The technical warning signs of equity weakness are clear to see. For the past several weeks, I have been voicing technical concerns about the stock market. This year seems to be a market where the adage of "Sell in May and go away" is applicable. What puzzles me is the lack of a fundamental trigger for the decline.

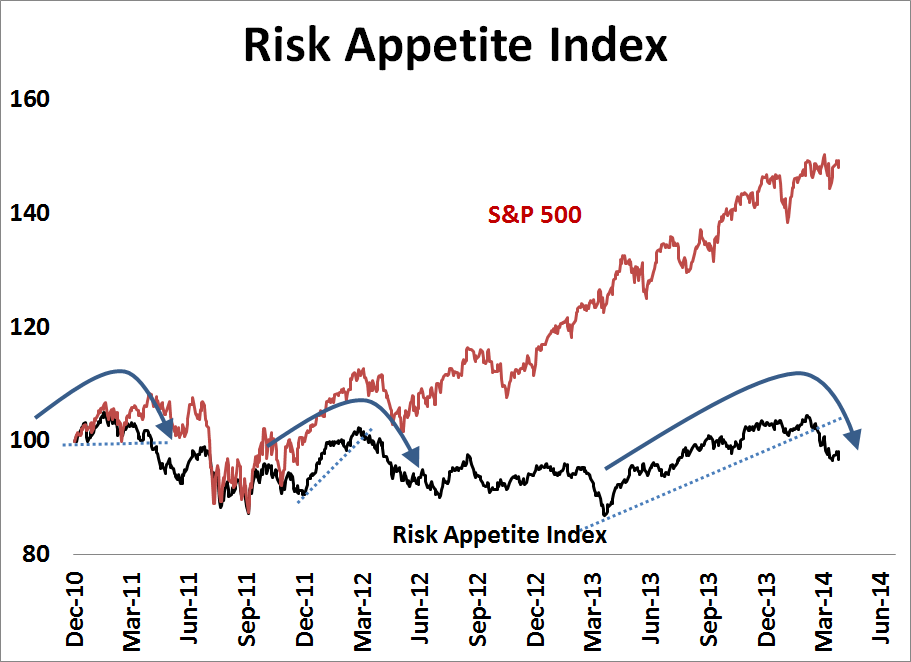

Risk appetite is fallingIn early April, I wrote about risk appetite rolling over (see

Bears 2 Bulls 1and

A case of risk exhaustion?). My Risk Appetite Index, which consists of an equally-weighted long position in the NASDAQ 100 and Russell 2000 (high beta risk-on index) minus an equally weighted short position in the defensive sectors of Consumer Staples, Telecom and Utilities (low beta risk-off index), continues to decline. The chart below shows that the index also displayed similar behavior (trend line breaches and general weakness) ahead of the market corrections in 2011 and 2012.

(click to enlarge)

Rising volatilityUnderlying the weakness of the risk appetite index is a change in sector leadership from the high-beta sectors like Tech, Consumer Discretionary and Financials to defensive sectors like Utilities and Consumer Staples (see

Interpreting a possible volatility regime shift). As well, I highlighted a possible regime shift where equity volatility appears to be headed higher. As knowledgeable readers know, volatility is inversely correlated with stock prices.

(click to enlarge)

