Weekly Market Update: China Fears Spoil the New Year

Global stock markets experienced one of the worst first trading weeks of the year ever, pummeled by China's ham-fisted attempts at stock market and currency reform. The S&P500 ended the first five days of 2016 down by 6%, while the DJIA erased 6.2% over the same period. Both the DJIA and the Nasdaq are now in correction, 10 percent off their 2015 highs. Weak Chinese data and the PBoC's attempts to shore up the economy by accelerating the devaluation of the yuan shuttered Chinese equity trading twice, creating panicked reactions in various global equity markets. Gold and government bond prices held up relatively well with investors turning away from risk assets, but oil prices continued to sink.

The selloff got underway on Monday after Chinese regulators implemented new circuit breaker rules for mainland equity markets, including a halt in trading for the day if the index fell 7%. That morning, the official China December manufacturing PMI dropped slightly to 49.7, marking its fifth month in contraction, while the unofficial Caixin manufacturing PMI dropped to 48.2, for its tenth month in contraction. The data gave traders the excuse they needed to test the new rules, and the Shanghai Composite was halted after dropping by 7% in afternoon trading. Shanghai appeared to stabilize somewhat on Tuesday and Wednesday, then on Thursday it only took 29 minutes after the open of cash equity trading for the Shanghai index to tank 7% and trigger the circuit breaker. The yuan fixing was blamed for Thursday's slide.

For eight straight sessions through Thursday, the PBoC weakened its yuan reference rate, dropping it to 6.5646 on Thursday, the weakest rate against the dollar since March 2011. Thursday's fix was significantly weaker, -0.5% from the prior day, the biggest margin of decline since the August devaluation. The move prompted concerns that the central bank's continued efforts to weaken the yuan will spur massive investment outflows from the mainland. The PBoC set the rate a bit higher on Friday. There were unconfirmed reports that the PBoC heavily intervened in markets throughout the week in an attempt to control the declines in the yuan. China's defense of the yuan had managed to stabilize the currency for almost four months following the notorious August devaluation, although the effort led to the first-ever annual decline in the nation's FX reserves, seen in data out on Thursday.

Traders dumped emerging market currencies while factoring the ramifications of a weaker yuan. The Mexican Peso and South Africa Rand hit fresh lifetime lows against the dollar. The Turkish Lira hit a three-month low and the Brazilian Real gained a foothold above four to the USD while its close ties to the Chinese economy were scrutinized. With oil trading in the low $30's and copper testing 2.00/lb., other commodity-backed economies saw their currencies fare very poorly as well. USD/CAD broke out above the 1.40 mark reaching levels not seen in more than a decade. The Aussie Dollar fell roughly 3 big figures against the Greenback to trade below 0.70 for the first time since early October.

Relations between Saudi Arabia and Iran reached an all-time low after the Saudis executed 47 militants, including Nimr al-Nimr, a Shiite cleric and activist on behalf of the Shiite minority. Protests erupted in Iran and throughout the Shiite world. In Tehran, a mob burned down the Saudi embassy, leading Riyadh (and many of its Gulf allies) to cut diplomatic ties with Iran. With crude at more than a decade low, the Saudi budget deficit hit an unprecedented 15% of GDP, forcing the government to dip heavily into its reserves. In response, the Saudis said they might attempt to IPO the state oil company, Saudi Aramco. Analysts suggest that even if the Saudis sell a small stake, the listing could easily surpass that of Alibaba, whose $25 billion IPO is the largest on record. Aramco could be worth anything from $1 trillion to upwards of $10 trillion, which would make it the most valuable company in the world by a long shot.

WTI and Brent marched in lockstep from around $38 to test towards $32 on Thursday afternoon. There was a brief move higher on Monday due to the Saudi/Iran dustup, however the Gulf tension was no match for global market turmoil. Traders ignored big drawdowns in the DoE and API crude inventory reports, as well. After fears about China and emerging market growth, the strong dollar appeared to be the other major catalyst holding down oil prices. The greenback at its weakest remained above the low levels seen in November and early December, however EUR/USD lunged back below 1.0750 early in the week, marking one-month lows.

The US December jobs report was surprisingly strong, capping off a good year of employment growth. Non-farm payrolls far exceeded expectations, rising by 292K versus 200Ke. The blowout in the ADP report earlier in the week had hinted at a good showing on Friday. Unemployment remains at 5%. Wages were the only sour note in the report: average hourly earnings were flat in December compared to the prior month and rose 2.5% against the prior year. Both numbers missed expectations.

