It's Time To Pay Attention To Funding Risks Again

Authored by Simon White, Bloomberg macro strategist,

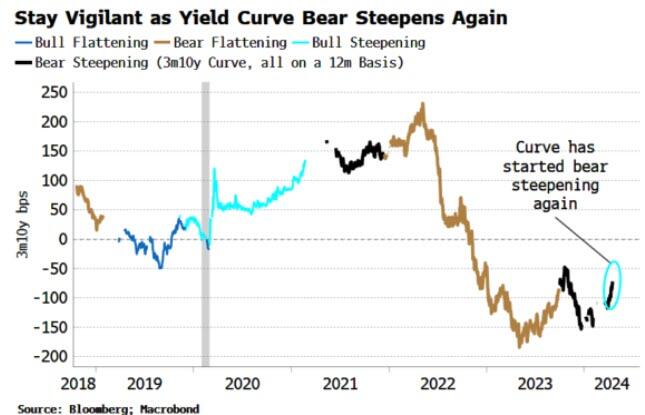

The risk of a squeeze in US funding markets is increasing as the yield curve bear steepens, i.e. longer-term yields rise more than short-term ones. More attractive bill yields and climbing interest-payment costs on government debt are depleting reserves and reducing their velocity, increasing the chance of a disorderly upswing in funding rates, as well as posing a risk to the stock market.

The bond market intimidates everybody, in the oft-cited words of Bill Clinton’s chief strategist James Carville. That description is apt today as rising yields reverberate across the financial system. Funding risks are intensifying again, increasing the chance of a rate-volatility driven correction in stocks.

Concerns about funding issues have been in abeyance for most of this year, but it is time to sit up and take notice again as the backdrop becomes more pernicious. The bear steepening of the yield curve is a double whammy, accelerating the rate of reserve depletion through a declining reverse repo facility (RRP) and rising government interest payments.

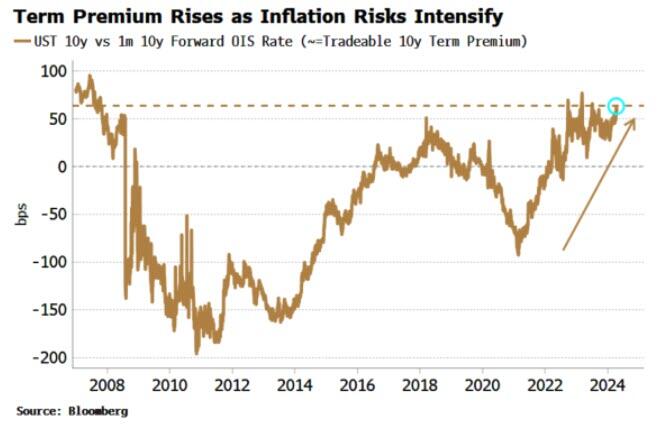

The curve has been bear steepening in the 3-12 month versus 10-year sectors as inflation fears drive term premium higher, with the measure now close to levels last seen in 2008 (using tradeable forward OIS rates rather than “academic” term premium).

A bear steepening is particularly problematic in the current set-up.

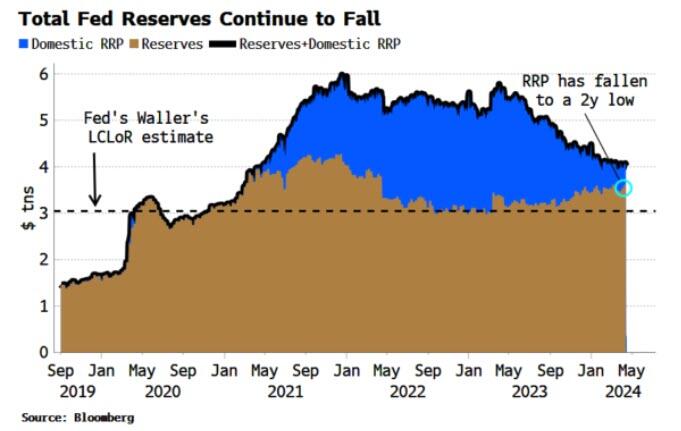

First note that the RRP has been hugely important in keeping risk assets supported despite the fastest rate-hiking cycle for decades and ongoing QT.