Deteriorating internals

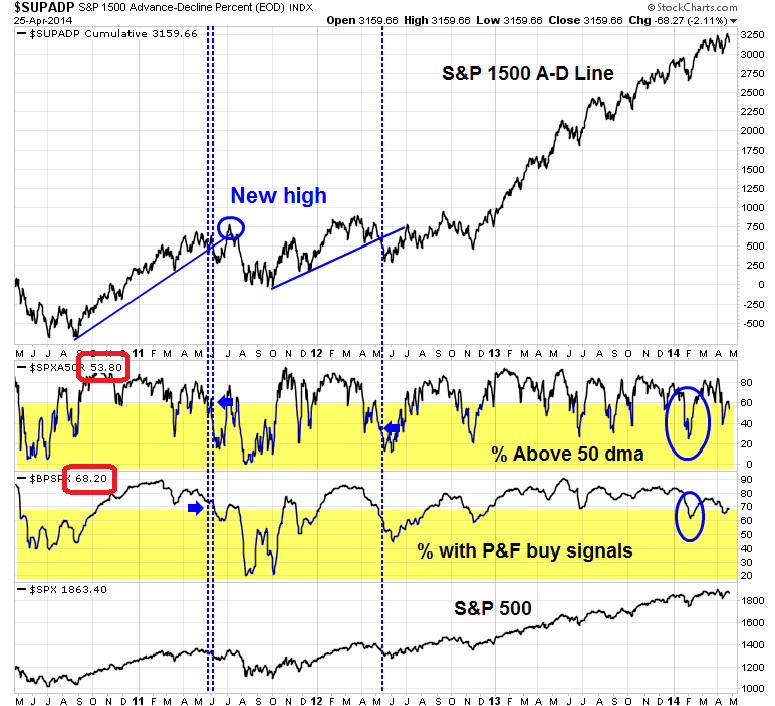

What has puzzled me is the robustness of the Advance-Decline Line, which has continued to make new highs as these signs of market weaknesses appeared. While the weakness in the A-D Line can warn of major bear markets, it is less effective in spotting corrective action as it failed to flash warning signs in the market declines of 2011 and 2012.

The chart below tells the story. The top panel is the SP 1500 A-D Line, the second the % of stocks in the SPX above their 50 day moving averages, the third % of stocks in the SPX with point and figure buy signals and the four panel the SPX. In the decline of 2011, which was sparked by the combination of worries over a eurozone debt crisis and political impasse in Washington, the A-D Line did breach an uptrend line, but rallied to make a new high shortly after. The shallow correction of 2012 was also accompanied by a breach in the A-D Line uptrend, but the breach did not provide any advance warning of the decline, which was similar to the 2011 experience.

(click to enlarge)

The combination of the % of stocks above their 50 DMA and % of stocks with point and figure buy signals can provide some warnings of weakness, but these indicators are somewhat iffy as well. The condition of the % of stocks above their 50 DMA is less than 60% (currently 54%) and % of stocks with point and figure buy signals is less than 70% (currently 68%) has been present in past corrective periods. These two indicators flashed a warning sign when the market weakened in February, but that was a false signal as a major correction did not follow.

Todd Harrison: Smart money is sellingIn addition,

Todd Harrison pointed out that the so-called Smart Money Flow Index is ominously bearish. The SMFI is defined in the following way:

The Smart Money Flow Index (SMFI) is calculated by taking the price of the Dow Jones Industrial Average at 10 a.m. on any given day, subtracting it from the previous day's close, and adding it to the next day's closing price. The first 30 minutes represent "emotional buying," driven by greed and fear of the crowd; smart money typically waits until the end of the day. If/when the DJIA makes a new high that is not confirmed by the SMFI, there is usually trouble ahead.

In other words, SMFI measures money flow by ignoring the movement in the Dow in the first half hour. While I would not necessarily characterize the first half hour of trading as dominated by dumb money, it is certainly emotional money. The chart below of the SMFI tells the story. While the Dow (in orange) has been holding up relatively well, SMFI has been dropping precipitously since mid March:

This second chart shows a longer-term perspective. The top panel shows the Dow and SMFI, as above, back to 2005. The green line on the bottom panel shows the spread between the Dow and SMFI - and the spread is as negative as it was in 2007.

Harrison followed up with a caveat to his analysis:

You will notice that we are still at levels last seen in 2007, which may prove to be a false "tell" but should, at the very least, be considered when making financial decisions.

Following the midterm election year patternWhen I put these technical patterns together, the stock market seems to be following the historical pattern of a midterm election year.

Ryan Detrickshowed the typical pattern of such years, where the market peaks out in late April and bottoms out in September.

The good news is that the bottom in the Fall has historically been a durable bottom and a superb buying opportunity for stocks, as per this analysis from

J.C. Parets:

(click to enlarge)

Bullish fundamentalsWhile the technical picture is warning of a major correction, what puzzles me is the lack of a fundamental trigger for a decline. The U.S. economy is behaving relatively well and seeing signs of a snap-back of winter related weakness. So far, Earnings Season has not proved to be a major disappointment. As per

Bespoke, the EPS beat rate is 62%, which is in line with historical average. On the other hand, the sales beat rate is a bit low at the 50% mark. Across the Atlantic, the ECB looks like it may finally edge towards QE, which should be supportive of European equities.