Automakers reported total industry sales of nearly 17.5 million for 2015, for the industry's best sales year ever. Fiat and Ford reported December US sales results that fell a bit short of expectations, while GM's December sales met consensus estimates. Fiat and Ford also reported that total 2015 sales were the best they'd seen in a decade. US-traded ADRs of Volkswagen sank sharply after the US government filed a lawsuit seeking penalties as high as $80 billion - more than the company is worth - and faulted the German carmaker for a lack of progress fixing cars with rigged engines.

Shares of Apple were under pressure this week after press reports warned that the company was expected to reduce the output of its iPhone 6s and 6s Plus devices by about 30% between January and March. Apple was said to be cutting back production in order to allow iPhone dealers to work their way through inventories that have piled up at retailers in markets ranging from China and Japan to Europe and the US amid lackluster sales. Several prominent firms cut price targets and ratings on Apple in the wake of the reports. Then on Thursday, Apple component suppliers Cirrus Logic and Qorvo cut their forecasts for the current quarter.

In other tech news, the Consumer Electronics Show in Las Vegas took place this week, with the usual assortment of flashy tech baubles on display. Smartwatches got the main billing, with investors frowning on the new FitBit Blaze watch. Amazon also got a great deal of attention for entering the semiconductor business and selling its own branded chips to other companies.

In merger news, the big story was Shire getting very close to success in its long-running pursuit of Baxalta. Back in August, Shire had proposed an all-stock deal at around $45/share for Baxalta, valuing it around $30 billion. Baxalta chose not to even enter negotiations back then, but this time around an offer as high as $48/share with a cash component up to 40% of the deal appears to have gotten their attention. ON Semiconductor got a new competitor in its pursuit of Fairchild Semiconductor. China Resources Microelectronics Limited offered $21.70/share, above ON Semi's $20/share bid, and Fairchild's board determined it to be a superior offer.

Closing Market Summary: The Stock Market Ends Week Sharply Lower

The major indices ended their day under heavy selling pressure as the market was rebuffed on its muted rebound effort. Sliding oil prices, global growth concerns, and the future path of the federal funds rate remained in focus as investors appeared less than willing to buy into current market conditions. The S&P 500 (-1.1%) ended its session behind both the Dow Jones Industrial Average (-1.0%) and the tech-heavy Nasdaq (-1.0%). Including today's trade, the benchmark index has surrendered 6.0% to begin the year whereas the Nasdaq has tumbled 7.3%.

Overseas action was hallmarked by restrained trading ahead of the U.S. Employment Situation Report. Futures jumped to pre-market highs following the announcement that nonfarm payrolls increased by 292k (Briefing.com consensus 200,000), but this would prove short-lived, as the rest of the report was digested by the market. Issues regarding flat wage growth (Briefing.com consensus 0.2%) and a static 9.9% U6 unemployment rate (which accounts for the unemployed, underemployed, and marginally attached workers) dulled the effects of the initial positive number.

The major averages gapped up to begin their day but were unable to find support at those prices levels. The market retreated from its early high alongside a drop in oil prices. Stocks were able to find some traction near mid-morning lows which resulted in a rally into positive territory. This rally matched a similar move in crude, but the commodity was no better at holding those price levels as the markets was at holding its advance. WTI crude ended its pit session down 0.3% at $33.16/bbl. For the week, the energy component surrendered 10.0%.

On the leaderboard, financials (-1.6%), health care (-1.4%), energy (-1.3%), and consumer discretionary (-1.1%) rounded out the sectors while utilities (UNCH), telecom services (-0.5%), consumer staples (-0.8%), and technology (-0.8%) lead the pack.

The health care space was the only countercyclical sector that could not finish near the top of the leaderboard. In the sector, biotechnology showed relative weakness, with the industry group finishing behind the the broader sector. This was evidenced by the iShare Nasdaq Biotechnology ETF (IBB 302.20, -5.58) closing out its session lower by 1.8%. Elsewhere in the space, sector large-cap AbbVie (ABBV 55.65, -1.56) underperformed with a decline of 2.7%.

In the technology space, investors sought out the large-cap names Apple (AAPL 96.96, +0.51), Facebook (FB 97.33, -0.59), and Microsoft (MSFT 52.33, +0.16). The three were some of the top-performers in the sector with respective performances of +0.5%, -0.6%, and +0.3%. Elsewhere, the high-beta chip makers struggled, evidenced by the PHLX Semiconductor Index sliding 1.6%.

