Citadel Is Handing Back About $7 Billion in Profits to Clients

Ken Griffin’s hedge-fund firm performed better than peers in 2023 with a nearly 15% return for its flagship fund

Citadel is planning to give its investors about $7 billion in profits it earned in a year when choppy stock markets and interest rates challenged most hedge-fund managers, people familiar with the firm said.

The flagship multistrategy fund at Ken Griffin’s Miami-based firm returned nearly 15% in the first 11 months of 2023, the people said. The fund, Wellington, gives investors exposure to stocks, bonds, commodities and other asset classes and returned 38% in 2022.

After handing back capital in the coming weeks, Citadel expects to start 2024 with about $58 billion in assets under management, the people said.

Many other hedge funds, including ones run by high-profile managers such as Dan Loeb and Jim Chanos, have struggled in a year that included a shifting outlook for inflation and job growth, a regional banking crisis and a run-up in the shares of big tech companies.

The average gain for hedge funds in the year through November was 4.35%, according to a fund-weighted index compiled by research firm HFR. The S&P 500 rose 20.8% including dividends in the year through November.

Citadel has long been one of the industry’s top performers, delivering more gains, net of fees, to clients since inception than any other hedge-fund firm, according to LCH Investments.

Unlike a classic hedge fund where analysts funnel investment ideas to a single decision maker, Citadel employs dozens of teams to trade independently in markets around the world within a set of risk parameters.

So-called multimanager platforms such as Citadel have emerged in recent years as the new center of gravity in the hedge-fund industry. The platforms have hired aggressively and bid up the price of investment professionals. Many portfolio managers who would have struck out on their own in an earlier era are now opting to accept lucrative offers to join a platform.

Investors in hedge funds like the model because it is centered on steady production—not on swinging for the fences. The funds typically balance bets that some stocks will rise with bets that others will fall. That model can also reduce overall exposure to rising stocks, weighing on performance when markets are rallying, like this year.

A Barclays index of 42 multimanager platforms posted annualized returns of 8.1% over the last five years, 2 percentage points better than the rest of the industry.

Citadel and other large hedge-fund firms regularly hand back profits to clients to prevent their funds from growing larger than managers feel they can invest. Since 2018, Citadel has returned about $25 billion in profits to investors, the people said.

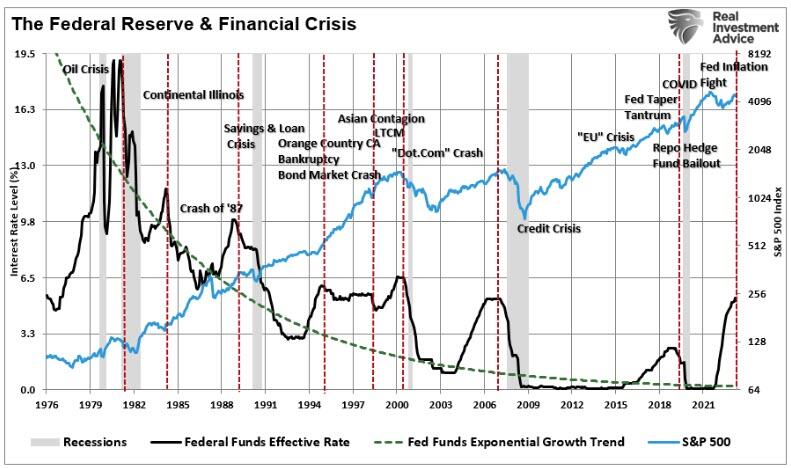

The Markets Are Front-Running The First Rate-Cut

In October, the markets were down 10% from the July high, bond yields were touching 5%, and talk of a coming recession was rampant. What happened?

Interestingly, a Wall Street axiom says, “Sell the last Fed rate hike.” The reason is that when the Fed starts cutting rates, it is due to the onset of a recession, a bear market, or a financial event. At that point, as shown below, the markets are repricing for lower expectations of earnings growth rates and profitability.

