

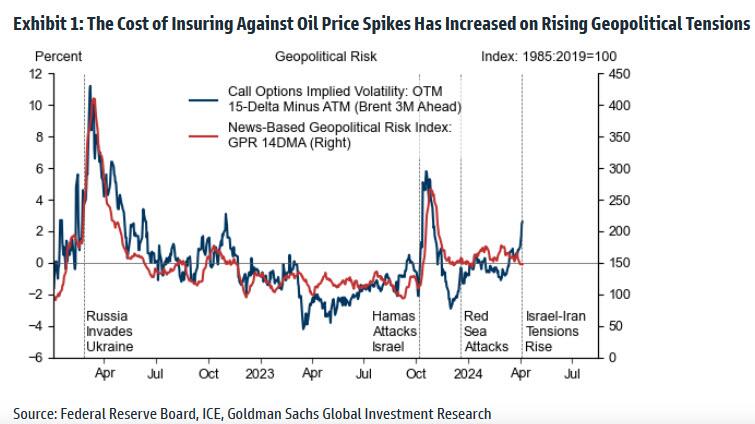

The geopolitical risk premium—the compensation investors demand for the risk that geopolitical shocks reduce oil supply—has also picked up following attacks on Russian refineries, and rising Iran-Israel tensions. That said, the cost of insuring against oil price spikes remains less elevated than in October 2023 and in 2022, because Middle East crude production remains unaffected by the war (Exhibit 1).As the market is now pricing in firm demand and geopolitical supply risks and as oil demand for inflation hedging has picked up, measures of positioning and valuation have risen sharply. Net managed money in crude and refined products has surged by over 400 million barrels since December (Exhibit 2). Our pricing framework suggests that actual Brent 1/36m timespreads have shifted from significantly undervalued in December to now modestly overvalued based on our nowcast of OECD inventories and our assumption of a modest 0.4mb/d Q2 deficit.

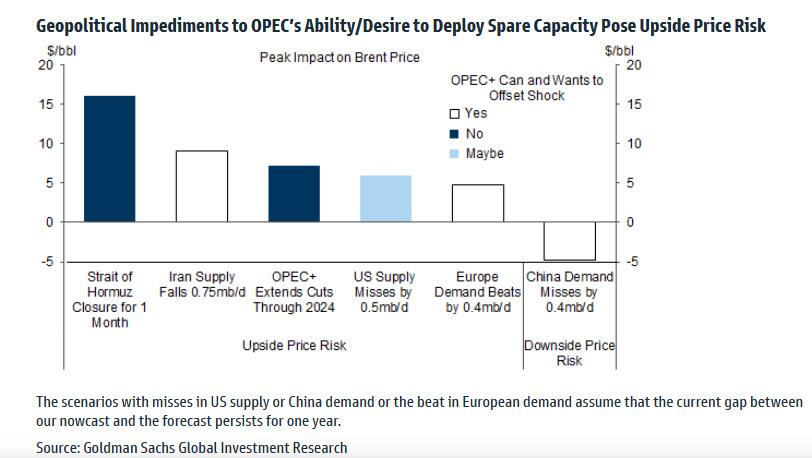

And the punchline: Q. What could push Brent oil prices above $100/bbl?

We see only modestly bullish risks to our non-OPEC+ balance from firmer demand in Europe, and likely temporary softness in US supply. In contrast, we believe that lower OPEC supply for longer, for instance because of geopolitical impediments to OPEC’s ability and/or desire to deploy spare capacity, could send Brent above $100 for some time.Specifically, we see upside risks to our 2023Q3 Brent forecast of $86/bbl in several potential geopolitical scenarios:

- OPEC+ may extend the existing production cuts further in a context of increased tensions between the West and several key OPEC+ countries

- The Russia-Ukraine or Middle East conflicts may damage upstream, midstream, or downstream oil infrastructure (as has happened to Russian refineries)

- Iranian oil supply may decline on disruptions or under a potentially more hawkish US Administration

- While highly unlikely, we estimate that an interruption of oil flows through the Strait of Hormuz would lead oil prices to rise 20% in the first month and eventually double if the interruption persisted for several months

Translation: not just Putin, but all of OPEC+ now controls the outcome of the 2024 US election.