Jeff Miller summed up the "Sell in May" hysteria perfectly here:

The seasonal slogans often substitute for thinking and analysis. The powerful-looking chart that leads today's post actually translates into a 1% monthly difference in performance. The "good months" gain 1.3% on average while the "bad months" gain about 0.3%.

The bear case then rests on a case of risk exhaustion and unwind (see

A case of risk exhaustion), which is a funds flow driven bearish trigger. Any resulting correction would likely be brief and possibly sharp, which would be a good buying opportunity.

The 2011 parallel?

Nevertheless, the technical picture is a stock market that is poised to decline, but needs a bearish trigger. One historical parallel would be the events of 2011. In 2011, market internals started to deteriorate before the bearish triggers manifested themselves. The proximate cause was rising tail-risk of a eurozone crisis and debt ceiling fight in Washington. Rising fear of the dire consequences of these events served to crater stocks, but neither of these Apocalyptic scenarios ever materialized.

If 2011 is a parallel, then perhaps the answer is to consider the possibility of the markets pricing in rising tail-risk, namely Russia-Ukraine and a China meltdown.

Russian tail-riskI have discussed the tail-risk from the Russia-Ukraine situation before.

Ambrose Evans-Pritchard wrote that the U.S. is preparing sanctions that could bring the Russian economy to a screeching halt by freezing the external financial transactions of Russia and Russian companies:

An elite cell at the US Treasury has developed an arsenal of financial weapons that can in theory bring even large countries to their knees through use of "scarlet letters" that cause global banks and insurers to pull back. Japanese banks are already retreating from Moscow to pre-empt problems with US regulators.

In a separate article,

Evans-Pritchard indicated that western energy companies like

BP and Shell (

RDS.A) may have trouble operating in the U.S. should the next stage of sanctions be imposed. It would be measures like these that would spook the markets and force a re-pricing of Russian related tail-risk.

Sources in Washington say the US Treasury may soon extend the black list to Igor Sechin, president of the oil giant Rosneft, the biggest traded oil company in the world. Any such move would be a costly headache for BP, which owns 19.75pc of Rosneft's shares under a deal reached in 2012 ending its stormy misadventures in TNK-BP. It is unclear whether BP could continue to operate in the United States or even carry out its global business smoothly if it continued to be a Rosneft shareholder with Mr Sechin still in charge, yet it would be difficult to find buyers for a holding worth $12.5bn in the midst of a crisis. America's Exxon Mobile would have to reconsider its drilling plans with Rosneft in the Arctic `High North'. The US Treasury is also eyeing some form of sanction against Gazprombank, the financial arm of the gas monopoly Gazprom. This would greatly complicate Shell's joint operations with Gazprom at Sakhalin Island and in the Arctic, though this would depend on the exact wording and how the US Securities and Exchange Committee chose to enforce it.

Zero Hedge has also speculated that the U.S. may target Putin's personal $40 billion stash. The

ZH postulated Russian response would be to retaliate in kind, regardless of whether Putin's personal funds are involved in the sanctions:

Russian presidential adviser Sergei Glazyev proposed plan of 15 measures to protect country's economy if sanctions applied, Vedomosti newspaper reports, citing Glazyev's letter to Finance Ministry. According to Vedomosti as Bloomberg reported, Glazyev proposed:

- Russia should withdraw all assets, accounts in dollars, euros from NATO countries to neutral ones

- Russia should start selling NATO member sovereign bonds before Russia's foreign-currency accounts are frozen

- Central bank should reduce dollar assets, sell sovereign bonds of countries that support sanction

- Russia should limit commercial banks' FX assets to prevent speculation on ruble, capital outflows

- Central bank should increase money supply so that state cos., banks may refinance foreign loans

- Russia should use national currencies in trade with customs Union members, other non-dollar, non-euro partners

In other words, a full-blown scorched earth campaign by Russia.

While I tend to take anything published at ZH with a grain of salt, they may not be that far off this time. Oleg Babinov of The Risk Advisory Group wrote the following in March about the Crimean crisis and the likely response from the Kremlin is roughly in line with the proposals outlined in ZH (via

Moscow Times):

If Russia does not rush in to incorporate Crimea as its "administrative unit" and the sanctions are limited to its dropping from Group of Eight and some limited visa sanctions and asset freezes for politicians and businessmen who are directly involved in separatist activities, Russia's response would be relatively small-scale. If this is the case, there will be little effect on investors, except those who may be involved in cooperation with Russian companies in the field of military technology - but this is possible only if the U.S. and the European Union do not decide to freeze cooperation with Russia in this field. But if sanctions are applied to Russian state-owned companies and banks, Russia might want to retaliate by freezing foreign companies' accounts here. There was an announcement that the constitutional law committee of the Federation Council has invited legal experts to study whether such sanctions would be legal, but no draft law has been produced yet.