As Michael Lebowitz noted previously in “Federal Reserve Pivots Are Not Bullish:”

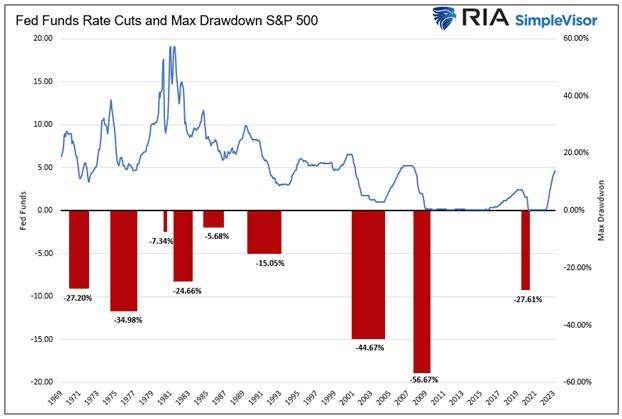

“Since 1970, there have been nine instances in which the Fed significantly cut the Fed Funds rate. The average maximum drawdown from the start of each rate reduction period to the market trough was 27.25%.The three most recent episodes saw larger-than-average drawdowns. Of the six other experiences, only one, 1974-1977, saw a drawdown worse than the average.”

Given that historical perspective, it certainly seems apparent that investors should NOT be anticipating a Fed rate-cutting cycle. Such should, in theory, coincide with the Fed working to counter a deflationary economic cycle or financial event.

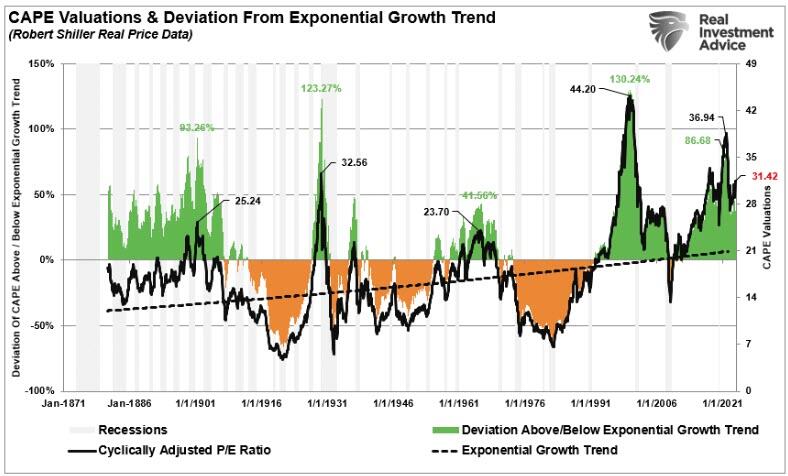

Yet, since the beginning of November, the markets have risen sharply in anticipation of the Fed cutting rates as soon as the first quarter of 2024. More interestingly, the worse the economic data is, the more bullish investors have become looking for that policy reversal. Of course, in reality, weaker economic growth and lower inflation, which would coincide with a rate-cutting cycle, do not support currently optimistic earnings estimates or valuations that remain well deviated above long-term trends.

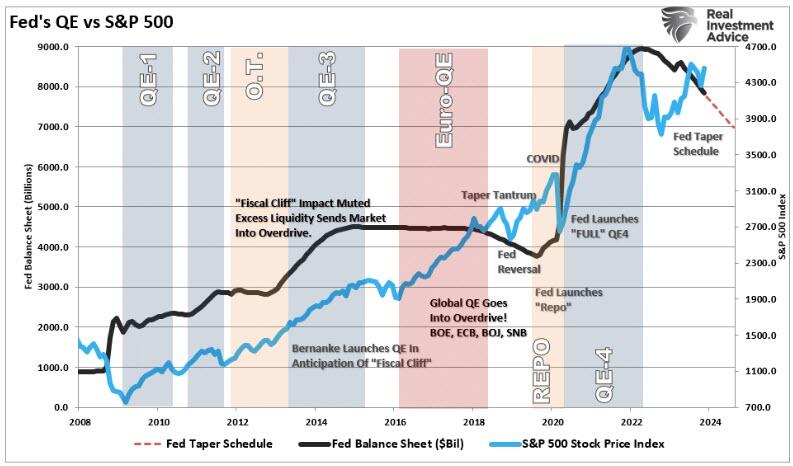

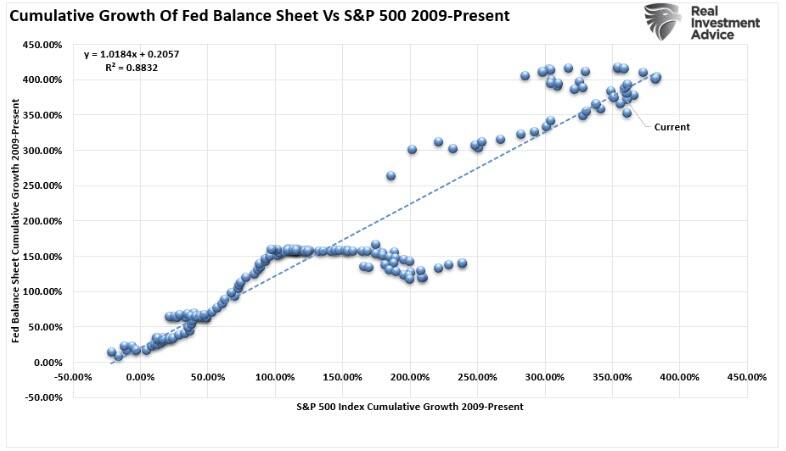

Of course, that deviation of valuations has been the direct result of more than $43 Trillion in monetary interventions since 2008, which has trained investors to ignore the fundamental factors.