The Treasury’s decision to pivot issuance toward short-term bills allowed money market funds (MMFs) to tap the more than $2.5 trillion liquidity idling in the RRP to fund the government. That prevented enormous public issuance crowding out other assets, and allowed the rally in stocks and bonds to continue.

But the RRP falling and eventually going to zero is a harbinger total reserves overall are potentially nearing their so-called lowest comfortable level — with estimates for the LCLoR ranging from about $2.5 to $3 trillion — where abrupt and acute funding problems become more likely. This week the domestic RRP fell as low as $327 billion, and is now at $440 billion, the lowest levels it has reached since June 2021, taking the sum of reserves and the RRP to just over $4 trillion.

The RRP has been declining as six-month and 12-month bill yields have been rising in response to the market reducing the number of rate cuts expected from the Fed, making bills more attractive to MMFs relative to the RRP facility.

Some of the RRP’s recent fall has also likely been driven by seasonal tax payments. But that should not mask the clear downwards trend in the facility and its rising volatility. It would not be the first time that a telegraphed non-risk becomes a real risk precisely because peoples’ guards are down.

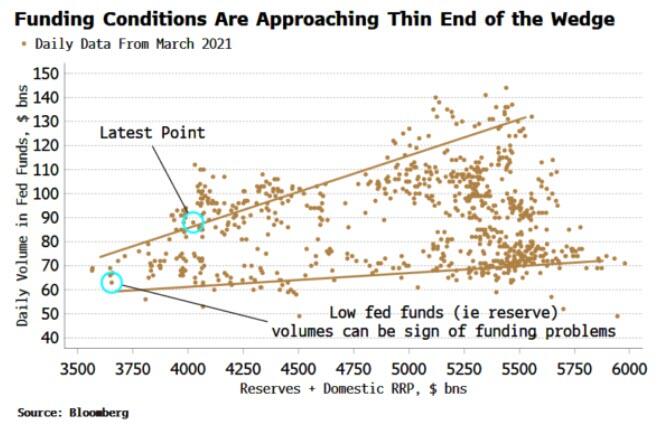

That’s potentially the case today. As I noted in a column earlier this year, a portent of previous funding episodes was a sharp drop in funding volumes immediately preceding a rapid rise in them, similar to a tsunami wave. As the chart below shows, when the total amount of reserves + RRP declines, volumes in fed funds (i.e. reserves) tend to also decline.

Further falls in fed funds volumes would be a sign that funding problems are potentially fomenting.

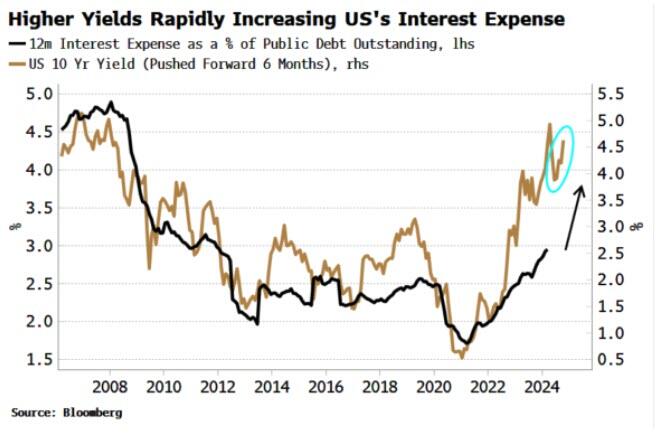

Rising longer-term yields are the other side of the coin in the bear steepening. The US government’s interest-rate bill is climbing rapidly, and is now over $1 trillion on an annual basis. This is set to grow much higher.