The greatest risk is surely an "asymmetric" riposte by the Kremlin. Russia's cyber-warfare experts are among the best, and they had their own trial run on Estonia in 2007. A cyber shutdown of an Illinois water system was tracked to Russian sources in 2011. We don't know whether US Homeland Security can counter a full-blown "denial-of-service" attack on electricity grids, water systems, air traffic control, or indeed the New York Stock Exchange, and nor does Washington. "If we were in a cyberwar today, the US would lose. We're simply the most dependent and most vulnerable," said US spy chief Mike McConnell in 2010. The US defence secretary Leon Panetta warned of a cyber-Pearl Harbour in 2012. "They could shut down the power grid across large parts of the country. They could derail passenger trains or, even more dangerous, derail passenger trains loaded with lethal chemicals. They could contaminate the water supply in major cities, or shut down the power grid across large parts of the country," he said. Slapstick exaggeration to extract more funds from Congress? We may find out.

For now, these scenarios are all speculative and remain tail-risks. However, should the events in eastern Ukraine spiral out of control, watch for the markets to start pricing in the possibilities of these risks - and they could be the trigger for a significant sell-off in the equity markets.

China: Whistling past the graveyardThe tail-risks in China are also rising. It all starts with problems in the overbuilt property market.

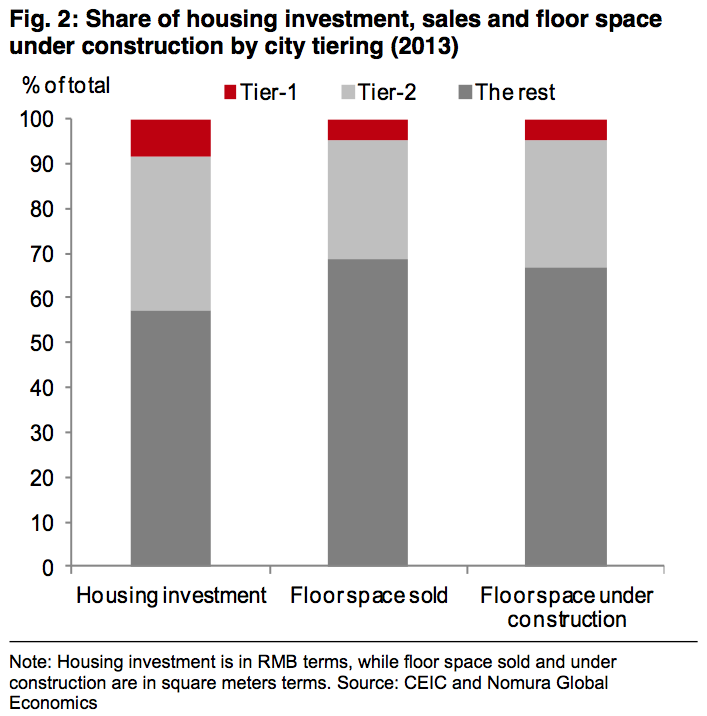

Nomura estimates that in 2013 alone, China added roughly

400 square feet of new construction per urban resident:

Zhang Zhiwei, chief China economist at Japanese investment bank Nomura, said in a

report last month that after building around 13.4 percent more floor space every year for the past several years, the country finally has too much housing. Zhang estimates about 2.6 billion square meters (about 28 billion square feet) were added in 2013, or 400 square feet of new residential floor space per urban resident.

These charts from

Nomura show the scale of the overbuilding, even by developed market standards:

Despite the apparent overbuilding, expansion is continuing, especially in the smaller cities:

(click to enlarge)

The overbuilding was not a problem until property prices started to cool off this year. The price decline is particularly acute in the Tier 3 and 4 cities (via

Xinhua):

The slowdown of the property market that was mainly seen in China's third- and fourth-tier cities last year has spread to more areas, and analysts warn of a tough 2014 for developers.