Has Pavlov’s Experiment Trained Investors

Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a potent stimulus (e.g.,food) is paired with a previously neutral stimulus (e.g., a bell). Pavlov discovered that when the neutral stimulus was introduced, the dogs would begin to salivate in anticipation of the potent stimulus, even though it was not currently present. This learning process results from the psychological “pairing” of the stimuli.

In 2010, then Fed Chairman Ben Bernanke introduced the “neutral stimulus” to the financial markets by adding a “third mandate” to the Fed’s responsibilities – the creation of the “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate this additional action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”– Ben Bernanke, Washington Post Op-Ed, November, 2010.

Importantly, for conditioning to work, the “neutral stimulus,” when introduced, must be followed by the “potent stimulus” for the “pairing” to be completed. For investors, as each round of “Quantitative Easing” was introduced, the “neutral stimulus,” the stock market rose, the “potent stimulus.”

While there has been previous debate on the impact of the Fed’s balance sheet changes on the markets, there is a very high correlation between the two, suggesting it is more than just a coincidence.

Notably, before 2008, there was clear evidence that markets repriced lower when the Fed began a rate-cutting cycle. Such was because the realization of a financial event created selling pressure in the market. Stocks historically fell until that rate-cutting cycle was over and the catalyzing event was resolved.

However, since 2008, the Fed has trained investors. Any financial or recessionary event jeopardizing the markets would be met with rate cuts and accommodative policy. That training was completed with the Fed’s response to the “pandemic-era shutdown” that led to massive monetary and fiscal interventions.

There is currently a large contingent of investors who have never seen an actual “bear market.” For many investors in the markets today, their entire investing experience consists of continual interventions by the Federal Reserve. Therefore, it is unsurprising investors are fully trained to “fear of missing out” on the next round of Fed support.

Are Investors Front-Running The Fed?

We have previously discussed the many economic indicators suggesting a recession is possible. However, one has yet to manifest itself, and economic growth has continued to defy tight monetary policy. Subsequently, investors have now concluded that a recession will be avoided, the Fed will cut rates, and stocks will rise.

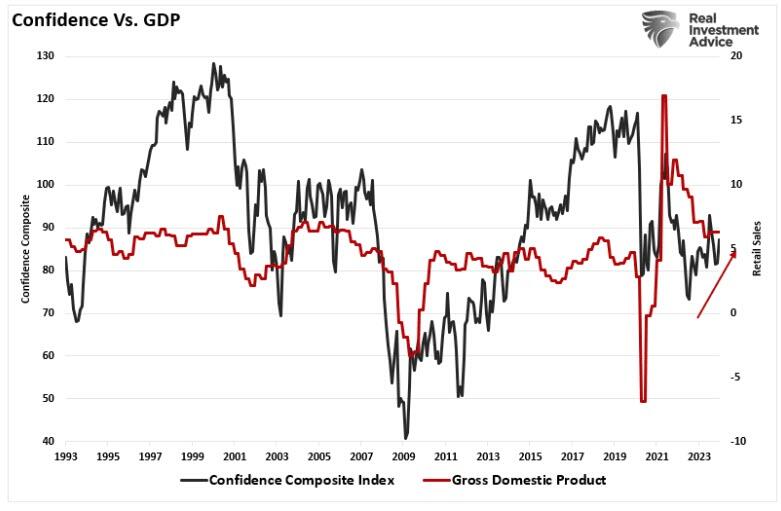

The market’s increase since November has the knock-off effect of boosting consumer confidence. As noted in Ben Bernanke’s quote, the result should be increased economic activity to keep the economy out of recession. The chart below is the consumer confidence composite index as compared to GDP.