The 10-year yield gives us a near real-time barometer for the US’s annual interest expense. The recent rise in yields projects the expense will soon double to almost 5% of total debt outstanding, or over $1.7 trillion - i.e. about the GDP of Australia each year in interest.

Here lies the rub: to pay that interest, the government needs to tax and borrow. But that is an ever-greater drain on reserves and their velocity, accentuating the effects of the Fed’s ongoing QT program.

You might ask why that is the case given the interest is paid to bond holders and is therefore re-injected into the economy?

But that’s unlikely to be so for two reasons.

- The first is that the corporate and household sectors, the two most likely to spend interest back in the domestic economy, together only account for about 10% of UST holdings. The much larger financial and foreign sectors are more likely to save the proceeds, or spend them abroad.

- Second, reserves that end up as savings are of lower velocity, especially if they were originally higher-velocity bank deposits used to pay taxes. The more that interest payments percolate through the system, the more they end up with holders who have an increasingly lower propensity to spend them.

Thus a bear steepening squeezes the RRP and outstanding reserves — as well as their velocity — in a pincer movement, increasing the risk of a funding episode.

The last such major squeeze was in September 2019. It’s notable that in the days running up to that, the yield curve was bear steepening (in fact, it was in the top 1% of eight-day rises for the 2s10s curve going back 2000).

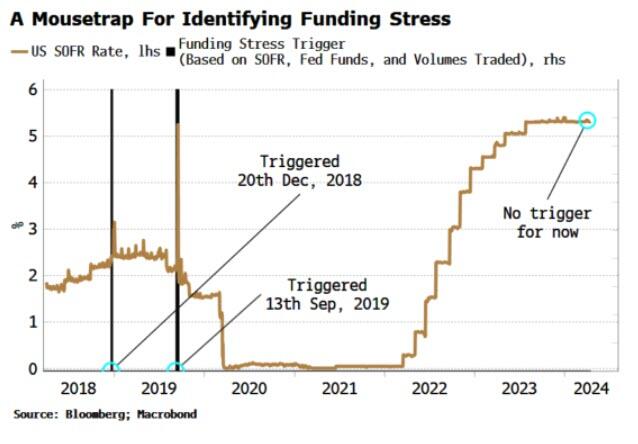

The bear steepening therefore means we should once again be vigilant to funding risks, and keep a close eye on the Funding Stress Trigger shown below.

The signal is inactive at the moment and the SOFR rate is currently well-behaved, but that can change quickly. In the last two major funding flare ups in 2018 and 2019, there were very few signs of what was to come, with the signal triggering only a few days before rates started to spike higher.

Funding stress would also be likely to increase rate volatility, which in turn would lead to higher stock-index correlation. That means a higher VIX, increasing the likelihood of a market correction as the stock perpetual motion machine shudders to a halt.

The potential risks, of course, may not come to pass, and funding markets continue to operate smoothly. But there are enough ex ante reasons to justify heightening one’s senses. The bond market may be intimidating, but a bear-steepening yield curve in the current market set-up is especially menacing, and should be watched closely.

23andMe CEO Anne Wojcicki Plans to Take Company Private

The DNA-testing company’s enterprise value is less than zero as its shares close at a new low

Anne Wojcicki is seeking to take her DNA-testing company 23andMe ME 43.04%increase; green up pointing triangle private after three years in public markets that saw the once-hot company’s valuation collapse from a high of $6 billion.

Her intentions were revealed in a public filing late Wednesday, which stated that she is working with advisers to help craft a potential deal and intends to speak with potential partners and financing sources. The filing said she would oppose any other buyer taking over the company. She holds 49.99% voting power in the company, which would make it all but impossible for anyone else to buy it.

News of Wojcicki’s plan drove 23andMe stock up 40% to $0.50 per share in early trading Thursday. They had closed Wednesday at $0.36, a record low that translated to a market capitalization of about $200 million. 23andMe had more than that amount of cash in the bank at the end of its last reported quarter. At the lower share price the company’s enterprise value was negative.