In Treasuries, the benchmark note ended its day on its high with the 10-yr yield falling four basis points to 2.11%.

Investor participation was well above average with more than a billion shares trading hands at the NYSE floor.

Economic data included Nonfarm Payrolls for December, whole sale inventories for November, and the Consumer Credit Report for November.

- December nonfarm payrolls increased by 292,000 (consensus 200,000)

- November nonfarm payrolls were revised to 252,000 from 211,000

- October nonfarm payrolls were revised to 307,000 from 298,000

- Private sector payrolls increased by 275,000 (consensus 194,000)

- November private sector payrolls were revised to 240,000 from 197,000

- October private sector payrolls were revised to 312,000 from 304,000

- The Unemployment rate was 5.0% (consensus 5.0%) versus 5.0% in November

- The U6 unemployment rate, which accounts for the total unemployed plus persons marginally attached to the labor force and the underemployed, was unchanged at 9.9%

- Average hourly earnings were flat (consensus 0.2%) after increasing 0.2% in November

- The average workweek was 34.5 hours (consensus 34.5) versus 34.5 hours in November

- The labor force participation rate was 62.6% versus 62.5% in November

- November Wholesale Inventories fell 0.3% while the consensus expected a decreased of 0.1%

- Today's report followed last month's revised decrease of 0.3% (from -0.1%).

- The inventories/sales ratio increased to 1.32 from 1.31 in October.

- November consumer credit showed an increased of $13.95 billion (consensus $18.50 billion)

- Prior months growth was revised down to $15.61 billion from $15.98 billion.

Investors will not receive any economic data of note on Monday.

- Russell 2000 -7.8% YTD

- Nasdaq -7.3% YTD

- Dow Jones Industrial Average -6.2% YTD

- S&P 500 -6.0% YTD

Fed's Williams (moderate, FOMC non-voter in 2016): Economy still needs support from Fed but not as much as previously

- Unemployment rate likely at 4.5% by the middle of 2015

- Overtime Fed Funds rate seen at 3-3.5%

- there are still downside risks to the economy including the USD strength and spillover from overseas; upsides to economy include housing

wenty-First Century Fox Inc (NASDAQ: FOXA) is still interested in Time Warner Inc (NYSE: TWX). A source familiar with the matter told Benzinga on Friday morning that Fox has made a new offer for Time Warner, this time at a price of $105 per share.

The source said the deal could happen as soon as next week. Time Warner shares closed Thursday's session at $70.20; The stock has been volatile on Friday amid a report from the New York Post that Time Warner shareholders could force a sale or spinoff HBO.

Gabelli & Co. analyst Brett Harriss told Benzinga Friday morning that this elevated price makes prospects of a takeover "seem unlikely."

Two other Wall Street analysts, who both asked to remain anonymous, told Benzinga this takeover makes sense.

Benzinga has reached out to Time Warner and Fox and has yet to receive a response.

Previous Offer

Fox had previously shown interested in Time Warner back in the summer of 2014. At that time, Fox bid $84 per share for the media company. The potential deal was called off in August of that year.

Media mogul and Fox CEO Rupert Murdoch at the time said, "Our proposal had significant strategic merit and compelling financial rationale and our approach had always been friendly. However, Time Warner management and its board refused to engage with us to explore an offer which was highly compelling."

Murdoch cited Fox's share price, saying it had become undervalued, making the deal "unattractive to Fox shareholders."

Previous Comments

Back in November 2015, Harriss wrote in a note that Fox "could return to re-bid" for Time Warner. Among other reasons, the firm said "Fox Warner" could eclipse Walt Disney Co (NYSE: DIS) as the dominant U.S. media company.

"We expect traditional operating synergies would be material in a combination," the firm wrote. "Fox estimated $1 billion of operating synergies as part of its 2014 offer which we expect to be conservative." Additionally, the combined sports right of the two companies would challenge ESPN, according to the firm.

Gabelli also said a combined entity would scale greatly on the international front, and that both would be better positioning to build a wholly-owned over-the-top (OTT) product.

Also last November, Morgan Stanley cited the rising U.S. dollar and the "fraying of the pay-TV bundle that rives the majority of Time Warner's economics" as two emerging headwinds for Time Warner.