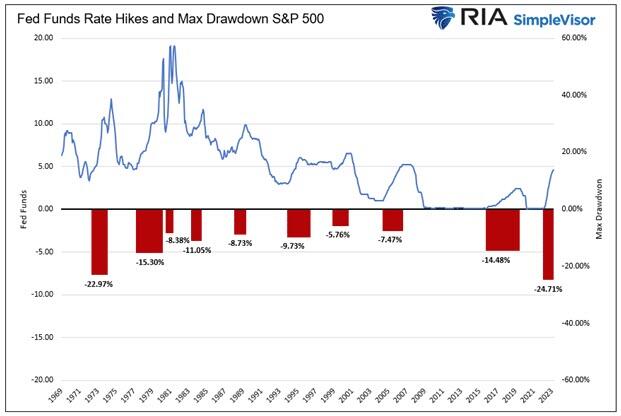

Note the increase in consumer confidence since the lows of October 2022. The question becomes, has the expected market decline from a Fed rate hiking cycle already completed? In the linked article above, Michael Lebowitz tackled that question. He used a Wicksellian model to estimate the expected percentage drawdown during a Fed rate hiking cycle. To wit:

“The graph below shows the maximum drawdown from the beginning of rate hiking cycles. The average drawdown during rate hiking cycles is 11.50%. The S&P 500 experienced a nearly 25% drawdown during the current cycle.”

That estimate of a 24% drawdown was not far off the market’s 20% nominal drawdown in 2022. This poses an interesting question to investors who are currently expecting a further drawdown in 2024.

“Since the market experienced a decent drawdown during the rate hike cycle starting in March 2022, might a good chunk of the rate drawdown associated with a rate cut have already occurred?“

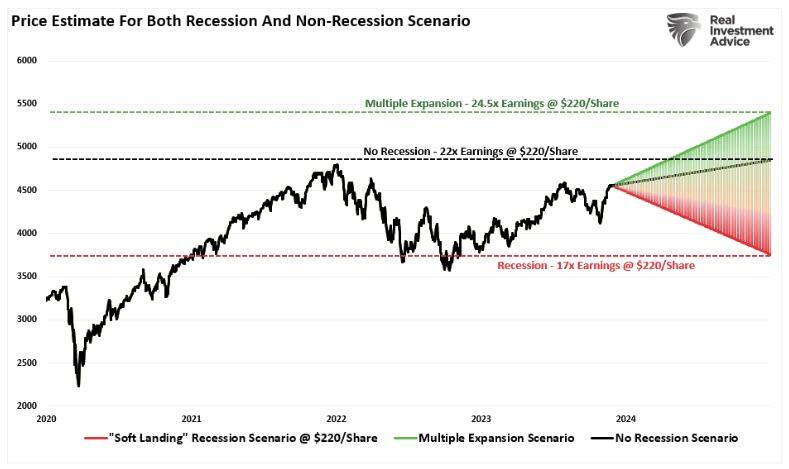

A Range Of Possibilities

Let me clearly state that I do NOT have a crystal ball for 2024. Even my “Crazy Eight Ball” replied with “outlook uncertain.”

However, there are three primary possibilities for the markets we must consider.

- The Fed cuts rates and navigates a soft landing, stabilizing earnings growth, and the markets price higher on easier monetary policy and reversing “Quantitative Tightening” or “QT.”

- Due to increased asset prices and consumer confidence, economic activity picks up, and the Fed remains on hold over concerns about a resurgence of inflationary pressures. The markets reprice modestly to accommodate for a drag on economic growth, but recession fears are dismissed.

- A financial event and a recession occur due to the current restrictive level of monetary policy, and even though the Fed drastically cuts rates and reverses QT, stocks reprice lower due to a drop in earnings growth.

These possibilities are the drivers behind the range of potential outcomes discussed last week.

Using history as a guide, the many voices suggesting more bearish outcomes for 2024 seem logical. However, we must consider the impact of the Fed’s decade-long training of investors to “buy monetary policy changes.”

It may not make logical or fundamental sense. However, we must remain open to the possibility that markets are front-running the eventual Fed’s “ringing of the bell.”

EU outlines plan to avert shortages of more than 260 critical medicines

Proposals include measures to encourage stockpiling and investment incentives for new factories in bloc

Vital drugs such as paracetamol and morphine need to be stockpiled or made in the EU to prevent shortages, according to a list of critical medicines for the bloc.

The list, published by the European Medicines Agency on Tuesday, includes more than 260 treatments including vaccines, painkillers and asthma medicines. The EU promised to have a plan to improve the supply of these medicines by April after several countries reported shortages last winter.

The proposals could include measures to encourage companies to stockpile products and diversify suppliers, investment incentives for new manufacturing plants in the EU and the introduction of joint procurement protocols as the bloc did with Covid-19 vaccines, according to a European Commission proposal in October.