Wojcicki declined to comment.

The cratering of its stock reflects the many challenges facing its business. Its DNA tests aren’t as popular as they once were and lose money. 23andMe has tried to create a recurring revenue stream from its tests by offering a subscription product, but that has fallen far short of the company’s sales goals since customers only need to take its test once.

Wojcicki pivoted the company into prescription drug development, hoping to use its massive DNA database to discover new pharmaceuticals. But drug discovery is a cash-hungry business in which prospects can take a decade to pay off. The company has enough cash to last until 2025 at its current rate of spending. It has potential drug candidates in the pipeline, and taking the company private while securing additional financing could give it more leeway to get them to market.

An effort to offer medical care has also sputtered as the company has yet to fully integrate the telehealth company it acquired that was meant to anchor that service.

Wojcicki co-founded the company in 2006. She took over as sole chief executive in 2009 after pushing out her co-founder and has seen the company through other challenges, including a run-in with the Food and Drug Administration in 2013. The agency halted sales of its health test, citing a risk of false reports but later cleared them after the company spent millions validating its health reports.

Nasdaq last year threatened to delist the company’s shares.

Spanish beauty group Puig aims for €14bn IPO

Family-owned company looking to sell up to 24% of its share capital

Spanish beauty group Puig, which owns brands such as Paco Rabanne and Charlotte Tilbury, is set for the biggest initial public offering in Europe so far this year with a valuation target of up to €14bn.

The family-owned company said it was aiming to start share trading on May 3 and gave an expected range for its market capitalisation of €12.7bn to 13.9bn.

It is aiming to sell up to €3bn of shares, putting 21 to 24 per cent of its stock in the hands of outside investors. The founding Puig family will retain a majority stake.

The 110-year-old Barcelona-based business will list in Madrid and on other Spanish stock exchanges with bankers at Goldman Sachs and JPMorgan leading the process.

Puig said it would use the proceeds “for general corporate purposes such as refinancing the acquisitions of additional ownership interest[s] in Byredo and Charlotte Tilbury and supporting the growth strategy of the company’s brands and portfolio”.

Both Byredo, a cult Swedish fragrance group, and Charlotte Tilbury, a British make-up brand associated with its eponymous founder, were acquired by Puig during a deal spree encompassing 11 companies in 12 years.

The acquisitions have been overseen by Marc Puig, chair, chief executive and grandson of the company’s founder, who opened the business in 1914 after a German submarine sunk a ship carrying the merchandise of his previous venture.

The base of the offer is about €2.6bn of shares but Puig is offering Goldman an “overallotment” option to purchase a further €390mn.

Bookbuilding begins on Thursday and will end on April 30. The final price of the shares will be determined after the bookbuilding process is complete, the company said.

Marc Puig has led the company since 2004 and said he would be the last generation of the family to head the business, though he has no current plans to step down.

Explaining the IPO rationale this month, he said: “We believe that the balance of being a family-owned company that is also subject to market accountability will allow us to better compete in the international beauty market during the next phase of the company’s development.”

In another big European IPO, shares in skincare group Galderma began trading in Switzerland last month.

Iran warns of shift in nuclear stance if Israel threatens atomic sites

Revolutionary Guards issue warning as US announces new sanctions

Iran has warned Israel it is likely to review its nuclear stance if its atomic facilities are threatened, as tensions rise following the Islamic republic’s weekend drone and missile attack on Israel.

Iran’s Revolutionary Guards said on Thursday that Tehran may “reconsider” its nuclear policy, which it has long insisted is purely peaceful but which western powers say has put it on the threshold of becoming a weapons state.

The warning was issued as the US announced new sanctions on Iran’s drone programme in response to Saturday’s strike on Israel.