Saudi Aramco I.P.O. Is Weighed by Kingdom

There are big initial public offerings — the $25 billion stock sale by the Alibaba Group, the biggest on record; the $16 billion market debut of Facebook — and then there are really big ones.

If Saudi Arabia follows through on its plan to list its state-owned oil producer, Saudi Aramco, as one of the kingdom’s top officials recently told The Economist, it would certainly claim the latter.

“This is something that is being reviewed, and we believe a decision will be made over the next few months,” Prince Mohammed bin Salman, Saudi Arabia’s deputy crown prince and one of its most powerful figures, told the publication. “Personally I’m enthusiastic about this step. I believe it is in the interest of the Saudi market, and it is in the interest of Aramco, and it is for the interest of more transparency, and to counter corruption, if any, that may be circling around Aramco.”

On Friday, Saudi Aramco released a statement confirming that it the company has been studying options to offer the public an unspecified, “appropriate percentage” of its shares or some of Saudi Aramco’s subsidiaries.

Consider that Exxon Mobil, the world’s biggest publicly traded oil producer, is valued at just over $320 billion. It’s not hard to believe that Saudi Aramco would be valued at huge multiples of its American counterpart.

In the interview with The Economist, Prince Mohammad agreed with the implication that an I.P.O. would be tantamount to a “Thatcher revolution” for Saudi Arabia, referring to the 1980s privatization of a number of Britain’s government enterprises under Prime Minister Margaret Thatcher.

Just how much Saudi Aramco’s market value would be is up for debate, of course. The Financial Times estimated in 2010 that the oil producer was worth $7 trillion, or approximately 12 Apples now. But The Financial Times’s Alphaville acknowledged in a post on Thursday that the estimate was born of heady times for state-owned energy producers that had gone public — companies whose earnings multiples have since tumbled.

Saudi Aramco could be different, of course. It has unparalleled cheap access to the ocean of petroleum that floats beneath Saudi Arabia’s sands.

The kingdom could have fetched an even higher valuation for its crown jewel before oil began plunging in price. (Brent crude closed on Thursday just above $33 a barrel.)

The kingdom would virtually certainly refuse to cede any control over the company if it is listed on a public exchange, which The Economist said would most likely be the Tadawul in Riyadh. While some companies with concentrated ownership have taken a hit on valuation, the biggest such market debutantes, like Alibaba and Facebook, have escaped such a fate.

Discussions about Saudi Aramco’s fate appear to be at an early stage. The Economist reports that Prince Mohammad has held two “high-level meetings” to discuss a potential stock sale. And discussions about how such a stock sale would look — whether it would be for some of the producer’s constituent businesses or for its parent company — are still going on.

At the least, the world’s biggest banks are undoubtedly salivating at the chance to work on such a big I.P.O., as much to claim credit for a prestigious assignment as it would be for the fees.

The company has relationships with many a major bank. Just look at the $10 billion in debt that Saudi Aramco secured last year: Deutsche Bank, JPMorgan Chase and Citigroup were among the underwriters.

Surely all of them, and Wall Street’s other top institutions, would compete hard to gain an I.P.O. mandate.

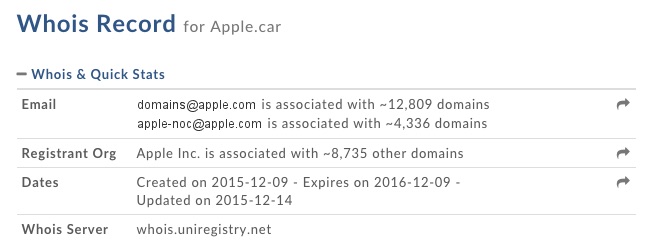

Apple has registered a trio of auto-related top-level domain names, including apple.car,apple.cars and apple.auto. Whois records updated on January 8 show that Apple registered the domains through sponsoring registrar MarkMonitor Inc. in December 2015, although they are not yet active.

The domains could be related to CarPlay, but there will naturally be speculation about their possible relation to Apple's much-rumored electric vehicle plans. Multiple reports over the past year said Apple has a secretive team of hundreds working on an electric vehicle with a prospective 2019 or 2020 shipping date.

There is increasing evidence that Apple is at least exploring the auto industry, including the iPhone maker's discussions with a secure Bay Area testing facility for connected and autonomous vehicles and the company's August meeting with the California DMV to review self-driving vehicle regulations.