Europe is heavily reliant on China and India as a source of drugs and the vital precursor chemicals needed to make them. As part of the EU’s drive for “strategic autonomy”, it is drawing up a plan to make more domestically.

France has vowed to reshore the production of 50 key medicines and is opening a new paracetamol plant next year. The last EU facility shut in 2008.

The European Medicines Agency, together with the Health Emergency Preparedness and Response Authority will publish a longer list of critical medicines which will identify those at risk of experiencing shortages.

“Together we will then identify the best measures to address and avoid shortages, from diversification and de-risking to increase manufacturing in Europe,” commission president Ursula von der Leyen said last week.

The list includes Salbutamol, a muscle relaxer used in asthma inhalers, insulin for diabetes treatment, warfarin, which prevents blood clots, and several types of penicillin and other antibiotics including erythromycin. Vaccines listed include jabs for meningitis, measles, mumps, rubella, influenza and tetanus.

Anaesthetics and painkillers such as lidocaine, morphine and fentanyl and commonly used drugs such as oxytocin are also on the EU’s critical list.

Health commissioner Stella Kyriakides is pushing the plan after lobbying from health ministers following last winter’s shortages. Painkillers for children were among those affected.

Adrian van den Hoven, director-general of generic drugmakers association Medicines for Europe, said the body “strongly supports” the move to improve Europe’s medicine supply security in the post-pandemic era. “The list of critical medicines is an important first step, by harmonising the wide variety of diverging national lists across the region,” he said.

However, he warned that health systems and consumers might face higher prices. “Many of the medicines on this list are subject to the most extreme forms of cost-containment in EU member states, which exacerbates the risk of shortages.”

Van den Hoven advocated the harmonisation of medical packaging rules so that drugs could be more easily transferred from one country to another.

Didier Reynders, the acting competition commissioner, told the European Health Summit in Brussels last week that he was open to permitting subsidies for new manufacturing facilities.

“We are open to assess the possibility of giving state aid for new manufacturers. It is more sensitive because of the distortion of competition,” he said. “But it is possible.”

Member states could pitch a pan-EU project as a “service of general economic interest” where “we have a shortage on the market”, he said, adding: “We need supply chains in Europe and not be dependent on third countries.”

Research Calls

-

Upgrades:

- 10x Genomics (TXG) upgraded to Neutral from Underperform at BofA Securities; tgt raised to $54

- Albemarle (ALB) upgraded to Neutral from Underperform at BofA Securities; tgt lowered to $149

- Amalgamated Bank (AMAL) upgraded to Overweight from Neutral at JP Morgan; tgt $29

- Amgen (AMGN) upgraded to Outperform from Sector Perform at RBC Capital Mkts; tgt raised to $300

- BlackRock (BLK) upgraded to Outperform from Neutral at Exane BNP Paribas; tgt $885

- BRP Group (BRP) upgraded to Strong Buy from Outperform at Raymond James; tgt $30

- Eagle Materials (EXP) upgraded to Neutral from Underweight at JP Morgan; tgt $200

- EverQuote (EVER) upgraded to Outperform from Mkt Perform at Raymond James; tgt $13

- Extra Space Storage (EXR) upgraded to Overweight from Underweight at Wells Fargo; tgt raised to $155

- Henry Schein (HSIC) upgraded to Overweight from Neutral at JP Morgan; tgt raised to $82

- Humana (HUM) upgraded to Buy from Hold at Argus; tgt $550

- HP Inc. (HPQ) upgraded to Overweight from Equal-Weight at Morgan Stanley; tgt raised to $35

- HubSpot (HUBS) upgraded to Overweight from Neutral at Piper Sandler; tgt raised to $610

- Itron (ITRI) upgraded to Neutral from Underweight at JP Morgan; tgt $68

- Manulife Financial (MFC) upgraded to Outperform from Sector Perform at RBC Capital Mkts

- Martin Marietta (MLM) upgraded to Overweight from Neutral at JP Morgan; tgt raised to $530

- Maravai Life Sciences (MRVI) upgraded to Buy from Neutral at BofA Securities; tgt lowered to $8

- NIKE (NKE) upgraded to Buy from Hold at DZ Bank; tgt $130

- PVH (PVH) upgraded to Buy from Neutral at Goldman; tgt raised to $126

- Quest Diagnostics (DGX) upgraded to Buy from Neutral at BofA Securities; tgt raised to $160