“Reconsidering the nuclear doctrine and policies of the Islamic Republic of Iran . . . is probable and imaginable, if the fake Zionist regime threatens to attack our country’s nuclear centres,” said Major General Ahmad Haq Talab, who oversees the security of Iran’s nuclear installations.

His comments were published in the semi-official Tasnim news agency, which is affiliated with the Revolutionary Guards, Iran’s most powerful military force.

Regime hardliners have previously threatened that during periods of heightened tensions with the west Iran could withdraw from the Non-Proliferation Treaty, which governs countries’ nuclear facilities.

Haq Talab warned Israel that any aggression against Iran’s facilities would be reciprocated at Israel’s nuclear weapon sites — which the Jewish state has never acknowledged possessing.

Israel has pledged to respond to last weekend’s Iranian attack, in which more than 300 missiles and drones were fired at the Jewish state.

That assault prompted Washington on Thursday to announce sanctions on 16 individuals and two companies that aid the production of unmanned aerial vehicles, such as drones, in co-ordination with measures announced by the UK.

“We are committed to acting collectively to increase economic pressure on Iran,” US President Joe Biden said, adding that his administration “will not hesitate to take all necessary action” to hold Tehran accountable.

“Our allies and partners have or will issue additional sanctions and measures to restrict Iran’s destabilising military programs,” Biden said.

Tehran said it launched last weekend’s attack — its first ever direct assault on Israel from Iranian soil — in retaliation for a suspected Israeli air strike on its consulate building in Damascus, which killed seven Revolutionary Guards members, including two senior commanders.

The US and other western allies have been pressing Israel to show restraint amid fears that the hostilities between Iran and Israel risk triggering an all-out Middle East conflict.

Israeli Prime Minister Benjamin Netanyahu said on Wednesday: “I want to make it clear — we will make our own decisions, and the State of Israel will do everything necessary to defend itself.”

Israel has given no indication of the timing or scale of its response, while Iran has vowed to retaliate against any Israeli strike on the republic.

“We are on the edge of a regional war in the Middle East,” EU foreign policy chief Josep Borrell warned at a G7 foreign ministers meeting on Thursday, as he called on Israel for “a restrained answer to the Iranians’ attack”.

Netanyahu has repeatedly threatened over the years to take action to prevent Iran acquiring a nuclear weapon.

The US-based Arms Control Association said in a paper this week that targeting Iranian nuclear sites “would be a reckless and irresponsible escalation that increases the risk of a wider regional war . . . and is more likely to push Tehran to decide that developing nuclear weapons is necessary to deter future attacks”.

Tehran and Washington have been locked in a nuclear crisis since then president Donald Trump in 2018 unilaterally abandoned the deal that Tehran signed with world powers, imposing waves of sanctions on the republic.

Under the 2015 accord, Iran agreed limits on its nuclear activity and a strict International Atomic Energy Agency monitoring regime in return for sanctions relief.

But after Trump withdrew the US from the agreement, Tehran responded by aggressively ramping up its programme, installing advanced centrifuges and enriching uranium to a purity of 60 per cent — the highest ever level in Iran.

Experts typically cite 90 per cent purity as weapons grade, but Iran has already taken the most difficult technical steps to reach that point.

Efforts by the Biden administration to revive the 2015 accord floundered and Iran has developed the capacity to produce enough fissile material required for a nuclear weapon in about two weeks.

In September, the US and Iran agreed to a prisoner exchange and Washington unfroze $6bn in Iranian oil money. It was hoped that the foes would build on those deals to agree to de-escalatory steps, including Iran agreeing to cap its uranium enrichment.

But any hopes of progress were dashed by Hamas’s October 7 attack and Israel’s retaliatory offensive in Gaza. In the months since, Iranian-backed militants have attacked Israel and US forces in the region as hostilities have intensified across the Middle East.

Israel has traded daily fire with Hizbollah, the Lebanese militant group and Iran’s most important proxy, and targeted Revolutionary Guards members in Syria.

The IAEA still has inspectors in Iran, but the UN watchdog and western governments have repeatedly accused Tehran of not co-operating with the agency.