Reid Hoffman, « athée mystique » et gourou de l’intelligence artificielle

Le cofondateur de LinkedIn invite l’Europe à davantage se positionner dans la course à l’IA opposant les Etats-Unis à la Chine, et dénonce la dérive libertarienne d’Elon Musk.

Le portrait pourrait classiquement commencer par le business : à 56 ans, Reid Hoffman fait partie de la « mafia PayPal », surnom donné à ces jeunes prodiges de la Silicon Valley, qui fondèrent avec Elon Musk et Peter Thiel la firme de paiement et firent le succès de la tech américaine des années 2000.

Cofondateur de LinkedIn en 2002, investisseur aux débuts de Facebook et d’Airbnb, venture capitaliste chez Greylock, ancien membre du conseil d’administration de la société d’intelligence artificielle (IA) OpenAI, Reid Hoffman est à la tête d’une fortune estimée par le magazine Forbes à 2,5 milliards de dollars (environ 2,3 milliards d’euros).

On pourrait poursuivre par la politique : à la différence de ses collègues libertariens, MM. Musk et Thiel, qui ont basculé aux confins de l’extrême droite, Reid Hoffman est un démocrate, qui fait tout pour s’opposer à un second mandat de Donald Trump : ainsi a-t-il contribué – en vain – à la campagne de son adversaire à la primaire républicaine Nikki Haley et financé – avec succès – le procès en diffamation intenté par l’ancienne journaliste du magazine Elle E. Jean Carroll, qui accuse Donald Trump de l’avoir violée.

Mais on a choisi d’engager la conversation par la philosophie, lors d’une rencontre d’une heure dans un hôtel chic au cœur de Manhattan, à New York. En ces temps de décollage de l’IA, Reid Hoffman estime que la technologie forge les générations et il fait partie de ceux qui veulent accélérer. « Quand on a inventé la machine à vapeur, on a créé la classe ouvrière et la classe moyenne. On ne veut pas retourner à la société de paysans. La génération qui grandit le fait avec l’intelligence artificielle. Les plus vieux s’inquiètent, mon Dieu, c’est neuf, c’est étranger. Les jeunes trouvent que c’est sympa, se disent : “Voyons ce que je peux en faire.” »

Lire aussi | Article réservé à nos abonnés Intelligence artificielle : « Sam Altman va-t-il réussir à maintenir le cap de la double mission d’OpenAI ? »

Dans un récent discours à l’université de Bologne (Italie), la plus vieille d’Europe, Reid Hoffman a comparé les temps actuels à la Renaissance, évoquant une « approche de la technologie profondément humaniste » : « Nous formons notre technologie qui, en retour, nous façonne et nous voulons le faire dans une direction qui nous rend plus humains. »

Bien sûr, les craintes sont évoquées. « Hollywood met toujours en scène l’homme contre la machine, et c’est toujours la machine la méchante », qu’il s’agisse de Terminator (1984), de James Cameron, avec Arnold Schwarzenegger, ou de HAL 9000, l’ordinateur d’IBM dans 2001 : l’odyssée de l’espace (1968), de Stanley Kubrick. Par le passé, l’innovation dérangea, tel le télescope de Galilée ou l’automobile, qui effrayait tant que « les gens agitaient des drapeaux orange à son passage ». Avant que les vertus de ces progrès ne soient exploitées.

« L’Europe qui essaye d’être arbitre »

Reid Hoffman, qui s’est amusé à écrire en 2023 un livre avec l’IA – Impromptu : Amplifying Our Humanity Through AI (« Impromptu. Amplifier notre humanité grâce à l’IA », Dallepedia LLC, non traduit) –, se décrit comme « athée mystique », car il reconnaît bien des mystères : « Les athées disent que le monde n’est que mécanique newtonienne. Clairement, le monde est plus intéressant que cela. Par exemple, on ne comprend pas la conscience. » Ce Californien a suivi un parcours éclectique qui fait de lui un personnage atypique dans la Silicon Valley.