- Ralph Lauren (RL) upgraded to Neutral from Sell at Goldman; tgt raised to $132

- Sempra Energy (SRE) upgraded to Overweight from Neutral at JP Morgan; tgt raised to $86

- Sonos (SONO) upgraded to Overweight from Equal-Weight at Morgan Stanley; tgt raised to $20

- Sprouts Farmers Market (SFM) upgraded to Buy from Sell at Goldman; tgt raised to $49

- Vulcan Materials (VMC) upgraded to Overweight from Neutral at JP Morgan; tgt raised to $245

- Zillow (ZG) upgraded to Mkt Outperform from Mkt Perform at JMP Securities; tgt $60

- Zscaler (ZS) upgraded to Outperform from Neutral at Macquarie; tgt raised to $231

-

Downgrades:

- Agilent (A) downgraded to Neutral from Buy at BofA Securities; tgt raised to $133

- Airbnb (ABNB) downgraded to Underweight from Equal Weight at Barclays; tgt lowered to $100

- AMC Networks (AMCX) downgraded to Neutral from Buy at Seaport Research Partners

- Arthur J. Gallagher (AJG) downgraded to Mkt Perform from Strong Buy at Raymond James

- CDW (CDW) downgraded to Equal-Weight from Overweight at Morgan Stanley; tgt $216

- Comerica (CMA) downgraded to Neutral from Overweight at JP Morgan; tgt $57

- Expedia Group (EXPE) downgraded to Equal Weight from Overweight at Barclays; tgt raised to $150

- Fortis (FTS) downgraded to Underweight from Neutral at JP Morgan

- GOL Linhas Aereas Inteligentes S.A. (GOL) downgraded to Sell from Hold at Deutsche Bank

- GoPro (GPRO) downgraded to Underweight from Equal-Weight at Morgan Stanley; tgt lowered to $3

- Grocery Outlet (GO) downgraded to Sell from Buy at Goldman; tgt lowered to $24

- Harmony Gold (HMY) downgraded to Underweight from Neutral at JP Morgan

- Illumina (ILMN) downgraded to Underperform from Neutral at BofA Securities; tgt lowered to $100

- Lam Research (LRCX) downgraded to Hold from Buy at Deutsche Bank; tgt raised to $725

- Macy's (M) downgraded to Sell from Neutral at Citigroup; tgt $14

- Progressive (PGR) downgraded to Mkt Perform from Outperform at Raymond James

- Public Storage (PSA) downgraded to Equal Weight from Overweight at Wells Fargo; tgt raised to $280

- RingCentral (RNG) downgraded to Hold from Buy at Jefferies; tgt lowered to $35

- Shopify (SHOP) downgraded to Sell from Hold at DZ Bank; tgt $65

- X4 Pharmaceuticals (XFOR) downgraded to Neutral from Buy at B. Riley Securities; tgt lowered to $1

-

Others:

- ACADIA Pharmaceuticals (ACAD) initiated with a Buy at Deutsche Bank; tgt $25

- Acumen Pharmaceuticals (ABOS) initiated with a Buy at Deutsche Bank; tgt $8

- Addus HomeCare (ADUS) initiated with an Outperform at TD Cowen; tgt $105

- Alcon (ALC) initiated with a Buy at Stifel; tgt $85

- Alector (ALEC) initiated with a Buy at Deutsche Bank; tgt $12

- Alexander & Baldwin (ALEX) initiated with a Buy at Janney; tgt $20

- Amylyx Pharmaceuticals (AMLX) initiated with a Buy at Deutsche Bank; tgt $36

- AZEK (AZEK) initiated with an Outperform at Wolfe Research; tgt $43

- Bausch + Lomb (BLCO) initiated with a Hold at Stifel; tgt $16

- Boeing (BA) initiated with an Outperform at William Blair

- Brown & Brown (BRO) initiated with a Neutral at BofA Securities; tgt $77

- Camden Property (CPT) initiated with an Equal-Weight at Morgan Stanley; tgt $95

- Campbell Soup (CPB) initiated with an Equal Weight at Wells Fargo; tgt $47

- CCC Intelligent Solutions (CCCS) initiated with an Equal-Weight at Morgan Stanley; tgt $13