Apple has aggressively recruited engineers and other talent from Tesla, Ford, GM,Samsung, A123 Systems, Nvidia and elsewhere to work on the rumored "Apple Car" project, which has allegedly been called "Project Titan" internally. Electric motorcycle startup Mission Motors even ceased operations after losing employees to Apple.

Apple likely remains in the earlier stages of research and development of its rumored electric vehicle, and it remains possible the company's plans change over the next three to four years. Nevertheless, the trio of new domains provide yet another clue that Apple may one day compete with the likes of Tesla and Google.

The domains could be related to CarPlay, but there will naturally be speculation about their possible relation to Apple's much-rumored electric vehicle plans. Multiple reports over the past year said Apple has a secretive team of hundreds working on an electric vehicle with a prospective 2019 or 2020 shipping date.

There is increasing evidence that Apple is at least exploring the auto industry, including the iPhone maker's discussions with a secure Bay Area testing facility for connected and autonomous vehicles and the company's August meeting with the California DMV to review self-driving vehicle regulations.

Apple has aggressively recruited engineers and other talent from Tesla, Ford, GM,Samsung, A123 Systems, Nvidia and elsewhere to work on the rumored "Apple Car" project, which has allegedly been called "Project Titan" internally. Electric motorcycle startup Mission Motors even ceased operations after losing employees to Apple.

Apple likely remains in the earlier stages of research and development of its rumored electric vehicle, and it remains possible the company's plans change over the next three to four years. Nevertheless, the trio of new domains provide yet another clue that Apple may one day compete with the likes of Tesla and Google.

Hearing vague takeover chatter circulating - Fox rumored as a potential acquirer

Gemalto starting to move

From: LAURENT CHEKROUN (MAKOR SECURITIES LO) At: Jan 8 2016 15:41:07

Subject: Fwd:>>> Microsoft’s latest attempt to get noticed in the mobile space can spell good

Microsoft’s latest attempt to get noticed in the mobile space can spell goodbye to long term network contractsMicrosoft Corporation (NASDAQ:MSFT) has long lurked in the shadows of Apple Inc. (NASDAQ:AAPL) and Google Inc. (NASDAQ:GOOG) in the smartphone industry. However, it appears the company is ready do give its all in a bid to get noticed. We take a look at recent reports which claim that the company is now planning to adopt a strategy which revolves around the manufacture of its own specially designed SIM cards.Ever since the company struck a deal with Finnish company, Nokia Inc. (NYSE:NOK), its smartphone business has fallen to depths not many had expected. With the partnership now over and the company pursuing a change in policy by pushing forth its own manufactured smartphones, Microsoft might be heading toward a new era of mobile devices.The company recently launched its Lumia 950 and Lumia 950XL, two flagship devices which feature specs that could compete with any existing smartphone in the industry. While the company might be falling short with its Windows Phone platform, it is hoping to attract users towards its devices via a new strategy, one that involves SIM cards.According to reports, Microsoft is currently testing a cellular data application which will allow Windows 10 running devices, including smartphones, tablets and other devices, to connect to different mobile networks without a contract. Such a move requires the company to manufacture its own SIM cards, something that will make access to LTE far easier for users.Although the application has been published on Microsoft’s Windows Store, the company is yet to confirm its plans regarding the service. The application can’t be downloaded by users just yet, but we have enough clues to figure out what to expect from it.The application which is listed down as Free is called, “Cellular Data” and is only compatible on Windows 10 running devices that make use of a “Microsoft SIM Card”. According to details, we believe Microsoft is planning to create its own virtual mobile network which will allow users to connect to partner carrier networks.For now, we are unsure of which partners will be on board with the new service, something Microsoft will need to focus on if it expects it to be a telling feature, to attract users towards its Windows 10 Mobile.According to reports, the application will allow users to stay connected wherever they go. Having access to Cellular Data courtesy of your Microsoft Account is quite a tempting proposition. The best feature about the service is that users will be able to pay for data using only their Microsoft account information, i.e. they will no longer have to rely on long term commitments to mobile networks.Its not known yet which markets are likely to get access to the service when it launches. However, many believe the company will only initiate International Roaming after gauging its success in the domestic market. Although Microsoft has confirmed that payment would be done via users' accounts, pricing details of the service are yet to be released.By the looks of things, Microsoft is focusing on the hardware aspects when it comes to its smartphone business. While the manufacture of SIM Cards and provision of widespread access to Cellular Data will please many, the company needs to relay some focus onto its currently buggy Windows 10 Mobile.