Il raconte un séjour dans un internat progressiste du Vermont, Etat rural du Nord-Est : « Je suis allé à Putney School car ils essayent de former des êtres humains équilibrés. J’ai fait de la forge, du travail du bois, cela fait partie de moi. » Puis il étudie à la prestigieuse université de Stanford, en Californie, notamment en neurosciences. « J’en ai déduit qu’ils ne savaient pas bien ce qu’était le langage intelligent, je me suis dit que la philosophie aurait peut-être une réponse. Alors je suis allé étudier à Oxford [Royaume-Uni] et j’ai conclu que les philosophes ne savaient pas non plus ce qu’était le langage intelligent. Et que peut-être la meilleure façon d’y contribuer était de créer un logiciel. »

Dans l’aventure de l’IA, Reid Hoffman invite l’Europe à se mettre de la partie, notamment pour injecter son point de vue culturel. « Le monde et l’Europe seraient mieux lotis si l’Europe innovait aussi. » L’Amérique innove, le Vieux Continent régule, dit l’adage aux Etats-Unis. M. Hoffman répond par une cruelle plaisanterie : « C’est un peu comme s’il y avait un match de Coupe du monde de foot entre la Chine et les Etats-Unis avec l’Europe qui essaye d’être arbitre. Cela pose deux problèmes : d’abord, l’Europe ne peut pas gagner, ensuite personne n’aime particulièrement les arbitres. »

« Les Chinois ont deux ans de retard »

Reid Hoffman salue les projets français, en particulier la start-up Mistral AI, qui vient de signer un partenariat avec Microsoft. « Dans mes yeux d’Américain, ils sont très Français. » Pour lui, il est normal que ces jeunes prodiges aient fait leurs armes chez les géants de la tech américains pour apprendre. « Il n’aurait pas été possible de sortir seulement d’une université. » Côté allemand ? « [Il n’a] pas vu passer sur [s]es radars » un effort significatif en matière d’IA.

Le sujet, d’un point de vue américain, reste la concurrence avec Pékin. « On dit que la Chine pense en siècles. Ce n’est pas le cas dans la tech : ils pensent en semaines. C’est le seul endroit au monde où je trouve que la Silicon Valley va lentement. » Toutefois, la Chine a une sorte de défaut paradoxal, une faible capacité à la persévérance : « Ils pivotent très rapidement, mais ne s’engagent pas dans des projets de plusieurs années. » Pour l’heure, selon lui, en dépit de l’avance qu’ils ont sur les données, « les Chinois ont deux ans de retard » sur les Américains dans leur course à l’IA.

Ce retard s’explique aussi par les difficultés d’accès aux microprocesseurs, en raison des multiples embargos américains, tandis que Washington subventionne massivement cette industrie. « L’administration Biden veut être certaine que les Etats-Unis conservent leur avance dans ce domaine-clé », explique M. Hoffman, qui insiste sur l’impact de l’IA sur tout le tissu économique américain : « L’IA est notre seul espoir pour retrouver notre industrie manufacturière qui fit la classe moyenne. »

Dérive libertarienne d’Elon Musk et Peter Thiel

En revanche, il se dit réticent sur les logiciels open source, ouverts à tous, dans l’IA. « J’ai été au conseil de Mozilla [qui développe des logiciels libres] pendant onze ans [de 2005 à 2016], donc je suis très positif sur de nombreux sujets. Mais quand vous ouvrez des modèles à haute capacité, vous ne les donnez pas seulement aux journalistes, aux corps académiques, ce qui est bien. Vous le donnez aussi aux Etats voyous, aux terroristes, à des gens qui veulent attaquer l’écosystème de l’information ou la démocratie. Nous avons des vulnérabilités, je suis donc prudent. »

Vu les immenses capacités de calcul nécessaire, l’IA semble pour l’instant profiter aux géants de la tech (Nvidia, Microsoft, Meta, Google, Amazon, Apple, Tesla) rebaptisés les « sept magnifiques ». « J’investis beaucoup dans les start-up », précise Reid Hoffman. Celles-ci se greffent sur les géants, appelés à se multiplier.

« Si les sept deviennent trois, alors oui j’ai un souci. Mais si les sept deviennent quinze, c’est un progrès. » Et de vilipender la politique antitrust de la concurrence de l’administration Biden conduite par la présidente de la Federal Trade Commission, Lina Khan, qui multiplie les procès contre les géants technologiques de la Côte ouest : « Je m’élève largement contre cette politique antitrust, car elle poursuit l’effondrement et pas l’expansion », accuse-t-il, dénonçant « un usage peut-être pas illégal, mais immoral d’une position d’autorité pour entraver autant que possible les grandes entreprises de la tech ».