Iran’s nuclear chief Mohammad Eslami told reporters on Wednesday that the republic could be still committed to the 2015 nuclear agreement if other signatories met their promises to ease sanctions on Iran. He said the head of the IAEA would “soon” visit Iran to “update” mutual agreements.

Amundi heads west in bid to be Europe’s BlackRock

Victory Capital deal will nearly triple US assets under management

Any up-and-coming pop star knows: it is tough to break America. A number of financial institutions have tried to crack the US over the years. Not many have succeeded. Amundi, with aspirations to be Europe’s BlackRock, is making its bid for scale stateside.

It has a long way to go. Catching US rivals such as BlackRock and Vanguard would require hugely bulking up its roughly $2tn of assets under management, a fraction of those peers. But the French asset manager, controlled by Crédit Agricole, is taking to their turf.

The group agreed this week to take a 26.1 per cent interest in Victory Capital Holdings, a $2.8bn US-listed fund manager. This deal should not only nearly triple its assets under management in that huge market, but also improve its profitability there.

This looks smart. No cash will change hands. Amundi US will combine its $104bn of AUM, and its roughly $1.2bn of revenues, with Victory’s client assets to create a $279bn manager with distribution throughout the US and Europe. In return, Amundi receives shares in Victory. Though more than two-fifths of these are non-voting shares, Amundi ends up with two of the nine director seats on the US company’s board. This structure helps circumvent US regulations when globally significant banks, such as Crédit Agricole, own fund management companies.

One can see the attraction for Amundi. First, Victory has a similar business model to its French suitor: buy, integrate, then repeat. It oversees 11 different businesses and its market value has nearly tripled to some $2.9bn in five years. Second, Victory’s cost to income ratio at 49 per cent should help dilute the 60 per cent plus ratio of Amundi US, created from its 2017 purchase of Pioneer Investments from Italy’s UniCredit, points out Tom Mills at Jefferies.

Full details of the transaction are not yet available. But the two sides put the valuation of the Amundi US business and the stake in Victory, once the latter has issued more shares, at about $1bn. On that basis, Amundi will have traded its US business for the equivalent of 1 per cent of its AUM, well above the 0.6 per cent at which the overall group trades.

European investors in asset managers would normally gulp at the thought of growth through acquisitions. The likes of Janus Henderson and Jupiter provide reason for pause. But at least Amundi’s deal, with its announced (pre-tax) cost cutting of $100mn offers hope for a better outcome.

Amundi has a long way to go in terms of its overall ambitions. But this looks a low-risk step along the way.

Gapping down

In reaction to earnings/guidance:

In reaction to earnings/guidance:

- EFX -9.1%, SNV -7.9%, LVS -3.9%, MCRI -3.3%, SNA -3.2%, BHLB -3.2%, FNB -3.1%, KEY -2.3%, TFIN -2.2%, BX -2.2%, TSM -1.5%

Other news:

- CAN -23.9% (files $300 mln mixed shelf securities offering)

- LAC -23.7% (prices offering of 55.0 mln shares of common stock at $5.00 per share)

- PHAR -8.5% (announces the launch of an offering of approximately €100 million convertible bonds due 2029 and the concurrent repurchase of the outstanding €125 million convertible bonds due 2025)

- BHVN -4.6% (prices offering of 5,609,757 of common shares at $41.00 per share)

- ITCI -2.7% (prices offering of 6,849,316 shares of its common stock at $73.00 per share)

- TSLA -2.2% (plans to layoff 285 employees at Buffalo plant, Reuters citing WARN notice)

- CAAP -2% (reports March traffic)

- VIGL -1.7% (presents findings from ILLUMINATE & IGNITE studies)

- ACAD -1.4% (presents new DAYBUE (trofinetide) clinical data)

- TWKS -1.3% (acquires technology and talent from Watchful)

- IBRX -1% (files mixed shelf securities offering)