- Conagra (CAG) initiated with an Equal Weight at Wells Fargo; tgt $31

- COMPASS Pathways (CMPS) initiated with a Buy at Deutsche Bank; tgt $16

- Crocs (CROX) initiated with a Buy at BofA Securities; tgt $128

- Electronic Arts (EA) initiated with a Peer Perform at Wolfe Research

- Enhabit Inc. (EHAB) initiated with a Market Perform at TD Cowen; tgt $12

- Freshpet (FRPT) initiated with an Overweight at Wells Fargo; tgt $90

- fuboTV (FUBO) initiated with an Overweight at Cantor Fitzgerald; tgt $5

- Gannett (GCI) initiated with a Buy at Compass Point; tgt $5

- HEICO (HEI) initiated with an Outperform at William Blair

- mmunovant Sciences (IMVT) initiated with a Buy at Deutsche Bank; tgt $50

- J.M. Smucker (SJM) initiated with an Overweight at Wells Fargo; tgt $140

- Karuna Therapeutics (KRTX) initiated with a Buy at Deutsche Bank; tgt $227

- Kellanova (K) initiated with an Equal Weight at Wells Fargo; tgt $56

- Lamb Weston (LW) initiated with an Overweight at Wells Fargo; tgt $120

- Mid-America Aptmt (MAA) initiated with an Equal-Weight at Morgan Stanley; tgt $128

- Neurocrine Biosciences (NBIX) initiated with a Buy at Deutsche Bank; tgt $136

- Neumora Therapeutics (NMRA) initiated with a Hold at Deutsche Bank; tgt $13

- Nintendo (NTDOY) initiated with a Peer Perform at Wolfe Research

- Post (POST) initiated with an Equal Weight at Wells Fargo; tgt $92

- Prothena (PRTA) initiated with a Buy at Deutsche Bank; tgt $62

- Roivant Sciences (ROIV) initiated with a Buy at Deutsche Bank; tgt $14

- RxSight (RXST) initiated with a Buy at Stifel; tgt $40

- SAGE Therapeutics (SAGE) initiated with a Hold at Deutsche Bank; tgt $21

- Sarepta Therapeutics (SRPT) initiated with a Buy at Deutsche Bank; tgt $109

- Skyward Specialty Insurance Group (SKWD) initiated with a Buy at Jefferies; tgt $40

- Sony (SONY) initiated with an Outperform at Wolfe Research

- Solo Brands (DTC) initiated with a Neutral at B. Riley Securities; tgt $5.50

- Take-Two (TTWO) initiated with an Outperform at Wolfe Research; tgt $186

- Tapestry (TPR) resumed with an Equal-Weight at Morgan Stanley; tgt $38

- Traeger (COOK) initiated with a Buy at B. Riley Securities; tgt $3.50

- Transdigm Group (TDG) initiated with an Outperform at William Blair

- Trex (TREX) initiated with a Peer Perform at Wolfe Research

iOS 17.2 improves Telephoto camera on iPhone 15 Pro, Apple says

Alongside the host of other new features, iOS 17.2 includes an upgrade for the Telephoto camera on the iPhone 15 Pro and iPhone 15 Pro Max.

In the release notes for iOS 17.2, Apple says that the update includes “improved Telephoto camera focusing speed when capturing small faraway objects on iPhone 15 Pro and iPhone 15 Pro Max.”

iOS 17.2’s camera upgrade

Essentially, this means that the iPhone 15 Pro and iPhone 15 Pro Max should now be faster at focusing on objects that are off in the distance. We’ll have to put iOS 17.2 through more testing to know just how big of a change this is. Still, the fact it got a mention in the iOS 17.2 release notes is a good sign.

The other big camera change in iOS 17.2 is support for taking spatial video on the iPhone 15 Pro and iPhone 15 Pro. This footage is designed to be watched on Apple’s Vision Pro headset, which is on track to be released in early 2024.

- Spatial video lets you capture video on iPhone 15 Pro and iPhone 15 Pro Max so you can relive your memories in three dimensions on Apple Vision Pro

- Improved Telephoto camera focusing speed when capturing small faraway objects on iPhone 15 Pro and iPhone 15 Pro Max

iOS 17.2 is now available to iPhone users everywhere. For a full rundown of everything new, check out our coverage here.

Fortnite maker Epic Games wins its antitrust fight against Google

On Monday, a jury sided with Epic Games over Google in an antitrust case that could reshape how app marketplaces like Google Play are allowed to operate.

The unanimous verdict wraps up a three-year-long legal battle between the companies. Epic, creator of the popular online multiplayer game Fortnite, first filed its lawsuit against Google in 2020 alleging that the tech giant’s app store practices violated federal and California state antitrust laws.

The lawsuit against Google was just one piece of Epic’s flashy effort to rally app developers large and small against mobile software’s entrenched gatekeepers. Epic’s war against Apple and Google centers around its hit game Fortnite, which is free-to-play and available on nearly every software platform imaginable, current App Store and Google Play drama notwithstanding.