Figures released by the National Bureau of Statistics (NBS) last Friday showed that 178.25 million square meters of residential property were sold in the first quarter, down 5.7 percent year on year.

Falling prices in the real estate market feeds into problems in the financial system:

Added to the property market woes is the credit crunch for both developers and buyers.

Stringent bank loans since the end of last year have dealt real estate firms, medium- and small-sized ones in particular, a blow in securing their fund chain, said Hu Baosen, board chairman of Central China Real Estate Ltd.

A credit crunch is developing:

Meanwhile, banks have not loosened their control over personal housing loans, making it more difficult to purchase property on mortgage.

Among the 35 major cities surveyed by Centaline Property Agency Ltd., 25 have seen their banks suspend housing loans.

While I have heard China bulls say that a cooling property market does not present that much of a problem because most real estate is not purchased with debt, there are secondary financial effects from suppliers such as the steel industry, which is suffering from over-capacity, and other producers of construction materials. The balance sheet of these companies are not pristine and have substantial debt. These credit risks are now manifesting themselves in the form of defaults in the shadow banking system, which leads to a credit crunch, which can result in cascading defaults and... you get the idea.

Patrick Chovanec believes that the Achilles heel of the Chinese financial system is declining property prices. That's because Chinese lenders lend based on collateral value, which is mostly property based, rather than cash flow because financial statements are unreliable:

If China's housing market crashes, the ripple effect could be even more cataclysmic for its economy than the recent housing market collapses in the US and Europe were for their economies. A fifth of outstanding loans and a quarter of new loans are to property developers, says Nomura; untold billions more have been lent out off bank balance sheets. As falling prices crimp margins, small developers-like the one in the news this week-will start defaulting.

But the fallout will be bigger still, says Patrick Chovanec of Silvercrest Asset Management. "Not only is property important because it's a key component of that investment boom, but it's essentially the asset that underwrites all credit in the Chinese economy, whether it's local government loans, whether it's business loans," Chovanec says, explaining that lenders require "hard" assets as collateral because financial accounts can easily be doctored.

Western banks are not immune to a financial crisis in China. Aggregate foreign currency denominated debt totals about USD 1 trillion (see

EM tail-risks are rising). Should events spiral out of control, the financial damage may not be limited to the Chinese banking system and financial contagion could very well spread throughout the global banking system.

Even as the economy slows and cracks appear in the financial system,

Premier Li Keqiang has stated that the government is not considering any large scale stimulus programs but rely on targeted mini-stimulus instead:

Chinese Premier Li Keqiang said his government is not considering any strong stimulus measures or policies which would risk enlarging the fiscal deficit but will push through reform in order to support economic growth.

"There is no consideration about expanding the deficit or using 'strong stimulus,'" Li said, adding that China's official "proactive" fiscal and "prudent" monetary policy biases won't change. "But the government won't do nothing. It will rely on reforms, structural adjustments, to increase effective supply and meet new demand," he said. His comments, which were published late Wednesday, were delivered at a State Council meeting at which the executive decision-making body decided to lower the reserve requirement for some rural financial institutions. That move, which analysts expect to pump a miniscule CNY15 billion into the market, may bring relief to a struggling corner of the financial system but isn't expected to do much to shore up the broader economy.