De même est-il sévère sur l’attitude de Joe Biden, qui ouvrit les hostilités contre Elon Musk en ne le conviant pas à un sommet sur l’électrique à la Maison Blanche à l’été 2021 sous prétexte que ses usines étaient non syndiquées. « Elon a tendance à être bagarreur. Et quand la gauche a commencé à l’attaquer, il a riposté comme Robert De Niro dans Taxi Driver [1976]. Mais faire un sommet sur la voiture électrique à la Maison Blanche sans l’inviter, c’est risible, grotesque ! », déplore-t-il. Et de pointer que l’effet est aussi désastreux auprès de la communauté de la tech, qui constate que la Maison Blanche est dans un déni de réalité pour faire plaisir aux syndicats. Au fil des trimestres, Elon Musk dérive, persuadé que l’enjeu est de créer une IA antiwoke. « Personnellement, ce qui m’obsède c’est d’avoir, grâce à l’intelligence artificielle, un système médical accessible pour tout le monde sur son smartphone. »

Reid Hoffman critique aussi la dérive libertarienne de MM. Musk et Thiel, qui semblent croire qu’on peut se passer d’Etat. « Vous avez déjà essayé d’être entrepreneur en Afghanistan ? C’est difficile non ? C’est là que je romps les rangs avec mes camarades de PayPal car je pense que oui, le gouvernement, cela compte. »

Pour l’élection présidentielle de novembre, Reid Hoffman fait feu de tout bois pour empêcher un second mandat Trump. « Je ne suis pas intrinsèquement démocrate contre républicain. J’ai financé toute une série de candidats républicains, la dernière en date étant Nikki Haley », l’ancienne gouverneure de Caroline du Sud qui briguait l’investiture républicaine face à Donald Trump. Sans succès. Alors, clairement, il votera pour Joe Biden, dont le bilan national et international est selon lui sous-estimé. « Etre vieux ne signifie pas être non fonctionnel », explique-t-il, et Joe Biden, pour lui, n’est pas « non fonctionnel » : « Absolument pas. En décembre [2023], j’ai passé des heures à discuter avec lui, de choses qu’il ne connaissait pas comme l’intelligence artificielle. Pourquoi avais-je besoin de déjeuner avec lui ? J’avais besoin de savoir cela. »

Labour denies plan for UK to rejoin EU customs union

Shadow minister says party ‘committed to making Brexit work’ after report from political consultancy on realignment

Tensions within Labour over its policy towards the EU burst to the surface on Monday after the party was forced to deny a report that it planned to re-enter a customs union if it wins the general election.

The paper from the Eurasia Group political consultancy cited unnamed “senior Labour insiders” as saying the party would seek to revive a high-alignment deal, originally brokered by former prime minister Theresa May but rejected by parliament in 2019, in a bid to boost economic growth.

“[That] deal is a first-term ambition. A de facto customs union by another name. It is the first step of where we’d want to get to,” one of the insiders reportedly said, adding they were reflecting new internal thinking on the EU relationship within the Labour leadership.

They added that if the opposition party won an October election with a large majority, as current opinion polls suggest, then Labour leader Sir Keir Starmer would travel to Brussels as early as December to signal his desire for a “fundamental upgrade” of the EU-UK economic relationship.

Labour quickly denied the briefing, which was sent to Eurasia Group clients on Monday morning, insisting that the party was sticking to its “red lines” on the EU, which include remaining outside both the single market and a customs union.

Nick Thomas-Symonds, the shadow Cabinet Office minister who is expected to be put in charge of Labour’s promised re-engagement with Europe if the party wins power at the next election, said the party position had not changed.

“Labour has long been clear that we are committed to making Brexit work. We have set out clear red lines on the future of our relationship with the European Union: no return to the single market, the customs union or return to freedom of movement,” he added.

Forging a customs union with the EU would require unravelling other parts of UK trade policy, including the trade deals signed with Australia and the 11-member Comprehensive and Progressive Agreement for Trans-Pacific Partnership.

Labour has promised to improve the EU-UK trading relationship, but within those “red lines”, saying it will seek a veterinary agreement to reduce border frictions for food products, improve touring opportunities for musicians and boost reciprocal access for professionals.

