I saw the newest Star Wars movie last week and it brought back memories that stretch back almost four decades. Watching Harrison Ford and Carrie Fisher on the screen reminded me of my age, though, once I learned how much Ford made for being in this episode, I understood the movie's story line much better. As I came out of the theater, though, I decided that it would be fun to update a valuation I did of the Star Wars franchise in 2012, when Disney acquired the rights from Lucas Films.

The Movies- Box Office Bonanza

If you are one of the few people on the face of the earth that has not followed the Star Wars story, it began in 1977 when George Lucas produced the first Star Wars movie, the fourth episode in what he saw as a six-episode series. That movie made history and remains one of the highest grossing movies of all time. It was followed in 1980 by the fifth episode, The Empire Strikes Back (my favorite), and in 1983 with the sixth in the series, The Return of the Jedi. Those first three movies created an entire generation of Star Wars fans, who then had to wait 16 years for the first in the series, The Phantom Menace (my pick for the worst of the series), which was followed by Attack of the Clones in 2002 and Revenge of the Sith in 2005. The six movies represent one of the most valuable movie franchises of all time, generating billions of dollars in box office receipts, with the appeal spreading globally.

The movies are shown in chronological order and the box receipts on the first three movies include the collections from their re-release in theaters in the 1990s.

The Add-Ons - Bigger than the Movies?

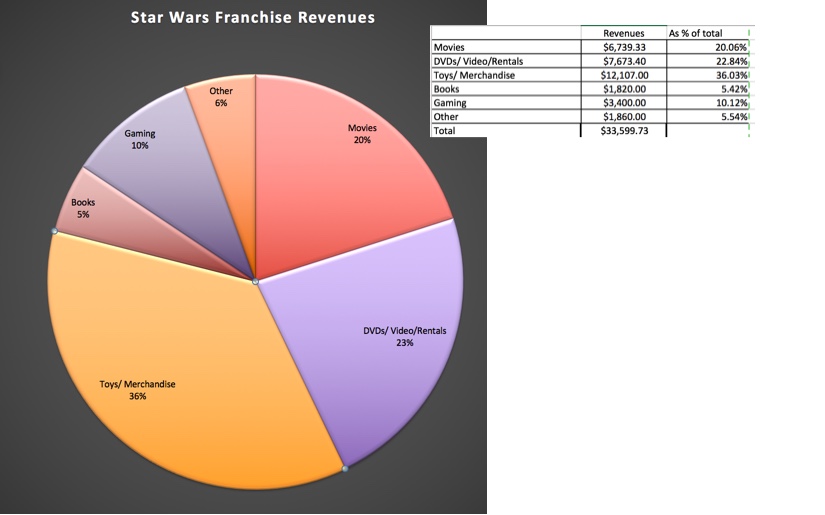

If you stopped just at box receipts, Star Wars might not be the most valuable franchise at all time, lagging the James Bond movies and perhaps even the Harry Potter and Lord of the Rings franchises. It is the magnitude of the add-ons to box receipts that make Star Wars unique and as someone who has partaken in all of them, I can attest to their power. I have owned the Star Wars tapes and DVDs, collected every Star Wars figure made, played Star Wars video games (very badly) and even used a GPS with a Yoda voice to drive from New York to Chicago (I love Yoda but he is a really bad navigator). The Star Wars empire stretches far and wide to include:

1. VHS/DVD/Rentals: The additional revenue from this stream reflects as much the hold that Star Wars has had on our collective imaginations, as it does the changing of technologies for home video watching over the decades. Starting with video tapes (VHS) sales and rentals in the 1970s, morphing into DVD sales in the last decade and continuing into streaming in today's environment, this add-on has generated $7.7 billion (unadjusted for inflation) in revenues.

2. Toys and Merchandise: This is the crown jewel of the franchise, as toy and merchandise sales have outstripped all other sources of revenue. The revenues from action figures sold by Kenner (1978-1985) and Hasbro (1995-2011) amounted to almost $10 billion (unadjusted for inflation) and adding in other merchandise, the collective revenues from toys and merchandise over the history of the franchise is in excess of $12 billion.

3. Gaming: As with the video rentals, the Star Wars games track shifting technologies, starting with an unlicensed game for the Apple II on a cassette tape, followed by table-top game by Kenner and games for the Atari. Starting in 1992, the games shifted away from the films to the expanded Star Wars universe, first with the X-wing computer games and later with Dark Forces, a shooter game. In 2013, Disney revealed that Electronic Arts would retain the rights to produce games for PCs and consoles, while Disney would retain the rights for other platforms. The collective revenues from all of these games between 1977 and 2015 is $3.4 billion.

4. Books: There have been almost 360 books, with 76 authors, in the Star Wars series and total sales have amounted to more than $1.8 billion. The staying power of the franchise is backed up by the fact that the first books were in print in 1978 and that there have been at least ten Star Wars novels a year, every year from 1991 to 2014.

5. TV Series/Other: Given its success on so many dimensions, it is surprising that the Star Wars franchise has not spawned a higher profile TV series. The longest lived TV series, Clone Wars, has had seven seasons and a second one, Star War Rebels, produced by Disney, has had two seasons. There have been periodic rumors about other TV series in the works, with the latest one suggesting that Netflix is planning three live-action series.

The collective revenues from these add-ons make the Star Wars revenue pie much larger than any competing movie franchise:

Note that the movie revenues in the table are not adjusted to 2015 $, since the revenues from the add-ons are not available in current dollars. In the table below, I scale the revenues from each of the add -ons to the box office receipts to get a measure of the value added from the rest of the Star Wars ecosystem:

In effect, for every dollar that Star Wars has made at the box office, it has generated four dollars in revenues from other sources. That number is a conservative estimate, since there have been undoubtedly others who have profited from the franchise unofficially (and illegally).