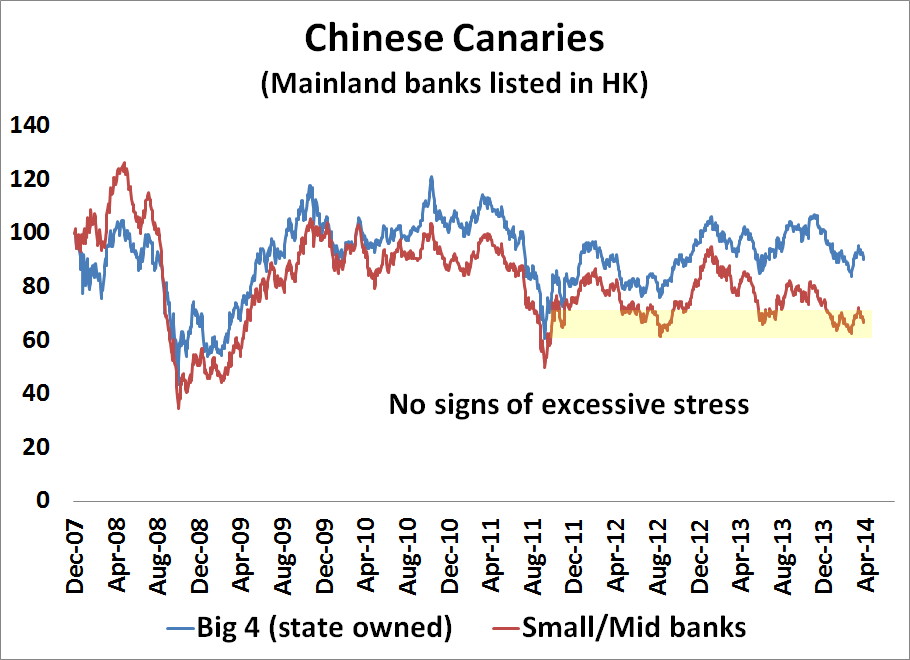

In the meantime, the markets are relatively relaxed about looming financial tail-risk. My so-called Chinese canaries, the prices of HK-listed Chinese banks, are not showing signs of extreme stress:

(click to enlarge)

In addition,

Reuters reports that there are few takers for tail-risk insurance on China (emphasis added):

Selling insurance against a financial crisis should not be difficult, five years after the last one nearly wrecked the global economy.

But when it comes to China, the world's second-largest economy, the probability of a full-blown crisis is apparently so remote that hardly anyone will buy an insurance policy against it, no matter how cheap. Financial wizards have been trying to sell peace of mind to investors in China for years, but fewer and fewer of those investors are interested, despite some worrying headlines.

In the past few months alone, China has seen its first domestic bond default, a small bank run, its weakest export performance since the global financial crisis, a marked slowdown in its property market and a rise in labor unrest. Steve Diggle, a Singapore-based hedge fund manager who crafts strategies to protect investors against financial catastrophes, says investors have faith that the Chinese government, armed with almost $4 trillion in foreign exchange reserves, will simply not allow things to get out of hand. He had to close down a fund that used to bet on doomsday outcomes in Asia last year.

While I am not saying that catastrophe in China is my base case scenario, it seems that the markets are whistling past the graveyard of a Chinese hard landing. Should the Chinese situation deteriorate, the possibility of a stampede for the exit is very real - and could be the trigger for a sudden downdraft in the price of risky assets.

Something's not right...

As I mentioned, market internals started to deteriorate before the eurozone crisis fully developed in 2011. Then, the trigger was worries about a Greek default and the possible repercussions on the euro, as well as a political impasse over the debt ceiling in Washington.

One possibility for 2014 is that the markets would follow the midterm election year pattern of a 10-20% summer correction into September or October. Already, the market technical picture is flashing warning signs. The trigger might be a combination of risk exhaustion by fast money accounts and rising tail-risk from one of these aforementioned events.

Despite the positive fundamental backdrop, my inner investor is siding with the technicians and he is becoming increasingly cautious. The technical message from Mr. Market is, "Something is not right about this bull." If the fundamentals were to hold up equity prices, then the technical outlook would improve and he would re-adjust his portfolio accordingly.

Jeff Miller's prescription of what to do sounds about right to him:

To make a wise decision you need to make an objective quantitative comparison between the economic trends and the small seasonal impact. The Great Recession has been followed by a slow and plodding recovery. We have an extended business cycle with plenty of central bank support. Since I am expecting the current cycle to feature (eventually) a period of robust growth, I do not want to miss it. The 1% seasonal effect will be minor in a month where we get a real economic surge.

If instead we get the typical sideways market with some volatility, it is a perfect environment for selling short-term calls against attractive, dividend-paying stocks.

My inner trader, who is more aggressive, is watching the developing head and shoulders pattern and waiting to the break to put on a leveraged short position on the market.

(click to enlarge)

Just be aware that developing head and shoulders patterns often fail and they do not become bona fide patterns until they are triggered. The bearish trigger is a breach of neckline support, which is at about the 4000 level. Should that occur, the downside target would be in the 3600-3650 region.

Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. ("Qwest"). The opinions and any recommendations expressed in the blog are those of the author and do not reflect the opinions and recommendations of Qwest. Qwest reviews Mr. Hui's blog to ensure it is connected with Mr. Hui's obligation to deal fairly, honestly and in good faith with the blog's readers."

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this blog constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or I may hold or control long or short positions in the securities or instruments mentioned.