However, internal critics of the party’s stance warn that these moves are too limited and will not be sufficient to deliver the other planks of the party’s policy platform, including an industrial strategy and being the fastest-growing economy in the G7.

Under May’s rejected deal, the UK remained in a de facto customs union with the EU and committed to high levels of regulatory alignments in areas including environmental and labour standards — a position Eurosceptics rejected as too close to the bloc.

Mujtaba Rahman, managing director for Europe at Eurasia Group, who authored the client note, said any move to structurally deepen economic ties would require Labour to take a more proactive approach than at present.

“They would need to make an early and clear move with Europe after the election, but also make an argument to the UK electorate about the benefits such an arrangement would carry for UK trade and investment and Labour’s growth agenda,” he added.

Brussels would potentially be open to such a proposal, a person briefed on the European Commission’s approach to the UK told the Financial Times, and it is monitoring what might be possible under a Starmer government.

“It would be a massive negotiation, but there would be openness from the EU side,” they added. “There’s been quite a lot of thinking on the possibilities here . . . but there will naturally be strings attached, whether financial, trade or on freedom of movement.”

Illustration of Rishi Sunak uses a butterfly net to chase question marks and Xs in the sky

Several other Brussels-based officials said they were open to a deal but sceptical that Starmer would want to make the necessary compromises.

A customs union is possible “if conditions are met” said one EU official, but they warned there would be no special treatment for the UK.

London “would be bound by the European Court of Justice and surrender sovereignty”, said a second official. “Every time we made a new trade agreement it would automatically apply to the UK,” they added.

The 27 member states are generally in favour of closer ties with the UK but remain wary of reopening deals struck after years of bruising negotiations. “We have moved on,” said another diplomat.

Rate-Cut Delays Could Mean Dollar Stays Stronger For Longer

U.S. elections and geopolitical uncertainty could also lift the currency

Further signs of a solid U.S. economy and potential delays to anticipated interest-rate cuts could prolong the dollar’s strength, analysts said.

Many analysts and fund managers have been anticipating that the dollar would fall this year as the Federal Reserve starts to cut interest rates, but rate-cut expectations have been trimmed back sharply recently while U.S. elections and geopolitical uncertainty could also lift the currency.

“Doubts are spreading as to the ability of the Fed to cut rates at its June FOMC meeting,” Jane Foley, head of FX strategy at Rabobank, said in a note.

“This, combined with political risks, suggests the prospect of a stronger-for-longer dollar.”

Money markets show expectations of U.S. interest-rate cuts have been slashed to just 62 basis points this year from around 150 basis points at the beginning of the year, according to Refinitiv, as data continue to point to robust economic growth and stubborn inflation. This has kept Treasury yields elevated and supported the dollar.

Pimco favors the dollar over the euro and other European currencies such as the Swiss franc and the Swedish krona in anticipation of further evidence of the U.S. economy performing better than others, economist Tiffany Wilding and Andrew Balls, chief investment officer for global fixed income, said.

Jonathan Petersen, senior markets economist at Capital Economics cited a risk that U.S. economic growth and inflation could stay strong rather than soften as expected, forcing the Fed to keep rates high while other central banks reduce rates.

“This would be enough to push interest rate differentials (and the dollar) back towards levels last seen in late 2022,” he told Dow Jones Newswires.

“Our sense is that the tailwinds that have supported the dollar so far this year, notably the favourable shift in interest rate differentials, will gradually turn to headwinds.”

Capital Economics expects the DXY dollar index—which measures the dollar’s value against a trade-weighted basket of currencies—to decline to 98.34 by the end of 2024 and to 97.84 by the end of 2025.

The DXY index is last at 104.290, having hit a 20-week high of 105.100 on April 2.

Natixis Research forecasts a smaller fall in the DXY index, to 102.300 in six months and gradually declining to just below 100.000 in 15 months’ time.

Natixis forecasts 100 basis points of U.S. interest-rate cuts this year, below their previous estimate of 150bps. This is well above the 62 basis-point reduction currently priced by U.S. money markets, with a first cut almost fully priced in for July, according to Refinitiv, and above the Fed’s current forecast of 75 basis points.

“This will weaken the dollar, but less than initially expected, especially in the second half of the year,” FX strategist Nordine Naam and the economic research team of the French bank said in a note.