The New Series: Disney takes over

In 2012, Disney acquired the Star Wars franchise for $4 billion, from George Lucas, with plans to produce three more Star Wars movies. At the time of the acquisition, I argued that it was a fair price, given Disney's history with developing, maintaining and merchandising franchises, but had to draw on the potential for synergy to justify the number. With the release of Star Wars: The Force Awakens just about ten days ago, Disney seems to be more than delivering on its promise, as the movie has broken box office records and is on its way to delivering a global box office of $2 billion or more.

To the extent that this movie, like its predecessors, will generate add-on revenues, there will be substantially more money to be made over the next few years. The next two movies are scheduled for 2017 and 2019, and there will be three spin offs in the intermediate years, with less ambitious budgets. After 2020, Disney's plans are not specific, but if the appetite remains, there will be undoubtedly more movies in the pipeline. More importantly, the movies will not only create a new base of younger fans but augment the sales of merchandise, toys and games in the coming decade. The revenues that would have come from DVDs and video rentals will be replaced with streaming revenues and there will undoubtedly be games and apps directed at smartphones, devices and gaming systems.

To value the franchise, I started with my estimates of worldwide box office receipts for Star Wars: The Force Awakens and the subsequent movies in the series. Though, the first two weekends have blown away expectations (with the movie making $1 billion), I will estimate $2 billion in revenues, for each of the three main movies, and half those proceeds for the spin offs, with an inflation adjustment of 2%.

As with the prior movies, the bulk of the revenues from the franchise will come from add-ons, and in assessing the potential, here are some of my assumptions:

1. Streaming: As viewers increasingly turn to watching streamed movies from services (Netflix, Amazon Prime) on their televisions and devices, the revenues from streaming are quickly catching up with box office receipts for movies, and by 2017, the total revenues from streaming are expected to exceed box office revenues. I will assume that each dollar in box office revenues from the new Star Wars movies will generate $1.20 in additional revenue in streaming, slightly higher than historical numbers (1.14).

2. Toys/Merchandise: The Star Wars movies have historically generated $1.80 in revenues from toys/merchandise for every dollar in box office revenues. Given Disney's prowess at merchandising, I would not be surprised to see this number go up, and I will assume that each dollar at the box office will translate into two dollars in merchandising revenues, a little higher than the historical value of $1.80 per box office dollar. Keep in mind that this franchise is a merchandisers' dream, with an almost endless potential for new opportunities in the Expanded Universe.

3. Books and eBooks: This is the stream that is perhaps most at risk, and I will assume that while a way will be found to adapt the publishing stream to changing tastes in reading, the revenues from this books/e-books will drop to $0.20 per box office dollar (from $0.27, the historical number).

4. Gaming: In keeping with the history of Star War games, I am convinced that that games will be adapted not only to gaming platforms (Xbox, Playstation and Nintendo) but also to smartphones and tablets. I will leave the gaming revenues at $0.50 per dollar in box office receipts.

5. TV Shows/Other: This is the one add-on where I will assume a significant improvement over historical numbers, as Disney, Netflix and others find ways to adapt the franchise to television viewers. I will assume that the revenues from TV shows will increase to $0.50 per dollar in box office receipts.

To estimate the franchise value, I used the operating margins of the movie (20.14%) and toy/merchandise businesses (15%) and netted out taxes (at a 30% tax rate), before discounting back at a 7.61% cost of capital, the entertainment sector average. (Disney will probably license most of the merchandise, passing of the risk to others, but settling for a share of the operating income.) At least based on my projections, the value of the Star Wars franchise, if it can maintain my estimated numbers (for add-ons) and deliver at the box office, is almost $10 billion. The value is obviously a function of movie revenues and the add-on dollar values:

Not only does that make Disney's $4 billion investment three years ago a very good one, but any synergies that Disney can gain in its other businesses (like this one) will create more upside. As always, you are welcome to make your own assumptions and revalue the franchise, using this spreadsheet.

An Acquisition Model that works?

I am not a fan of acquisition-driven growth, primarily because the process so often leads to over paying for growth, but Disney may have found an acquisition model (albeit a limited one) that works with its Star Wars and Marvel acquisitions. In both cases, the company bought established movie franchises and has used its merchandising machine to generate value. Those results have already borne fruit with Marvel, especially with the Avenger movies, and we may be be seeing the beginnings of the Star Wars dividends this week.

During the week, while I was in the city (New York), I saw at least three Stormtroopers and a Darth Vader on Times Square and every store that I went into had something related to Star Wars, on sale. If you are a Star Wars purist, appalled by the shameless merchandising of the movie, I am afraid that you ain't seen nothing yet. If you are a Star Wars collector, and think that you have the entire collection already (for you or your kids), here is something for you to ponder. If you are a Disney stockholder like me, may the force be with you!

Attachments

1. Star Wars: Valuing the Franchise (Spreadsheet)

2. Star Wars: Franchise Value Picture (jpg file)

/cdn0.vox-cdn.com/uploads/chorus_asset/file/4294211/stock-apple-watch-music-0172.0.jpg)

/cdn0.vox-cdn.com/uploads/chorus_asset/file/3585726/new-apple-macbook-2015-_-_22.0.jpg)

Goldman Sachs

Goldman Sachs{kind=link}

{kind=link}