Epic argues that both tech giants violate antitrust laws by forcing app users to make payments through their own systems and taking a significant cut of in-app revenues in the process. In their defense, Apple and Google generally point to concerns around security to justify their shared desire to steer app users toward a central software authority.

Apple and Google do differ in their handling of third party apps — iOS doesn’t allow them while Android permits “sideloading” apps — a fact that changed the shape of Epic’s battle against Google. Still, Google cautions customers against installing external apps and the process isn’t nearly as straightforward as simply downloading something on Google Play.

On the face of those facts, it wasn’t obvious that Epic would prevail in its case against Google Play’s relatively less restricted ecosystem, but prevail it did.

“Today’s verdict is a win for all app developers and consumers around the world,” Epic Games wrote in a statement about the verdict. “It proves that Google’s app store practices are illegal and they abuse their monopoly to extract exorbitant fees, stifle competition and reduce innovation.”

Epic praised regulation in the works that could place further limitations on Apple and Google’s dominant software practices, citing the UK’s Digital Markets, Competition and Consumer Bill and the EU’s Digital Markets Act in the EU.

In a statement provided to TechCrunch, Google’s VP of Government Affairs & Public Policy Wilson White confirmed the company’s plans to appeal.

“We plan to challenge the verdict. Android and Google Play provide more choice and openness than any other major mobile platform,” White said. “… We will continue to defend the Android business model and remain deeply committed to our users, partners, and the broader Android ecosystem.”

If any of this sounds familiar, it’s likely because Epic took the same fight to Apple. That much-publicized campaign began with a spoof on Apple’s iconic “1984” advertisement and culminated in a mixed ruling two years ago.

The court’s decision mostly favored Apple, though did require the iPhone maker to open up its software market by allowing developers to direct customers to alternative payment options. In September, both companies asked the Supreme Court to reconsider the ruling and take on the case, so basically everything is still up in the air.

Epic began pointing Fortnite players to direct downloads back in 2018, steering them away from Google’s Play Store. In 2020, Epic released Fortnite through Google’s official app marketplace, but still slammed the company for discouraging users from downloading third-party apps. Now, the popular game is no longer available on Google Play, nor can it be installed on iOS devices through Apple’s App Store.

This won’t be the last we hear of Epic’s multi-front battle; Google is sure to appeal soon. Still, between the somewhat unexpected win in court and last week’s massive launch of Lego Fortnite, which attracted more than 2.4 million concurrent players, everything is coming up Epic right now.

Gapping down

In reaction to earnings/guidance:

In reaction to earnings/guidance:

- ORCL -9%, HAE -2% (guidance), CASY -1%, JCI -0.9%

Other news:

- ATHA -9.8% (Results from SHAPE Phase 2 Clinical Trial of Fosgonimeton)

- CBUS -7% (prices 2106723 Class A shares at $9.00 per share)

- SBOW -6.5% (prices secondary offering of 2.2 mln shares of common stock)

- KNTK -6.4% (prices secondary offering of 6.5 mln shares of common stock at $31.50 per share)

- HAS -5.5% (to reduce workforce by nearly 20%)

- SNCY -4.8% (prices secondary offering of 4 mln shares of its common stock by an affiliate of certain investment funds managed by affiliates of Apollo Global Management) GO -4% (CFO stepping down; reaffirms Q4 guidance)

- MAT -3% (trading in sympathy with HAS)

- LCID -2.9% (CFO departing)

- LQDA -2.7% (prices offering of 3491620 shares of common stock at a public offering price of $7.16 for total gross proceeds of approximately $25.0 million; also provides United Therapeutics Corporation (UTHR) patent update)

- AMRC -2.5% (selected in Hawaiian Electric Company's clean energy initiative)

- IOSP -2% (acquires QCP Quimica Geral)

- GPOR -1.8% (prices block trade by selling shareholders of 653464 Shares of Common Stock for gross proceeds of $84.2 mln)

- LPTX -1.5% (to present new data)

Analyst comments:

- GPRO -5.3% (downgraded to Underweight from Equal-Weight at Morgan Stanley)

- AMCX -2.1% (downgraded to Neutral from Buy at Seaport Research Partners)

- ABNB -1.9% (downgraded to Underweight from Equal Weight at Barclays)

- A -1.5% (downgraded to Neutral from Buy at BofA Securities)

- AJG -1% (downgraded to Mkt Perform from Strong Buy at Raymond James)

- EXPE -0.9% (downgraded to Equal Weight from Overweight at Barclays)