Saxo’s head of FX strategy Charu Chanana expects that the better performance of the U.S. economy versus its peers will start to fade and weigh on the dollar.

“U.S. economic data has been strong in the first quarter, but signs of weakness are emerging, potentially marking a turning point for the U.S. economy,” she said.

Saxo expects that a ‘soft landing’ for the U.S. economy, where inflation slows without causing a steep economic slowdown or recession, could bring with it a weaker dollar and it may be prudent to reassess long dollar positions.

This is based on the ‘dollar smile’ theory, where the dollar strengthens in periods of either economic prosperity or economic uncertainty, but weakens during periods of moderate growth.

However, there are concerns about how long dollar weakness will last.

“New risks loom on the horizon,” she said.

A Trump election victory “could potentially lead to a strengthening of the dollar due to tariff risks and safe haven flows,” she said.

Thames Water debacle holds a harsh lesson about asset pricing models

Investors should stop using an approach that many have long regarded as fundamentally flawed

It is rare these days to come across a climate change denier in the world of institutional investors — especially those who choose to invest in infrastructure, an essential lever of the energy transition and decarbonisation of the economy. Investors tend to believe the latest science on climate change. But, when it comes to asset pricing, strangely enough they often do not.

At the end of 2022, a group of large pension plans, including funds from Canada, Japan and the UK, discovered that they had lost a large part of the £5bn investment in Thames Water that they had recorded on their books. This Easter, they learnt that they had probably lost all of it.

There is only one way for a water utility serving the capital of a G7 country to lose so much value so fast: it was never worth £5bn to begin with.

Yet its owners denied this reality for years. The signs that Thames Water and its parent Kemble Water Finance constituted a high-risk, low-profit business were there all along. The cost of capital in this investment should have been considered quite high (and increasing over the years) and its value much lower.

A key reason why the risks of investing in Thames Water were ignored is the continued use of invalid asset pricing approaches for reporting its “fair value”.

For instance, many investors in private assets — and in this case the water sector regulator, Ofwat, too — rely on the “capital asset pricing model” (CAPM) to estimate a cost of capital and the value of the business (and for Ofwat the allowed level of water tariffs).

This model states that the cost of equity of a company is a function of the expected return of “the market” and how much this company correlates with it or its “market beta”. Today, CAPM remains the most commonly used framework for estimating the value of private investments like infrastructure companies.

Yet the scientific community has known for more than 30 years that CAPM, while one of the foundations of the field of academic finance, is wrong. That’s right: the model used by most large valuation firms, many private asset managers and the regulators of UK network utilities has been proven not to work.

CAPM relies on a very abstract notion of “market portfolio” and does not fit the market data. It has been shown time and again that better models can be used to explain asset prices, and that these approaches have led to the creation of entire new industries from hedge funds to factor investing. What is more, the way CAPM is used to value private assets often makes a mockery of the original model by relying on inputs that seldom have any relationship with the actual investment.

The inevitable conclusion from all this is that the reported values of private investments held by institutional investors and their managers today are very likely to diverge significantly from their true market value, and do not represent the level of risk taken or the liquidation value of these assets. This is how investors in Thames Water saw their investment go from £5bn to zero in a few months — they were blindsided by bad models and bad data. In other words, they ignored the science.

Some will point out that these values are audited. This is correct but also irrelevant. Auditors validate a process, not the content of the valuation exercise. Did you use a well-known asset pricing model? Tick. Did you adjust for the asset illiquidity? Tick. It is not for the auditors to say which asset pricing model is the correct one, what the “illiquidity premium” is or if the level of interest rates used corresponds to current market levels.

Sticking to these practices amounts to denying the science and the importance of risk when it comes to the market value of private assets. As with climate change, the costs of this denial are increasingly becoming larger, as private assets represent a greater share of the portfolio of investors.

There is a better way. Applied financial research and data availability about private investments have made significant progress since CAPM was developed in the 1960s. It is time for investors in private companies like Thames Water to take a more scientific view of asset pricing. They need proper measures of risk for the private asset classes to which they now allocate large amounts, and of the value of the assets they hold.

After all, these underpin the value of everything from defined benefit pension rights to defined contribution lump sums, life insurance policies, wealth management and many other products. And for all of these there is, ultimately, a fiduciary responsibility to report the true market value of what’s sitting in your clients’ portfolios.